Europe

The prevalence of diabetes is rapidly increasing, fuelled by an aging population and climbing incidence of obesity. Given the vast amount of people diagnosed with diabetes, along with many more who are prediabetic and undiagnosed, the market opportunity for innovative treatments and preventative solutions is immense. New technologies for disease management and novel treatment categories are providing hope for effective prevention, management, and treatment of diabetes.

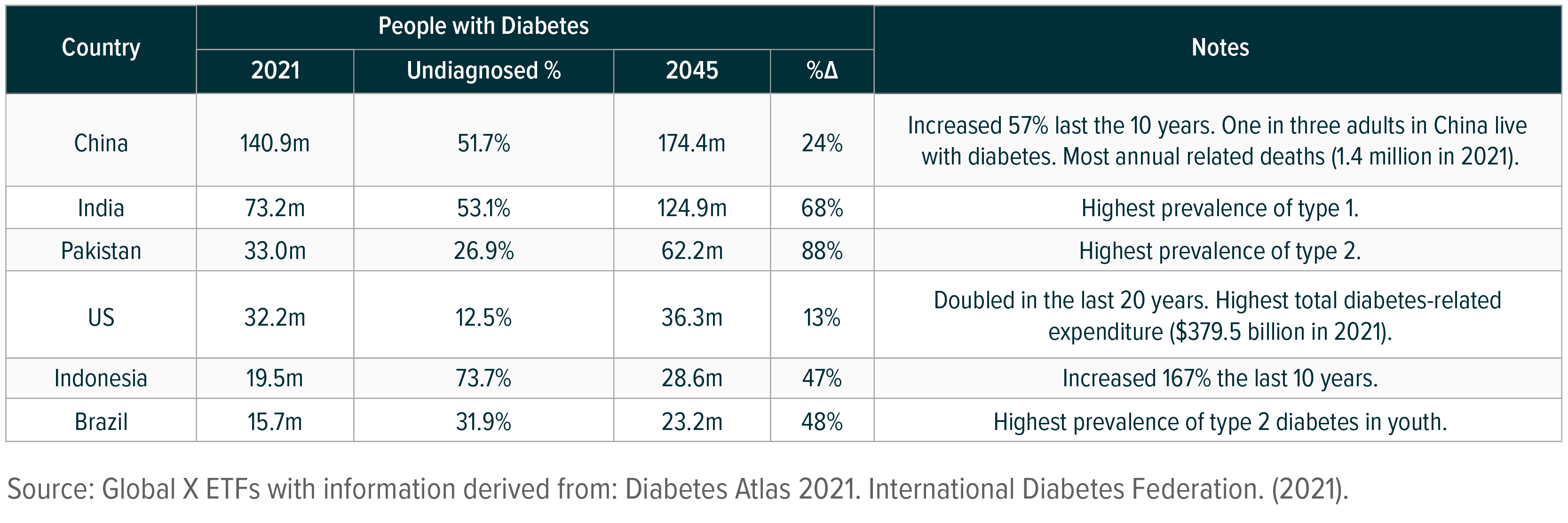

The health care industry, fuelled by a growing number of patients, continues to drive innovation in the diabetes space. Diabetes is one of the top leading causes of death worldwide, with 6.7 million adult deaths directly tied to the disease in 2021.1 The number of adults with the illness across the globe is also quickly increasing. Where the figure stood at 151 million individuals in 2000, it now stands at over 537 million patients worldwide.2 The industry forecasts 783 million individuals will have diabetes by 2045, though certain countries are expected to see accelerated prevalence of the illness.3

Driven by increased prevalence of diabetes, the illness caused at least $966 billion in health expenditures in 2021, a 316% increase over the last 15 years.4 In the United States, $1 in every $4 in health care costs is spent on caring for individuals with diabetes, with a total estimated $379.5 billion spent in the US on diabetes-related expenses.5, 6 An estimated 48 to 64% of lifetime medical costs for diabetes patients are complications from the illness, such as heart disease and stroke.7

The staggering patient outcomes and economic impact have fuelled innovation in the sector, with an array of novel approaches to disease management. Notably, however, treatment of the illness varies depending on the type of diabetes a patient has.

To determine how well their treatments are working, diabetes patients must measure glucose levels throughout the day. This helps guide the patients on how much insulin their bodies need and when. Keeping track of glucose levels over time also plays a key role in doctor evaluations to manage the condition.

