Europe

Personal Consumption Expenditures (PCE) inflation data for January were in line with expectations, leaving bets for three fed funds rate cuts this year unchanged.1 While the Federal Open Market Committee’s (FOMC) favourite inflation gauge suggests inflation remains on track to its 2% target and economic activity remains strong, questions about financial stability may put a new twist on the rates path.2 Challenges in the U.S. banking sector combined with a deterioration of the U.S. fiscal outlook could increase rate volatility and risk premiums on U.S. Treasuries across the curve and weigh on the FOMC’s decision.

To cope with growing regional divergences and uneven economic prospects, increasing cash holdings to counterbalance equity risk can be a valuable strategy. Also, the strong equity market performances led by Tech this year highlight tactical opportunities in thematic investing.3 A careful selection of themes could help investors add regional and sector tilts to leverage macro views while diversifying idiosyncratic risk.

Investment strategies highlighted this month:

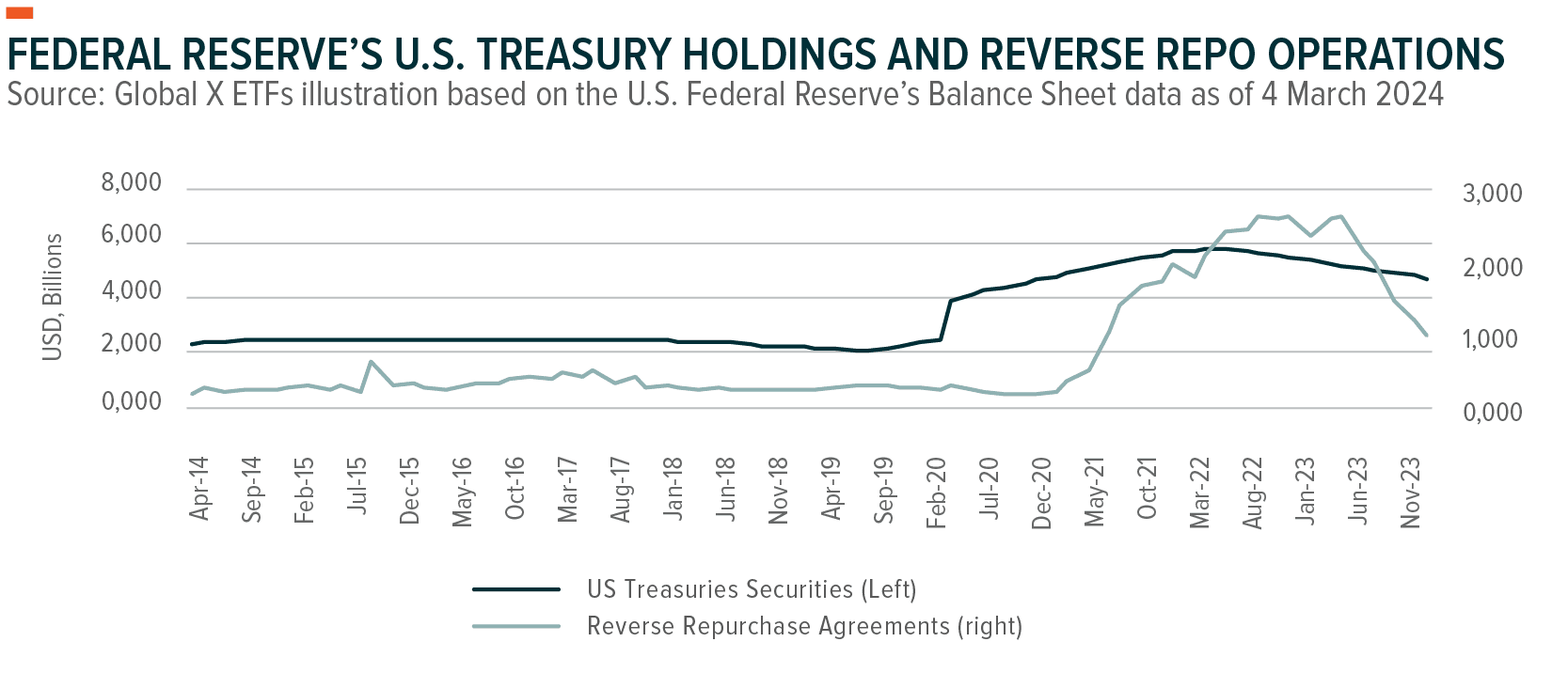

The Fed could soon start discussing adjustments to its balance sheet reductions with financial institutions about to abandon reverse repo. Cash flowing from banks’ deposits to money market funds would reduce the size of bank balance sheets at the same time the Fed’s Bank Term Funding Program (BTFP) ends on March 11th, possibly creating challenges for the U.S. banking sector.4

