Europe

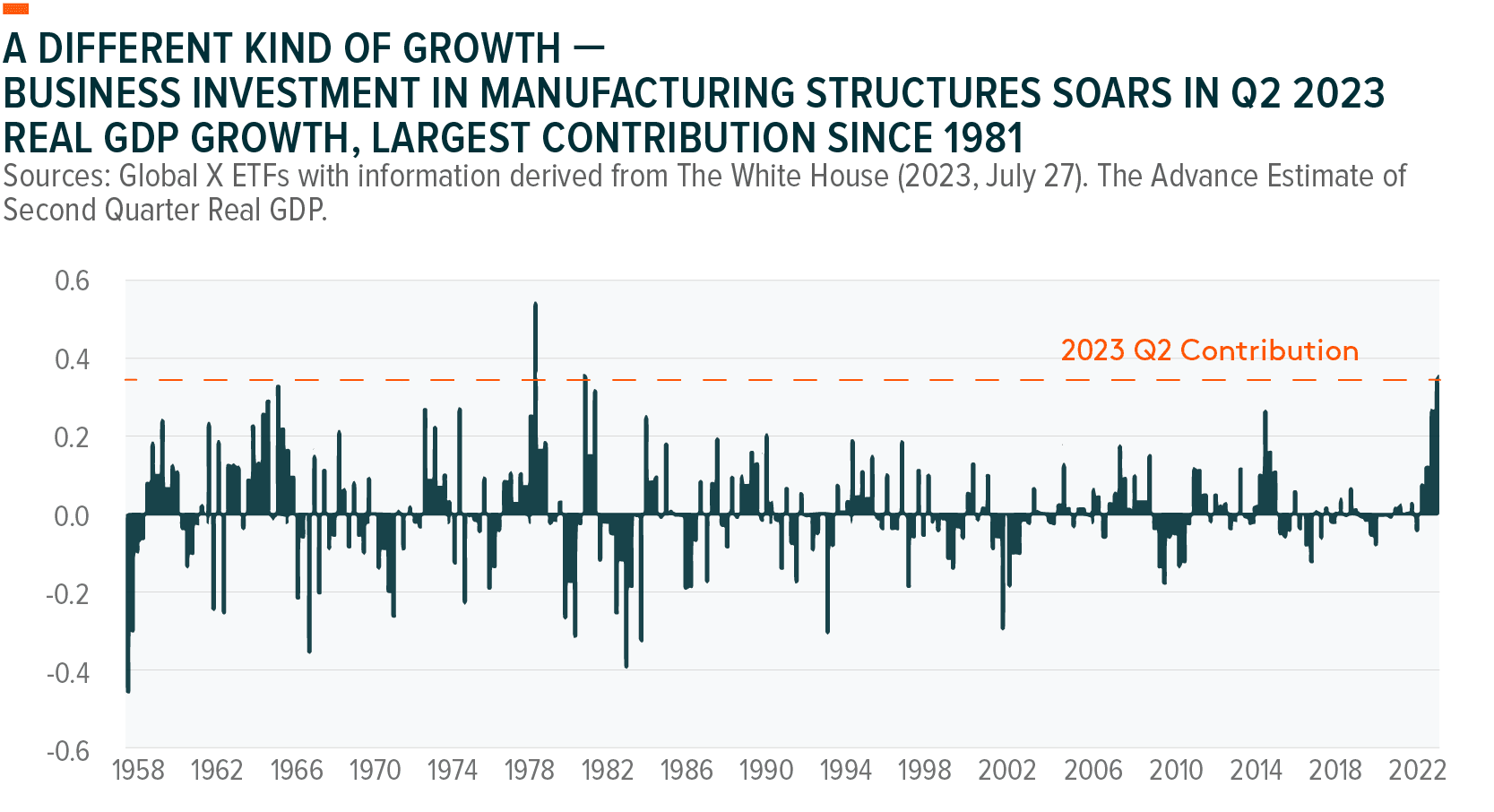

Economic growth that’s not only a result but also a deliberate pursuit is differentiated economic growth. So one item that caught our attention in Q2 real GDP growth printing at a better-than-expected 2.4% was that 0.4% of it derived from private investment in manufacturing structures.1 It was that component’s largest contribution to real GDP growth in more than 40 years, hearkening memories of the 1980s business boom.2 This type of business investment has an innate ability to shape the economy’s trajectory from the factory floor. And with companies increasingly embracing disruptive technologies, we expect diverse investment opportunities to emerge as manufacturing enters a new era.

As the sum of all its economic activities, GDP is the heartbeat of an economy. A window into the strength of that pulse is GDP growth, being the sum of consumer spending, business investment, government spending, and net exports (exports minus imports).

Consumer spending is the bellwether in the U.S. economy, constituting nearly 70% of nominal GDP, and consumers continued to spend in Q2 despite still-high inflation and interest rates. Spending grew by 1.6% in real annualised terms, propelled by a still-strong labour market.3 It was another example of a resilient consumer helping the economy to defy recession odds.