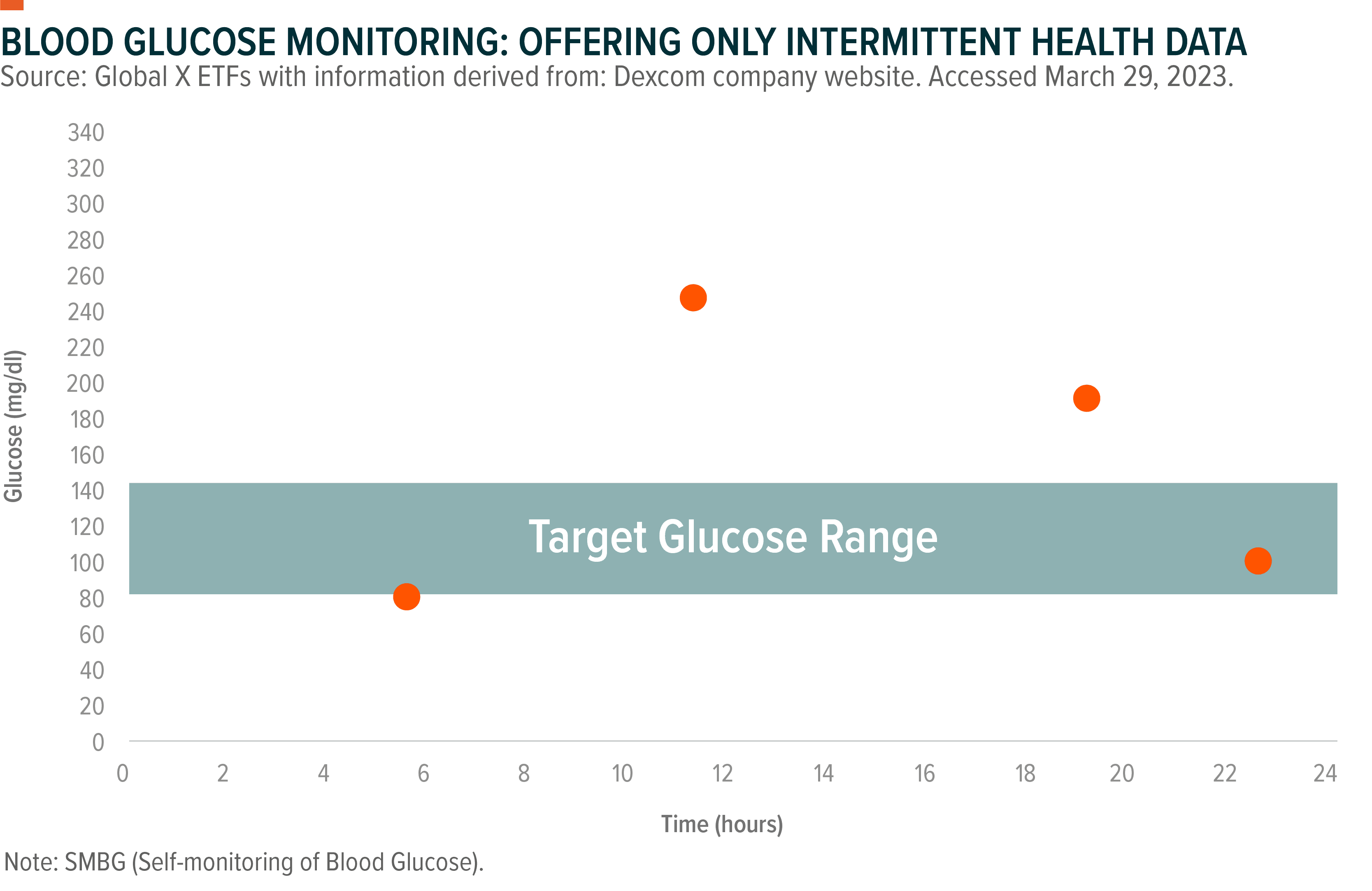

For a long time, patients solely relied on blood glucose monitors (BGMs), which analyse a small amount of blood, usually from finger pricks. This method is up to 95% accurate and can be used four to 10 times a day.9, 10 BGMs also require manual data collection and manual data sharing.

