Europe

The International Renewable Energy Agency (IRENA) projects that trillions of dollars need to be invested annually into CleanTech for the world to have a chance at limiting the effects of climate change to 1.5°C to 2°C.1 Reducing emissions in the power sector represents a significant portion of the projected investment needs, and the clean energy transition is already well underway.2 We forecast that non-hydro renewables could account for nearly 40% of global power generation by 2033.3 As the energy transition continues to gain speed, we expect that companies throughout the renewable energy value chain can potentially benefit.

This piece is part of a series that dives deeper into this year’s iteration of our flagship piece, Charting Disruption.

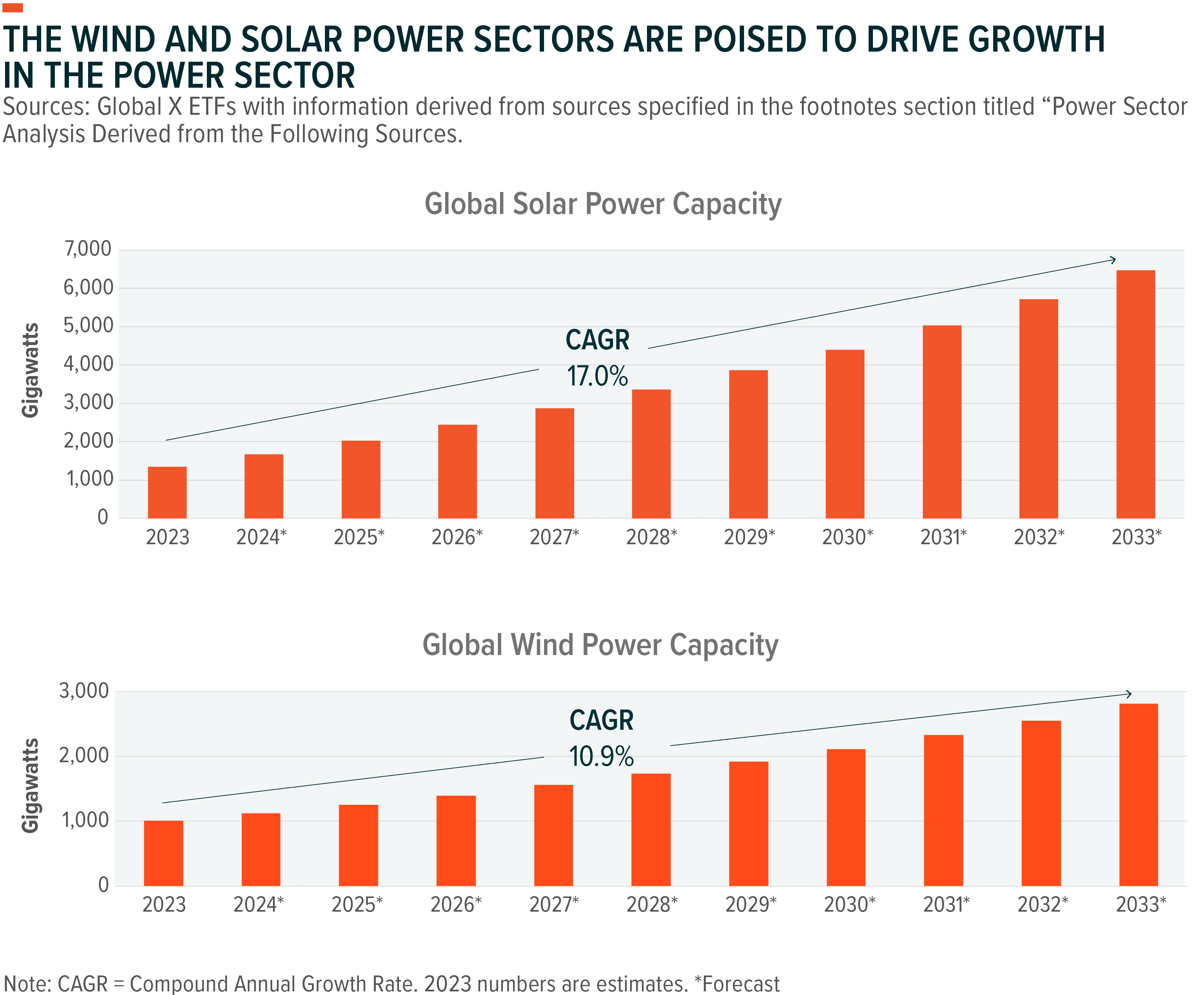

Global non-hydro renewable electricity capacity, including wind, solar, geothermal, and biomass-fired power, is forecast to increase from around 2,500GW in 2023 to nearly 9,5000GW in 2033.7 Over the same timeframe, non-hydro renewables electricity generation is forecast to increase 3.2x to reach nearly a 40% share of global power generation by 2033.8 We feel there are mostly upside risks to these forecasts, despite challenges throughout the industry in recent years.