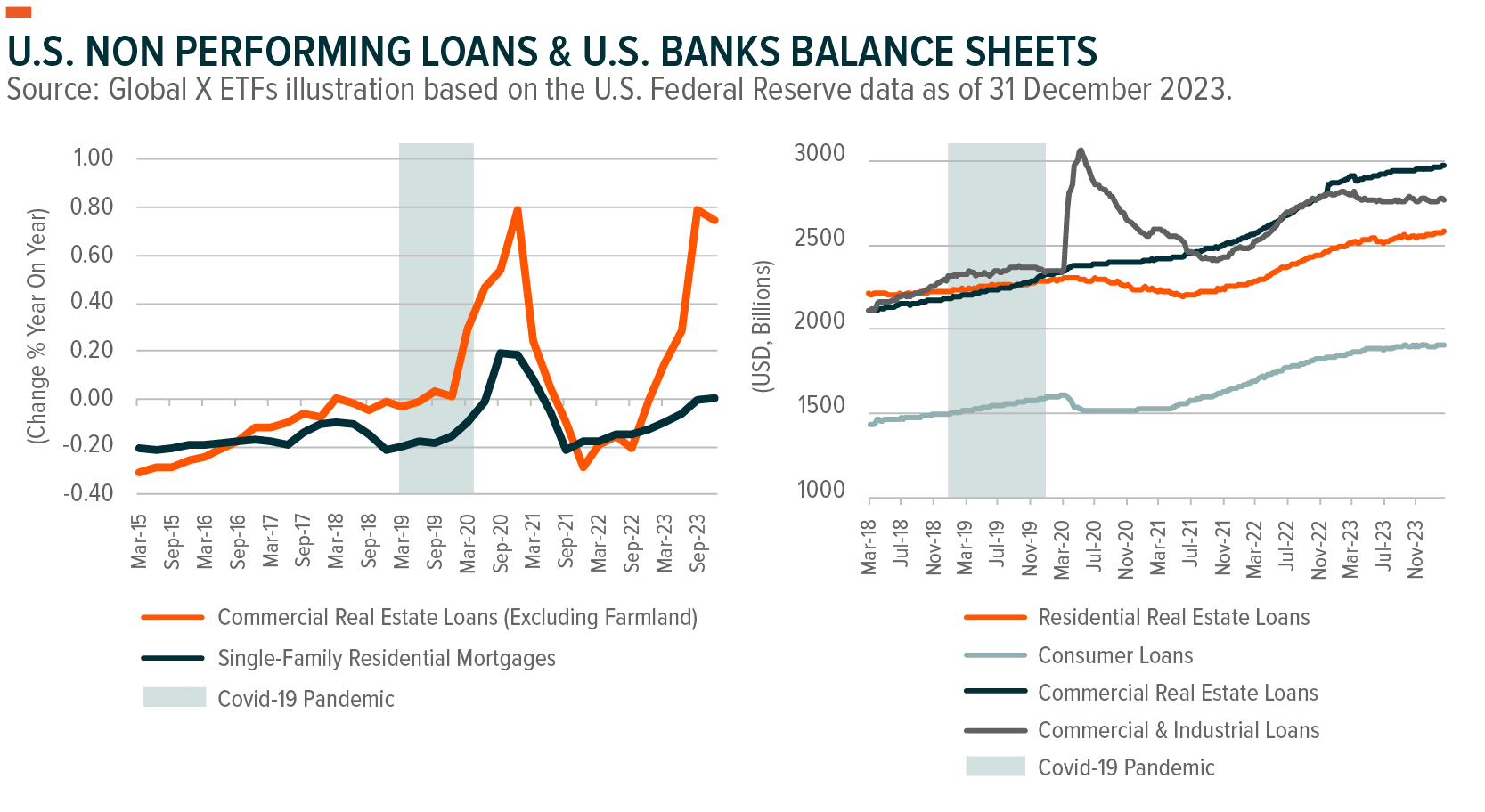

Bank balance sheets are a potential concern. The Signature, Silvergate, and Silicon Valley Bank failures in 2023, and more recently, disappointing results causing New York Community Bancorp to drop 45% on 31 January, point to heightened focus on the banking sector’s financial stability. In particular, commercial real estate looks like it could remain a thorn in banks’ sides.5