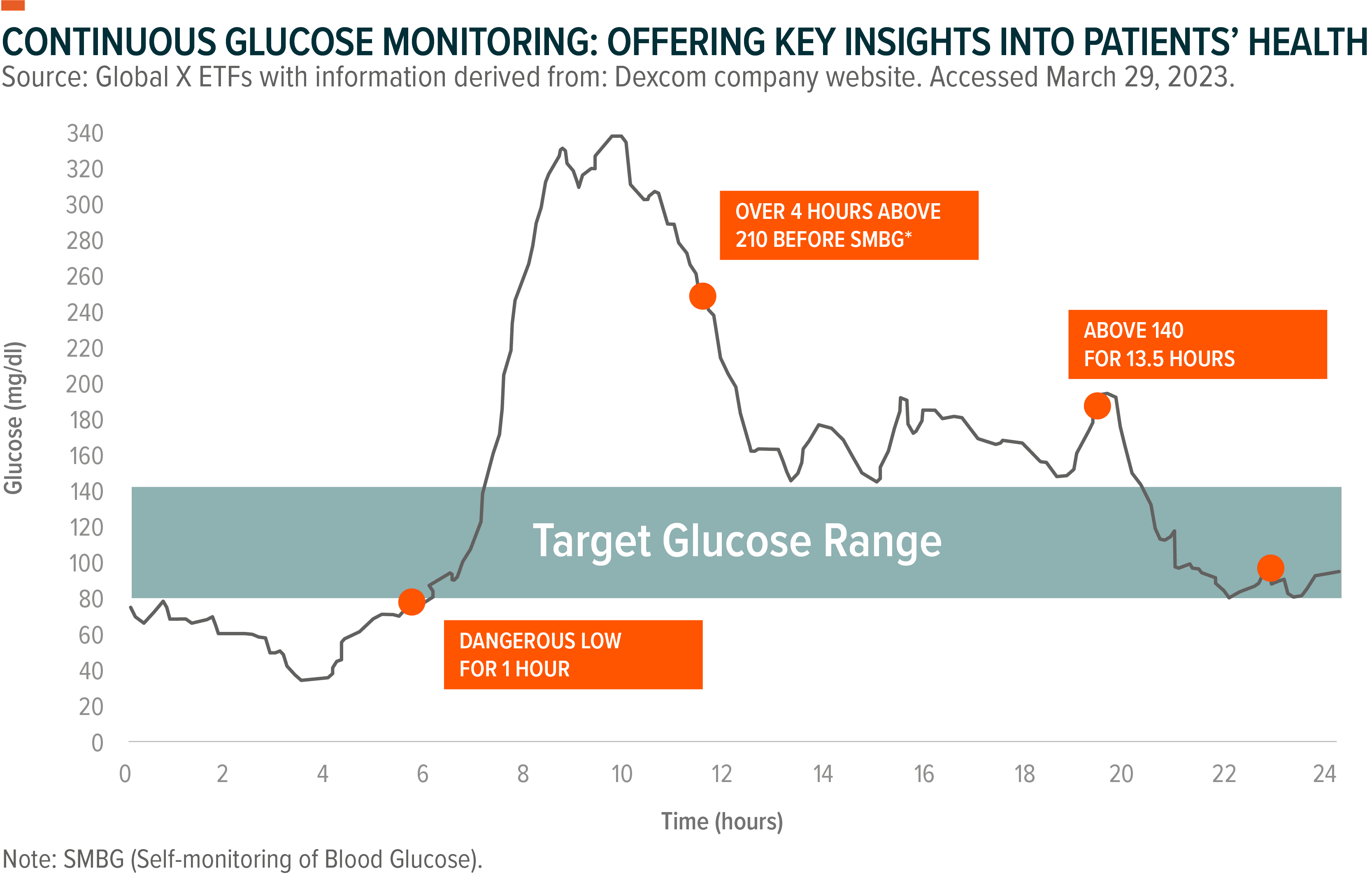

Continuous glucose monitors (CGMs) offer an alternative. These are sensors placed under the skin that measure glucose levels and automatically transfer data to a smart device. The devices measure up to 288 readings a day and automatically collect patients’ data.11 Patients can set up alerts when glucose levels are out of range and can remotely share their data with loved ones or their physician.

CGMs have gained in popularity since first being commercialized in 1999, and new data continue to support the promise of the technology. A recent clinical trial showed a 67% decrease in patient hospitalizations when using a CGM.12