There are several structural tailwinds that support the strong long-term growth outlook, including a robust policy landscape. Over 150 countries have announced economy-wide net-zero emissions targets, and many have set specific renewable energy targets.9 In order to meet these goals, many countries are using measures such as tax credits, project tenders, streamlined permitting procedures, and grant programs to encourage renewable energy growth.

Additionally, many corporations continue to expand the use of renewable energy to reduce operational emissions. As a result, Power Purchase Agreements (PPA) have become a popular method for sourcing renewable energy. PPA’s are contractual arrangements between an electricity generator and a buyer, typically a utility or a corporation, outlining the terms for the sale and purchase of electricity over a specified period, often facilitating the development and financing of renewable energy projects. According to Pexapark, a Swiss consulting firm, the European power purchase agreements (PPA) market broke records for both volume and number of deals signed in 2023. In 2023, 16.2 GW of renewable PPA’s were contracted, which is a 40% increase on the prior year.10 Deal volume totalled 272 and increased by 65% from 2022.11 Corporates played a significant role in driving the PPA market, securing 11.95GW across 218 deals, a 28% increase in volume and a 66% YoY increase in deal count.12

Presently, the PPA landscape in Europe is dominated by utility off-takers, corporations aligning with ESG goals, and large industrial players utilizing PPAs for power price hedging. The European renewables sector is seeing a growing role of hybrid PPA’s, involving both power generation facilities and co-located storage, green procurement strategies, PPAs for green hydrogen production, and multi-buyer structures. EDP Renovaveis, the Spanish renewable energy company, in 2023 signed a PPA with a privately owned French hydrogen firm to supply its hydrogen generation projects with renewable energy generated by a 55MW solar project in Germany.13 The signing of a PPA from an industrial gases producer specifically for hydrogen production marks a new and growing area of market growth for PPAs.

Additionally, one of the largest potential growth opportunities for corporate clean power purchases could come from the rapidly evolving AI landscape. By one estimate, energy demand could be 5x to 7x higher from the server racks that are involved in the training and use of generative AI.14

Furthermore, wind turbine and solar module manufacturers are making tech improvements that can improve system performance and expand project suitability ranges. These advancements could also cut project costs to make renewables even more cost-competitive with traditional power sources. For example, in the solar power sector, leading manufacturers like JinkoSolar, First Solar, and Hanwha Q Cells are working towards the commercialization of tandem perovskite-silicon panels, which could offer much higher efficiencies and lower manufacturing costs relative to traditional panels.15,16 Solar tech advancements could also expand the use of more niche solar applications, such as floating solar projects and agrivoltaic systems that can be used in land-constrained areas.

The growing momentum for energy storage is another key component of the robust long-term growth potential throughout the renewable energy industry. This is because energy storage is essential for integrating intermittent wind and solar power resources into power grids. Annual global battery energy storage system (ESS) installations have grown rapidly in recent years, from 22.2GWh in 2020 to an estimated 138GWh in 2023.17 Between 2022 and 2023, ESS installations were estimated to have grown 80% y-o-y.18 Looking forward, ESS installations are likely to increase further, due to cost declines, energy storage tech advancements, and expanding project pipelines for standalone storage and renewables-plus-storage projects.

Policies in major renewables markets like the United States, European Union, China and India also support positive ESS outlooks. For example, in August 2023, India's government published its National Electricity Plan, which targets 74GW/411GWh of energy storage by 2032.19 To reach these targets, the government is planning to expand measures to encourage ESS growth over the coming years. In China, there are policies in place that require renewables projects to be paired with ESS technologies. This could help energy storage capacity in the country grow to over 50GW by 2025.20

The renewable energy industry experienced strong growth in 2023, despite weaker-than-expected demand in major markets due to high interest rates and elevated project costs. Looking forward, structural tailwinds remain in place that could create significant investment opportunities over the long term. As investments into renewable energy pick up, we expect significant opportunities to emerge for companies throughout the renewable energy value chain, from solar and wind power equipment manufacturers to project developers.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. International Renewable Energy Agency (IRENA). (2023, March). World Energy Transitions Outlook 2023: 1.5°C Pathway; Preview.