The COVID-19 pandemic affected the commercial real estate market as much as any, given the massive shift of commercial activities online and work from home flexibility. Lower demand for commercial real estate is apparent across all sectors, with Data Centre REITs a major exception.6 At issue is that the government programmes to support businesses, such as the CARES Act in 2020, along with loan forbearance, loan leniency, and low interest refinancing opportunities may have artificially maintained commercial real estate prices.7 As a result, prices didn’t adjust to reflect lower demand, nor did the value of U.S. banks’ loan portfolios to commercial real estate.

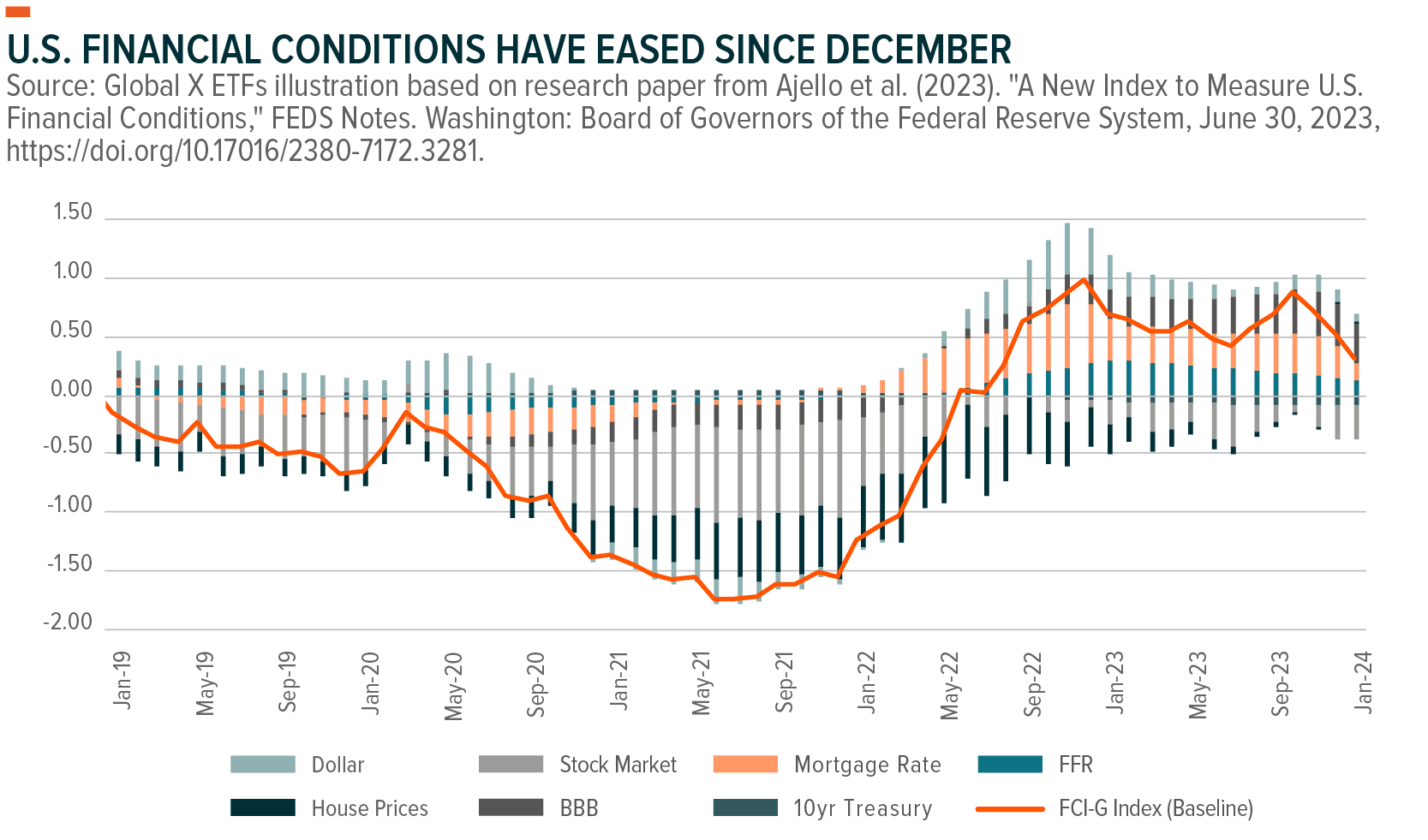

That said, the Fed’s U.S. Financial Conditions Index have declined since October last year led by strong equity performances and a decline in the 10-year US Treasury yields, suggesting that financial conditions have already eased, reducing headwinds to GDP growth.8 With inflation still above target, strong economic data and financial conditions loosening, the FOMC is unlikely to drastically revise its projections of three rate cuts for this year and could even delay its first rate cut to later this year.