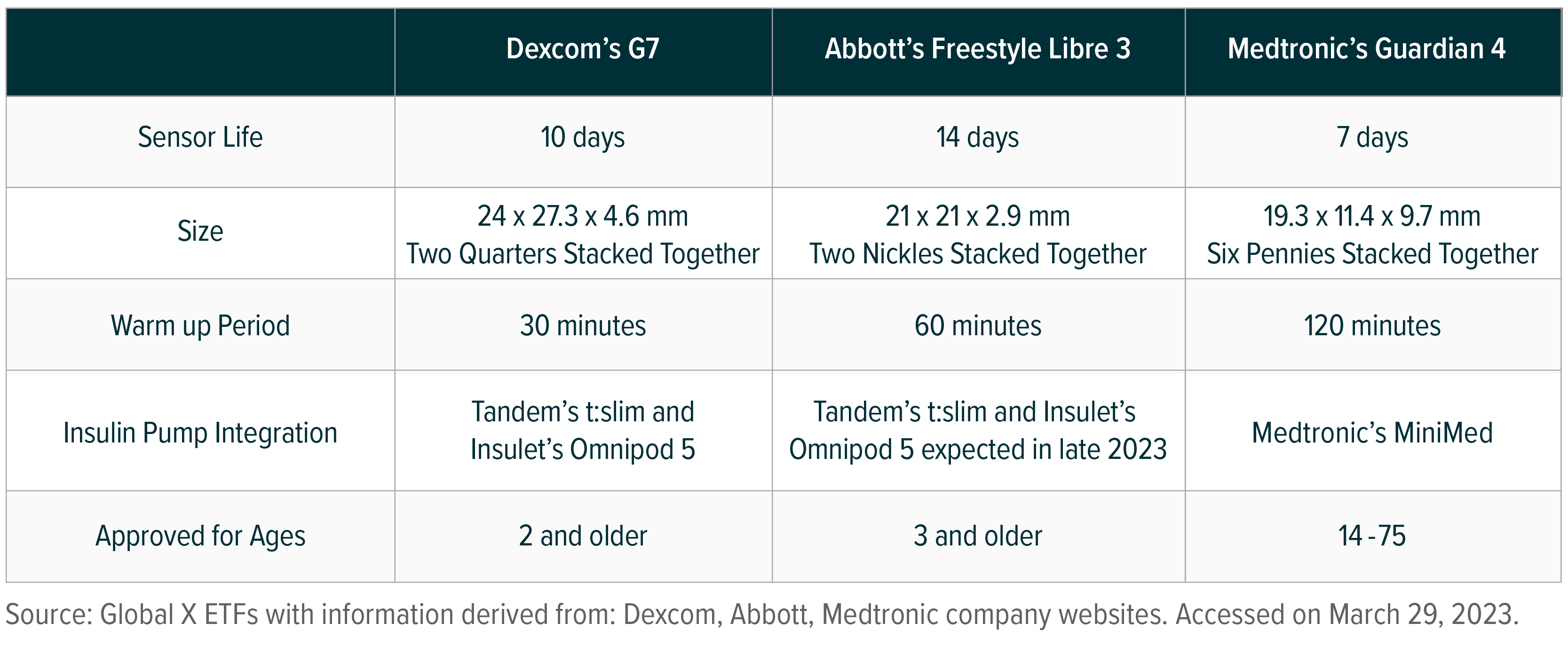

The CGM market is concentrated among three main players: Dexcom, Abbott, and Medtronic. All three companies have recently reported strong revenues, as the industry further embraces the technology. Abbott leads the way in CGM revenue, with an impressive 4.5 million patients utilizing its devices, resulting in estimated revenue of $1,000 per user annually.13 In 2022, Abbott’s diabetes segment generated $4.76 billion in revenue.14 Dexcom, for its part, reported $2.91 billion in sales in 2022, while Medtronic reported $2.3 billion in total diabetes sales in 2022, including its Guardian 4 CGM and MiniMed insulin pump.15

Abbott recently announced plans to grow its Freestyle Libre CGM into a $10 billion product over the next five years, which would represent a 15% compound annual growth rate (CAGR).16 Abbott is also working on a new wearable device that can monitor both glucose and ketone levels to help patients at risk of developing diabetic ketoacidosis, a common complication for Type 1 patients. Dexcom, for its part, expects 2023 revenue to increase 20%, aided by the recent approval of the G7.17 The firm forecasts revenues could reach $3.35 billion to $3.49 billion in 2023.18

Under new guidance by the Centers of Medicare and Medicaid Services (CMS), CGMs are now reimbursed for a wider proportion of diabetes patients, expanding the market opportunity for CGM makers. Specifically, the proposal expands reimbursement to patients who take long-acting insulin, also known as basal insulin, as little as once a day. The new guidance doubles the market opportunity of type 1 and type 2 insulin dependent patients.19 This would be a particularly large win in the type 2 diabetes space, in which CGMs only have about 25% penetration.20

The technical enhancements in the care of diabetic patients have also opened a new way to automatically deliver insulin based on a patient’s needs over time. Insulin pumps are small, wearable devices that deliver insulin to diabetes patients and offer an alternative to traditional insulin injections. Insulin pumps are a more consistent and convenient method for insulin delivery, removing patient guess work. When used in combination with a CGM, the pump adjusts insulin levels specifically based on the patient’s blood glucose readings. This is known a closed loop system.