2. Ibid.

3. Global X ETFs Analysis from variety of sources. See ‘Power Sector Analysis Derived from the Following Sources’ footnote below for the full list.

4. Ibid.

5. Ibid.

6. Ibid.

7. Ibid.

8. Ibid.

9. Net Zero Tracker. (n.d.). Net Zero Numbers. Accessed on January 20, 2024.

10. PV Magazine (2024, January 29). Record number of European PPAs in 2023, 11. Ibid.

12. Ibid.

13. Energy Global (2024, January, 25). Lhyfe and EDP renewables sign corporate PPA.

14. S&P Global. (2023, October 17). Power of AI: Surging datacenter load has Dominion bracing for AI’s added demand.

15. MIT Technology Review. (2024, January 15). The race to get next-generation solar technology on the market.

16. JinkoSolar. (2023, November 10). Three-Peat Victory! JinkoSolar Sets New Records for Cell, Module, and Tandem Efficiency Successively.

17. Rho Motion. (2023, August). Battery Energy Stationary Storage Quarterly Outlook, Q3 2023 – Highlights Presentation.

18. Ibid.

19. Energy Storage News. (2023, September 5). India Requires 74GW/411GWh of Energy Storage by 2032, According to National Electricity Plan.

20. South China Morning Post. (2023, February 5). China’s Energy Storage Sector Set for Strong Growth in 2023 as Electric Cars, clean Energy Projects Boost Demand.

Power Sector Analysis Derived from the Following Sources

ABEEolica. (2023). Annual wind energy report 2022.

2. Absolar. (2023, October 16). Solar Photovoltaic Energy in Brazil: Absolar’s Infographic.

3. AK&M. (2023, August 19). The volume of electric generation in Russia in January-June 2023 has not changed.

4. Canada Energy Regulator. (2023). Canada’s Energy Future 2023.

5. Carbon Brief. (2023, November 11). Analysis: China’s emissions set to fall in 2024 after record growth in clean energy.

6. Central electricity Authority – Government of India. (n.d.). Installed Capacity Report: October 2023. Accessed November 12, 2023.

7. Climate Cooperation China. (2023, February 1). 2022 Energy Statistics Show Rapid Development of Renewable Energy in China.

8. Ember. (2023, October 3). Solar adoption in India entering “accelerating growth” phase.

9. Empresa de Pesquisa Energética (EPE). (n.d.). Pde 2031 - English version. Accessed November 11, 2023.

10. EnergyWorld.com. (2023, September 16). India may add up to 30GW more thermal power capacity, says R K Singh.

11. Fraunhofer Institute for Solar Energy Systems ISE. (2023, January 3). Net Electricity Generation in Germany in 2022: Significant Increase in Generation from Wind and PV.

12. Fraunhofer Institute for Solar Energy Systems ISE. (2023, July 3). German Net Power Generation in First Half of 2023: Record Renewable Energy Share of 57.7 Percent.

13. Government of India Ministry of Power. (n.d.). Generation. Accessed on November 13, 2023.

14. International Energy Agency (IEA). (2023, July 19). Declining electricity consumption in advanced economies is weighing on global demand growth this year.

15. International Energy Agency (IEA). (2023, October). World Energy Outlook 2023.

16. International Energy Agency (IEA). (2023, June). Renewable Energy Market Update: Outlook for 2023 and 2024.

17. Ministry of Economy, Trade and Industry (METI). (2021, November 26). Outline of strategic energy plan. Agency for Natural Resources and Energy.

18. PVTech. (2023, July 31). China’s installed solar capacity reaches 470GW as of H1 2023.

19. Renewable Energy Institute. (2023, June 16). How Electricity Supply and Demand Changed Amid Soaring Fossil Fuel Prices.

20. Reuters. (2023, November 2). German power mix may get dirtier for 1st non-nuclear winter.

21. U.S. Office of Energy Efficiency and Renewable Energy. (2023, August 24). Offshore Wind Market Report: 2023 Edition.

22. U.S. Office of Energy Efficiency and Renewable Energy. (2023, August 24). Land-Based Wind Market Report: 2023 Edition.

23. U.S. Energy Information Administration (EIA). (n.d.). International: Data. Accessed on November 15, 2023.

24. U.S. Energy Information Administration (EIA). (2023, October 24). Electricity: Preliminary