Note: Positive (negative) values measure headwinds (tailwinds) to GDP growth over the next year. A reading of 1 percent above (below) the zero line means that financial conditions are a notable headwind (tailwind) to economic activity that is equivalent to a 100 basis point drag (boost) on GDP growth over the following year. The Fed’s financial index depends on the recent history of three-month changes in seven financial variables: the federal funds rate (FFR), the 10-year Treasury yield, the 30-year fixed mortgage rate, the triple-B corporate bond yield, the Dow Jones total stock market index, the Zillow house price index, and the nominal broad dollar index.

It is possible that the Fed slows down or pauses its balance sheet reductions in an effort to ensure stability in the banking system as financial institutions abandon reverse repo. Without reverse repo, the full effect of quantitative tightening would be felt, potentially resulting in higher borrowing costs and a deterioration of bank balance sheets. The current dry-out of the Fed’s overnight reverse repo facility suggests financial institutions could divert a large amount of cash from the Fed’s facility into Treasury bills, which currently yield over 5%.9

Very short Treasury bills can be an attractive destination as well, particularly with a persistently inverted Treasury yield curve. Cash holdings are likely to remain high given the strong equity market performances so far this year, and Treasury bills may help balance risk from equity allocations.

Some investors seek to reduce risk by allocating broad portfolios by region and sector. However, over the past two decades, high regional equity correlations and North American equities returning twice that of other major regions made this risk reduction strategy difficult. An advantage to using thematic ETFs is that they’re geographic and sector agnostic. They can work well as building blocks alongside regional or sector allocations while diversifying risk through companies that are typically underrepresented in broader regional benchmarks.

For example, the current U.S. macro picture points to a possible V-shaped recovery, and one may be interested in adding tactical exposures to U.S. equities and certain sectors. With the unemployment rate the lowest across Western countries, consumer demand improving in the U.S. and the UK, and inflation stagnating, sectors like Information Technology, Communication Services, Consumer Discretionary, Financials and Industrials could perform well alongside defensive sectors like Health Care.