A host of insulin pumps have entered the market in recent years, with Medtronic, Tandem Diabetes, Insulet, and Roche having come out with products that show significant benefit to patients. Currently, an estimated 20-30% of T1D patients utilize them over multiple daily injections (MDIs).21 Given their ease of use, studies have shown insulin pumps can increase the “time in range” (TIR) for diabetic patients by nearly 24%.22 A recent study also showed that T2D patients using Tandem’s t:slim X2 pump, when used in combination with Dexcom’s CGM, spend 3.6 hours a day longer in the target blood glucose range after switching to the closed loop system.23

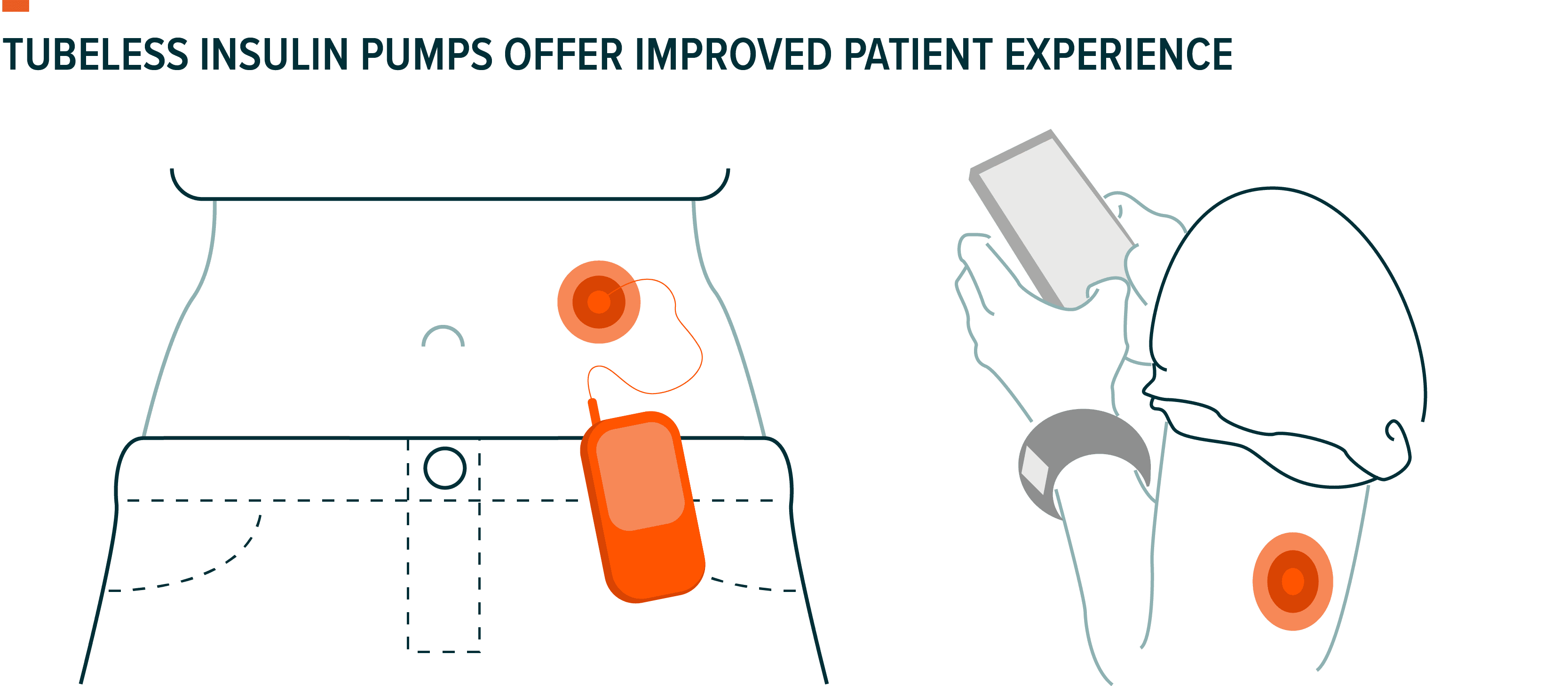

Technology for insulin pumps is improving rapidly, and newer models offer an improved patient experience via a sleeker, more comfortable design. Traditional insulin pumps usually require a small receiver with a tube that goes under the skin to deliver insulin. Newer models, like Insulet’s Omnipod, offer a tubeless device. These are also known as patch pumps and are small adhesive patches worn directly on the skin. The patch contains all of the mechanisms to seamlessly deliver insulin, without the need for any tubing.

Tubeless devices offer a more convenient system for patients, reducing the risk of the tubing getting dislodged and interrupting insulin delivery. The sleek design is particularly beneficial for active patients and paediatric diabetics. Young patients with diabetes tend to require smaller doses of insulin, have more unpredictable eating habits, engage in more unplanned physical activity, and may struggle to recognize and communicate the need for treatment during episodes of low blood sugar.