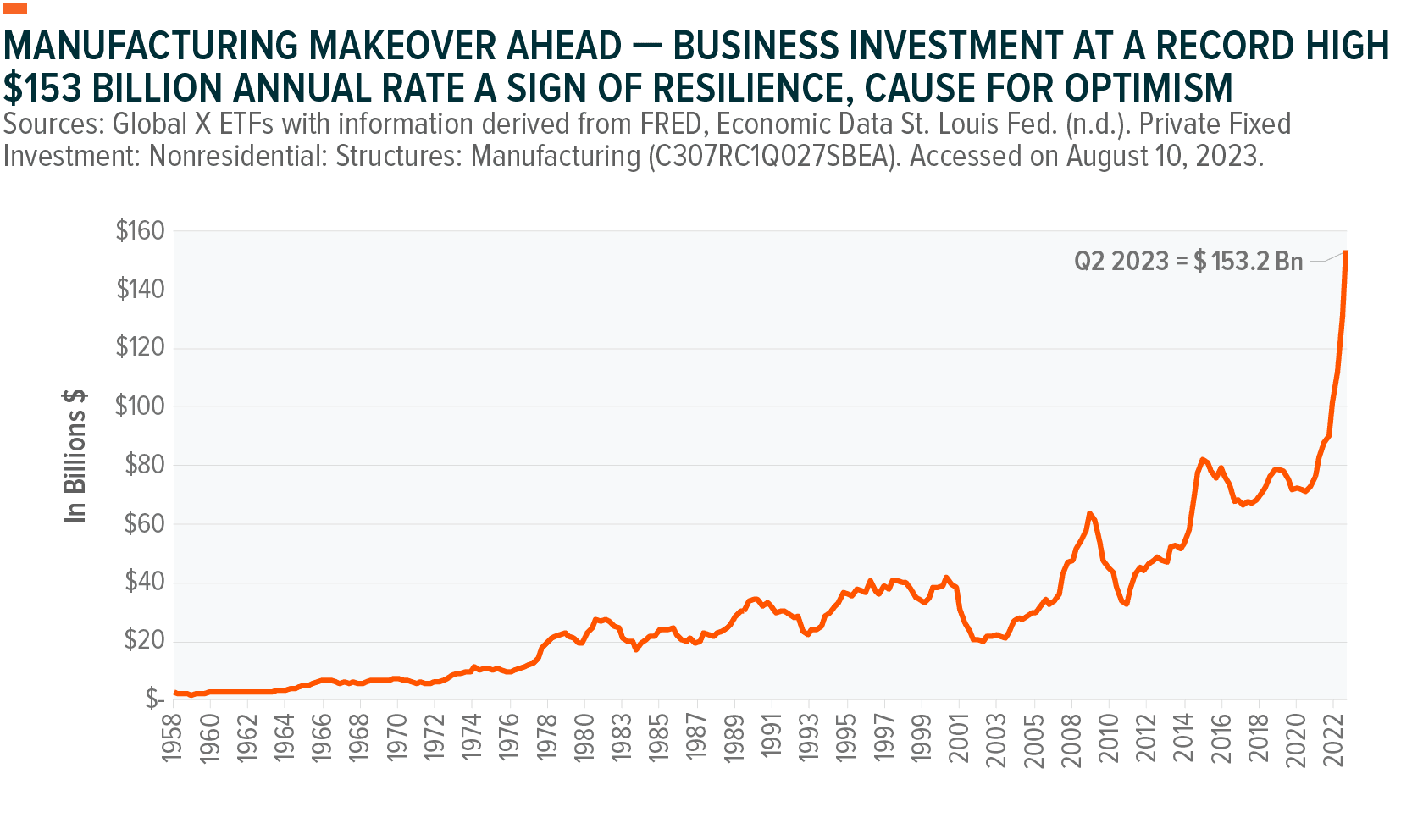

Business investment represents only 13% of nominal GDP, but it punches above its weight in terms of impact because it can mold economic growth by fostering job creation and enhancing household earnings.4 For example, back in the 1980s, construction employment grew by 19% even with two recessions early in the decade.5 So business investment contributing 0.4% in Q2 is a notable input when looking at how the economy may trend.6 On a nominal basis, business investment was at a $153 billion annual rate in Q2, the highest ever.7

Business investment plus recent legislative efforts like the Inflation Reduction Act (IRA), the CHIPS and Science Act (CHIPS), and the Infrastructure Investment and Jobs Act (IIJA) bode well for U.S. manufacturing. This confluence sets the stage for a potentially transformative boom era for manufacturing and a burgeoning opportunity for infrastructure development companies.

Whether by building advanced factories that incorporate AI, automation, and next-generation connectivity, or by modernising existing units, we believe that the future of manufacturing is an economic growth story. That this growth story is by design and built for the long term puts a different spin on it relative to recent history. This business investment could create compelling opportunities across the U.S. infrastructure development theme and the companies that make it go, from the factory and beyond.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. The White House (2023, July 27). The Advance Estimate of Second Quarter Real GDP.

2. Ibid.

3. Ibid.

4. Ibid.

5. Plunkert, L. M. (1990, September). The 1980’s: A Decade of Job Growth and Industry Shifts. Monthly Labor Review.

6. The White House (2023, July 27). The Advance Estimate of Second Quarter Real GDP.

7. FRED, Economic Data St. Louis Fed. (n.d.). Private Fixed Investment: Nonresidential: Structures: Manufacturing (C307RC1Q027SBEA). Accessed on August 10, 2023.

8. Jacobs Investor Relations. (2023, August 8). Jacobs Fiscal Third Quarter 2023 Earnings Conference Call.

9. Nucor Corporation. (2023, July 25). Nucor’s Second Quarter of 2023 Conference Call.

10. Topalian, L., & Laxton, S. (2023, July 25). Second Quarter 2023 Earnings Call [PowerPoint slides]. Nucor Corporation.

11. Norfolk Southern Corporation. (2023, July 27). Norfolk Southern Corporation FQ2 2023 Earnings Call.

12. Norfolk Southern Corporation. (2023, July 27). Q2 2023 Earnings Call [PowerPoint slides].

13. Terex Corporation.. (2023,August 2). Terex Corporation Earnings Conference Call.