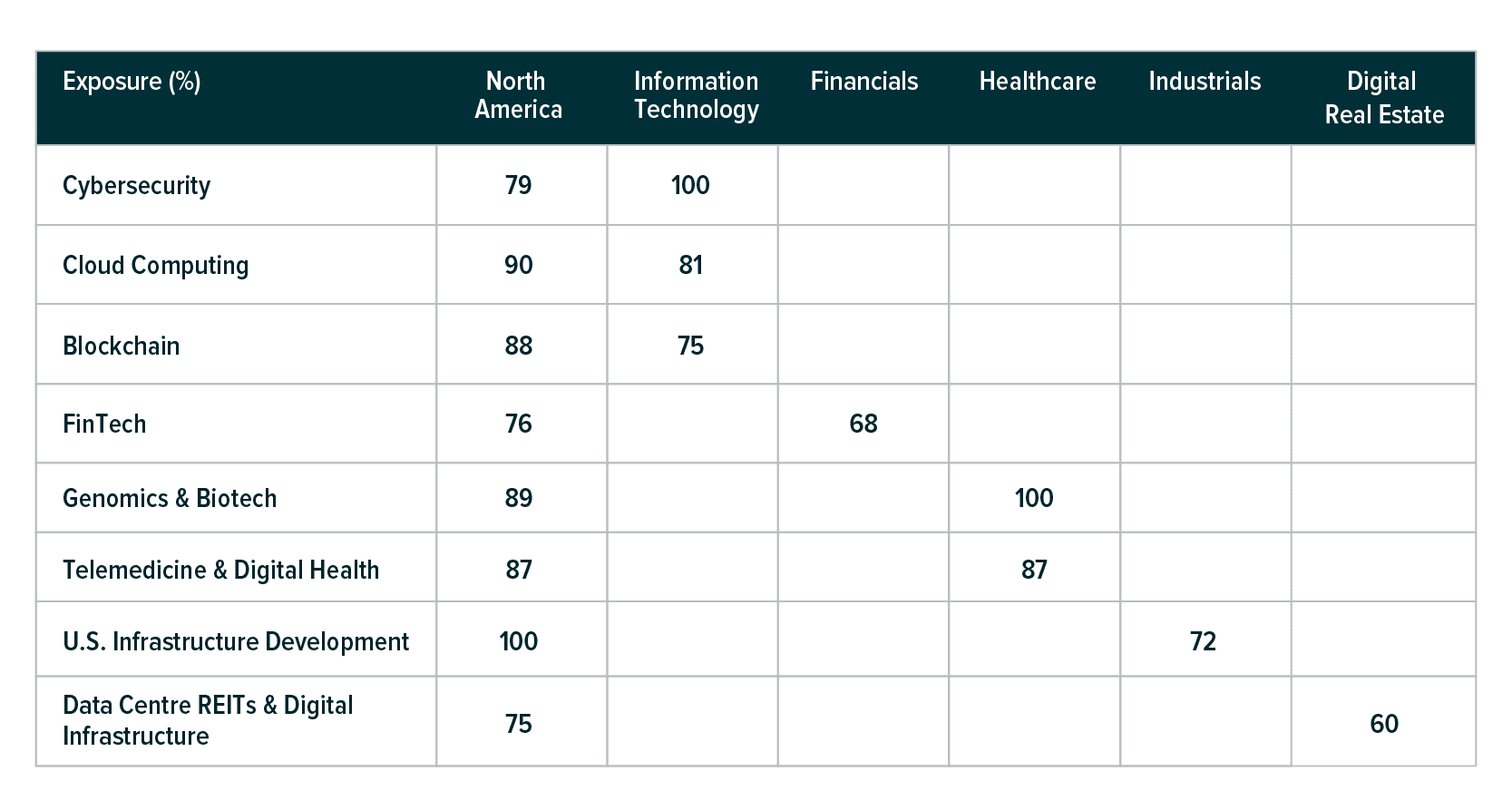

On the tactical side, Cybersecurity, Cloud Computing, Blockchain, FinTech, Genomics & Biotech, Telemedicine & Digital Health, and U.S. infrastructure Development could be useful, beyond long-term investment benefits of capturing structural trends. Also, Data Centre REITs & Digital Infrastructure stand out as potentially defensive within the real estate sector in the current environment. Demand continues to grow for data infrastructure to store, process, and distribute the data powering the digital economy and AI’s proliferation. Meanwhile, difficult operating conditions weigh on other real estate asset classes, commercial real estate in particular.

Source: Global X ETFs illustration with data derived from Morningstar as of 23 February 2024. Themes are captured through the following indices: Indxx Cybersecurity v2 Index, Indxx Global Cloud Computing v2 Index, Solactive Blockchain v2 Index, Solactive Genomics v2 Index, Solactive Telemedicine & Digital Health Index, and Indxx U.S. Infrastructure Development v2 Index, and Solactive Data Center REITs & Digital Infrastructure v2 Index.

Source: Global X ETFs illustration with data derived from Morningstar as of 23 February 2024. Themes are captured through the following indices: Indxx Cybersecurity v2 Index, Indxx Global Cloud Computing v2 Index, Solactive Blockchain v2 Index, Solactive Genomics v2 Index, Solactive Telemedicine & Digital Health Index, and Indxx U.S. Infrastructure Development v2 Index, and Solactive Data Center REITs & Digital Infrastructure v2 Index.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Personal Income and Outlays, U.S. Bureau of Economic Analysis, 29 February 2024.

2.https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20240131.pdfralreserve.gov/monetarypolicy/files/fomcminutes20240131.pdf

3. Bloomberg as of 6 March 2024.

4. https://www.federalreserve.gov/newsevents/pressreleases/monetary20240124a.htm

5. https://internationalbanker.com/technology/what-the-collapses-of-signature-bank-and-silvergate-capital-mean-for-crypto/

6. https://www.jll.co.uk/content/dam/jll-com/documents/pdf/research/global/jll-data-center-outlook-global-2024.pdf

7. https://home.treasury.gov/policy-issues/coronavirus/about-the-cares-act

8. Ajello et al. (2023). "A New Index to Measure U.S. Financial Conditions," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 30, 2023, https://doi.org/10.17016/2380-7172.3281.

9. Bloomberg as of 5 March 2024.