Fuelled by recent innovation and ongoing adoption of insulin pump technology, pump manufacturers continue to grow their footprint. Insulet reported $1.25 billion in 2022 revenue, representing 20% growth from the prior year, and expects 2023 revenue to grow an additional 14-19%.24 Tandem Diabetes, for its part, reported $801 billion in 2022 revenue.25 Following the 14% growth in 2022, Tandem now projects 10-12% growth in 2023.26 Expected growth from Insulet and Tandem will play a key role in the industry reaching anticipated revenues of $8.3 billion by 2028, up from $4.6 billion in 2021.27

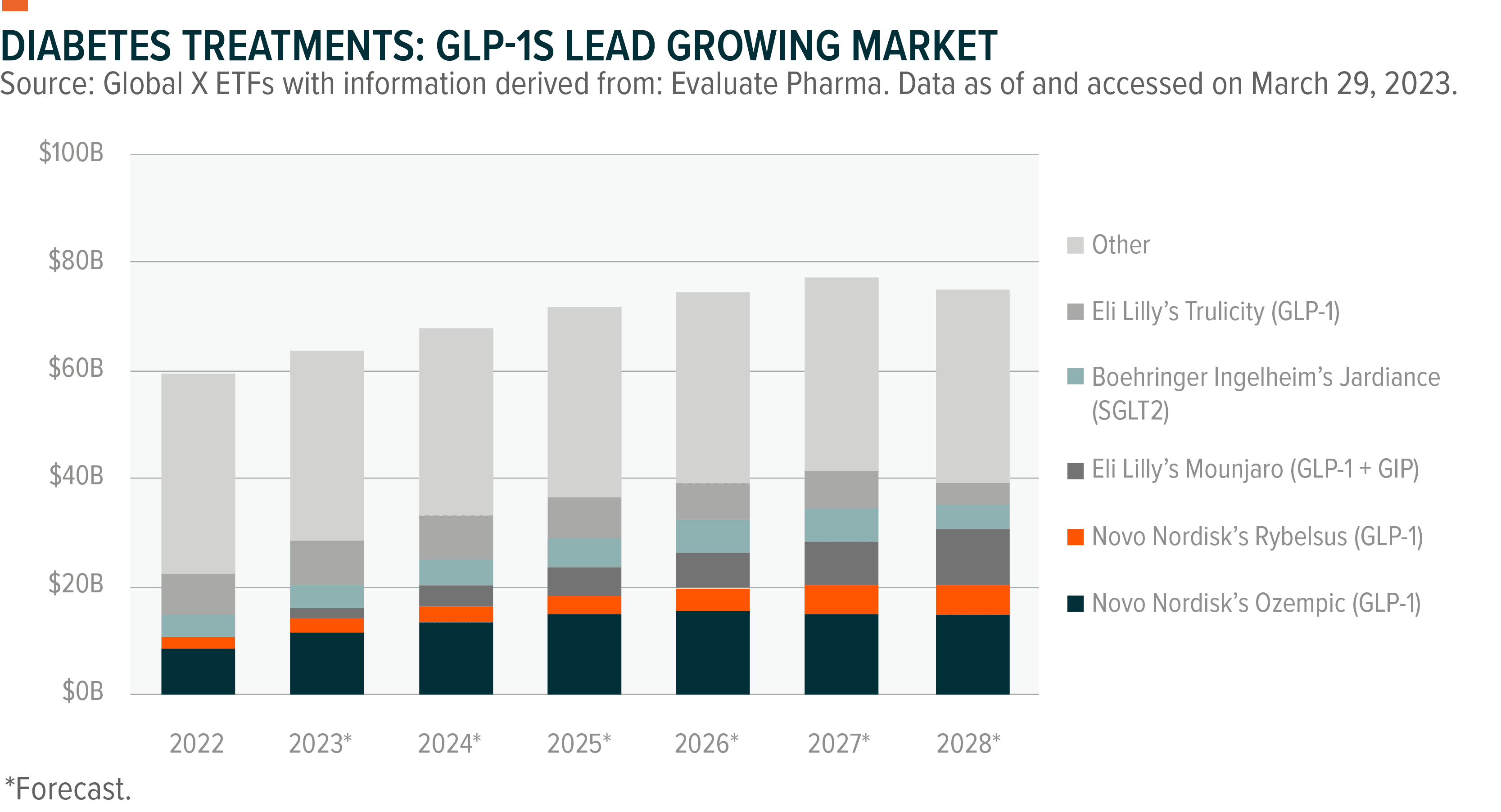

A new class of therapies has come to market, improving patient outcomes for type 2 diabetes patients. GLP-1 (glucagon-like peptide 1) stimulates the body to produce more insulin when a patient’s blood sugar levels start to rise, helping manage diabetic symptoms. This treatment category has revolutionized the type 2 diabetes space, with four out of five of the top expected products in T2D in 2028 being GLP-1s.28 To meet demand, both Lilly and Novo look to expand supply capacity of their GLP-1 portfolios, with Eli Lilly looking to double its capacity by the end of 2023.29

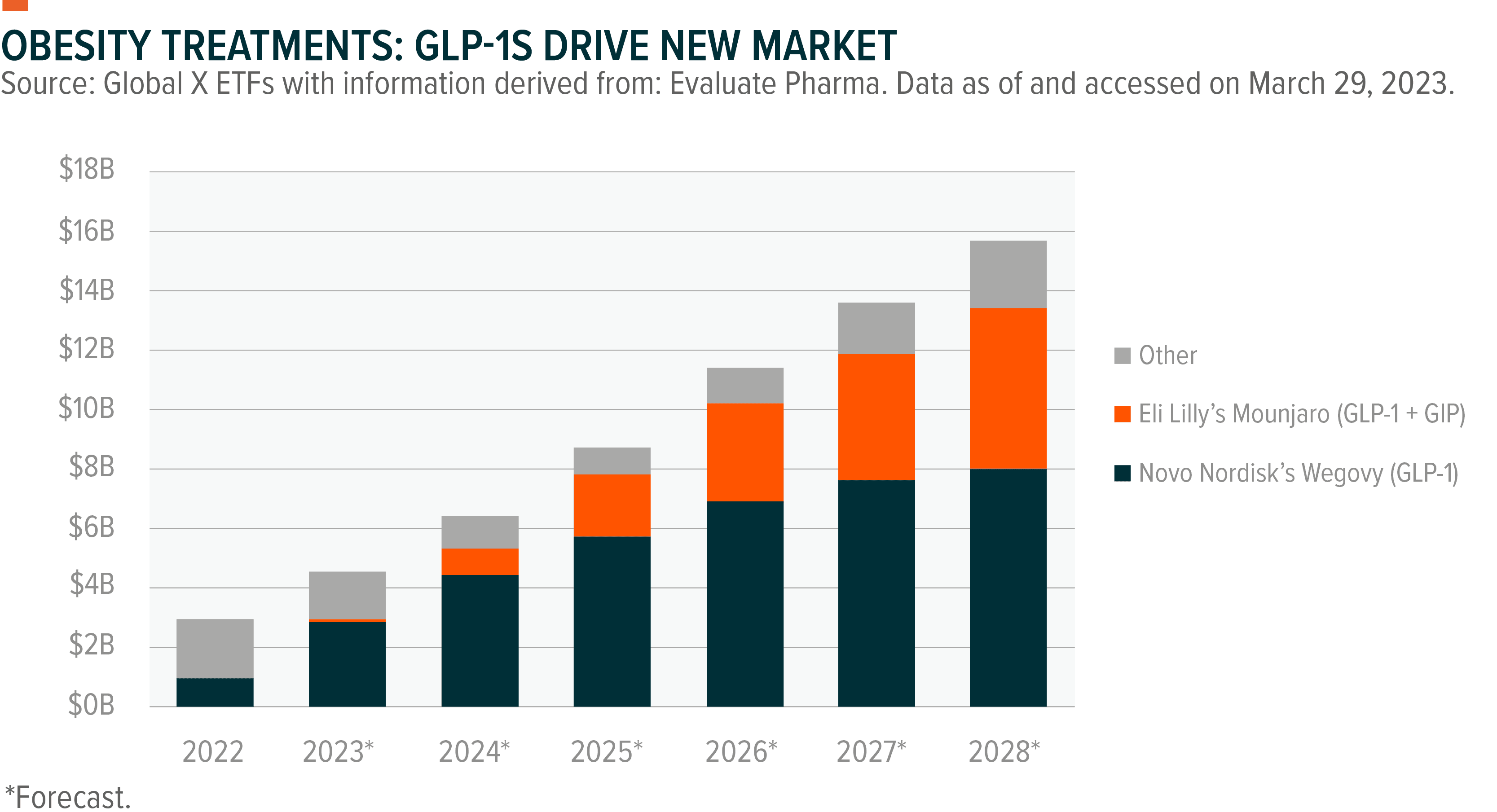

This drug category can also help curb hunger, opening its potential use to the obesity market, which is expected to be worth over $50 billion by the end of the decade, up from $2.7 billion today.30 The industry is set to particularly benefit from a broader shift in health care to focus more on causes of illnesses like diabetes and cardiovascular disease rather than treatment of their symptoms. Studies have shown obesity accounts for 80 to 85% of the risk in developing type 2 diabetes, and obese individuals are 80 times more likely to develop the illness than non-obese people.31 Prediabetes patients, for example, could benefit from such treatments. Estimates show that for every type 2 diabetic, a population of 30 million patients in the United States, there are about twice as many prediabetics.32, 33

The obesity space is expected to grow at a compound annual growth rate (CAGR) of 37% through 2028, compared to diabetes’ expected 4% CAGR in the same period.34, 35

Lily’s Mounjaro showed promising results in its SURMOUNT-1 clinical trial, in which patients achieved average weight reductions of 16%, 21.4%, and 22.5% at 5mg, 10mg, and 15mg doses, respectively.36

The results topped Novo Nordisk’s diabetes drug Ozempic, marketed as Wegovy to obesity patients, which in clinical trials helped patients lose an average 12.4% of their body weight versus placebo.37

The medical community is optimistic about Mounjaro and its potential impact on the obesity market, as its efficacy data compares favourably to conventional surgical approaches. Sleeve gastrectomy surgery and gastric bypass typically result in average weight reductions of 20% and 25-30%, respectively, but come with high risks and cost upwards of $35,000.38 GLP-1s are projected to play a pivotal role in addressing the global obesity epidemic, as global obesity rates have nearly tripled since 1975.39

The landscape for diabetes treatment and prevention has evolved greatly in recent years, with additional breakthroughs likely to follow. Demographic shifts toward an older population, and the ongoing public health problem of obesity, suggest that there is a large market opportunity for companies that can deliver innovative solutions for not just diabetes treatment, but also prevention.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Diabetes Atlas 2021. International Diabetes Federation. (2021).

2. Ibid.

3. Ibid.

4. Ibid.

5. Health and Economic Benefits of Diabetes Interventions. Centers for Disease Control and Prevention. (2022, December 21).

6. Diabetes Atlas 2021. International Diabetes Federation. (2021).

7. Health and Economic Benefits of Diabetes Interventions. Centers for Disease Control and Prevention. (2022, December 21).

8. Evaluate Pharma. (2022). Diabetes, type 1: Indication Overview │Indication Profile. Retrieved March 29, 2023.

9. Beyond Type 2. (2022, October 12). How accurate are blood glucose monitors?

10. Mayo Clinic Staff. (2022, February 1). Blood sugar testing: Why, When and How.

11. Dexcom. (n.d.). Continuous Glucose Monitoring vs Blood Glucose Monitoring. Accessed on March 29, 2022.

12. MedTech Drive. (2022, September 21). Abbott’s Freestyle Libre linked to 67% drop in hospitalizations for type 2 diabetes patients: Study.

13. MedTech Drive. (2023, January 10). How Abbott plans to make its freestyle libre a $10B product.

14. Abbott Laboratories. 2022 Abbott Annual Report.

15. Dexcom 2022 10K.

16. MedTech Drive. (2023, January 10). How Abbott plans to make its freestyle libre a $10B product.

17. MedTech Drive. (2023, January 9). Dexcom forecasts 2023 revenue to rise as much as 20% on G7 launch.

18. Ibid.

19. MedTech Drive. (2022, October 7). Dexcom, Abbott have ‘massive opportunity’ with new CGM coverage proposal: analysts.

20. Ibid.

21. Endocrinology Advisor. (2019, January 9). Diabetes and the use of insulin pumps.

22. Healio. (2023, February 27). Insulin pump with adaptive therapy settings improved time in range in type 1 diabetes.

23. Medtech Drive. (2022, November 14). Tandem pump, paired with Dexcom CGM, boosts blood glucose control in type 2 diabetics.

24. Insulet. (2023, February 23). Q4 2022 Insulet Corporation Earnings Conference Call.

25. Tandem Diabetes. (2023, February 22). Tandem Diabetes Care Announces Fourth Quarter 2022 Financial Results and Full Year 2023 Financial Guidance.

26. Ibid.

27. Grand View Research. (2022, January 6). Insulin pump market size & share report, 2021-2028.

28. Evaluate Pharma. (2022). Diabetes, Type 2: Indication Overview │Summary. Retrieved March 29, 2022.

29. Evaluate Vantage. (2023, February 2). Lilly hits the Mounjaro plateau.

30. Fierce Pharma. (2022, July 15). Novo Nordisk, Eli Lilly poised to divvy up obesity market that could be worth $50B in 2030: Analysts.

31. Diabetes & Obesity. Diabetes U.K. (2023, January 22).

32. Fierce Pharma. (2022, May 13). Lilly’s highly anticipated diabetes Drug Mounjaro wins FDA Blessing.

33. Fierce Pharma. (2022, June 8). Lilly, Novo Nordisk’s weight loss meds could replace surgery for obesity patients: Specialist.

34. Evaluate Pharma. (2022). Obesity: Indication Overview │Summary. Retrieved March 29, 2022.

35. Evaluate Pharma. (2022). Diabetes: Indication Overview │Summary. Retrieved March 29, 2022.

36. Lilly’s Trizepatide delivered up to 22.5% weight loss in adults with obesity or overweight in surmount-1. Eli Lilly and Company. (2022, April 28).

37. Fierce Pharma. (2022, September 23). With Lilly’s Mounjaro set for stardom, an Alzheimer’s win would be ‘icing on the cake’: Analysts.

38. Fierce Pharma. (2022, June 8). Lilly, Novo Nordisk’s weight loss meds could replace surgery for obesity patients: Specialist.

39. World Health Organization. (2021, June 9). Obesity and overweight.