Europe

Corporate earnings shined in Q1. To date, roughly half of the S&P 500 companies have announced earnings results, and a large majority of them beat expectations. However, this good news may be fleeting. In April, the S&P 500 Index declined by 4.08%, and the U.S. equity benchmark’s outlook for the rest of Q2 suggests heightened volatility amid several notable tail risks.1 Included among these risks is the potential for a more hawkish Federal Reserve (Fed). Should slower growth, a still-strong labour market, and resurgent inflation combine to delay rate cuts further, pressure on earnings estimates in the coming quarters is possible. In this scenario, companies with meaningful global exposures will likely be the most vulnerable.

It is expected that U.S. equities can maintain their bullish trend this year, as long as the big tech stocks and investments in artificial intelligence (AI) remain strong, manufacturing activity maintains its current pace, and inflation doesn’t increase any further. For now, the current macroeconomic environment and strong earnings growth appear supportive for U.S. equities. For investors concerned about the potential for heightened volatility and a downturn in U.S. equity prospects, the benefits that buffer strategies can bring to a portfolio continue to be highlighted.

Investment Strategy views on S&P 500 earnings results for Q1:

U.S. GDP for Q1 disappointed with a 1.6% annualised growth rate, below consensus’ 2.5% forecast. Meanwhile, inflation came in hot with headline at 3.1% annualised and core at 3.7%.2 The higher-than-expected price pressures pushed out the prospect of a rate cut this year.

Given the trajectory of recent economic data, ‘three potential risks that could emerge for U.S equities are highlighted. First, the Fed not cutting rates this year is a real possibility. Instead, the Fed may continue to reduce its quantitative tightening (QT) to maintain ample liquidity and keep financial conditions supportive of economic growth. At its May meeting, the Fed announced plans to reduce the cap on its Treasury runoff from US$60 billion to US$25 billion starting in June. The cap on mortgage-backed securities will remain at US$35 billion.3

Second, with the Fed in no hurry to cut, the divergence between the United States and Europe is likely to increase. The European Central Bank (ECB) and the Bank of England (BoE) are likely to cut at least once this year, pushing the U.S. dollar higher against its peers. The effect of asynchronous rate cuts by the ECB or the BoE would likely lead to a strong depreciation of the Euro or the Sterling against the US dollar and other major currencies, possibly being counterproductive at trimming inflation in Europe since it would make imports more costly but will certainly improve competitiveness of the regions and boost exports. In this scenario, European equities may offer investors attractive entry points relative to their U.S. counterparts.

Third, markets digested the Fed’s higher-for-longer rates narrative amid optimism about higher future growth led by AI productivity gains. While these stocks continue to drive equities, such concentration leaves markets vulnerable to this small group of companies and prone to volatility.

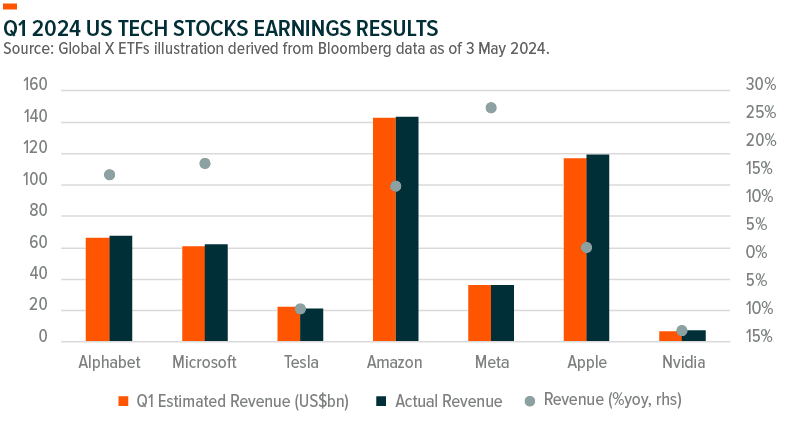

The Magnificent 7, comprising Amazon, Microsoft, Apple, Alphabet, Nvidia, Tesla, and Meta, dominated the market’s attention again this earnings season, and for good reason. Cloud services, advertising revenue and new AI developments stood out as positives. AI investments by these large tech names were scrutinised to evaluate their growth potential and whether they can sustain a broader market rally and spur new economic growth. This type of scrutiny is likely to increase in future quarters as AI proliferates. Other winners included Health Care and Consumer Staples.

Cloud Services and Advertising Boosted Revenues

Microsoft’s sales and profit exceeded expectations in Q1, lifted by corporate demand for Azure’s cloud services and OpenAI’s offerings, a sign that spending on technology is recovering from its post-pandemic lows last year. Azure revenue increased by 31%, above the average forecast for 29% and the 30% gain in Q4. About 7% of the Q1 gain was attributable to AI, compared with 6% in Q4.4

Amazon Web Services (AWS), Amazon’s cloud unit, posted its strongest sales growth in a year, a sign that the retailer’s most profitable segment is recovering from last year’s lows. Revenue for AWS increased by 17% year-over-year (YoY).5 Advertising revenue was another positive for Amazon, increasing by 24% YoY.6

Alphabet’s cloud services revenue jumped by 28% in Q1, led by its investments in AI. Search advertising revenue was up by an impressive 14% YoY. Also, Alphabet instituted a dividend worth about US$10 billion annually at the initial rate, and it announced US$70 billion of share repurchases.7

AI Even More of a Focal Point

Meta, Microsoft, and Alphabet signalled that their AI investments and generative AI-specific revenue have become key stock drivers. Microsoft’s OpenAI enabled the company to add AI tools that summarise documents and generate new content for its Microsoft Office software. Meta significantly increased its investments in AI to support product development efforts.

Global data centre infrastructure is increasingly in demand as companies race to integrate generative AI into products, services, and business operations. Amazon announced that its capital expenditures on data centres would increase significantly. All told, the company is expected to spend US$150 billion on data centres in the coming years, primarily to support AWS’ growth.8

Nvidia accelerated the development of its data centre products, recently launching four inference platforms that combine the company’s latest processors. The products expand Nvidia’s partnerships with Google Cloud, AWS, Microsoft Azure and Oracle Cloud Infrastructure. The company’s data centre revenue increased by 14% from a year ago and 18% from the previous quarter.9

Prudent Retail Spending Weighed on Discretionary Products

Amazon’s e-commerce business reported sales of $54.6 billion in Q1, slightly missing analysts’ estimates amid lower consumer spending in the more expensive product range.10 Gaming revenue for Tesla fell 8.7% YoY and Nvidia’s fell 38% YoY due to lower sales.11 Apple’s revenue rose only 2% YoY due to concerns about elongated sales cycles.12

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Bloomberg as of 30 April 2024

2. US Bureau of Economic Analysis

3. Federal Reserve issues FOMC statement

4. FY24 Q1 - Press Releases - Investor Relations - Microsoft

5. Amazon.com, Inc. - Amazon.com Announces First Quarter Results (aboutamazon.com)

6. Ibid.

7. GOOG Exhibit 99.1 Q1 2024 (abc.xyz)

8. Amazon.com, Inc. - Amazon.com Announces First Quarter Results (aboutamazon.com)

9. NVIDIA Corporation - NVIDIA Announces Financial Results for First Quarter Fiscal 2024

10. Amazon.com, Inc. - Amazon.com Announces First Quarter Results (aboutamazon.com)

11. Tesla Releases First Quarter 2024 Financial Results | Tesla Investor Relations. NVIDIA Corporation; - NVIDIA Announces Financial Results for First Quarter Fiscal 2024

12. Apple reports first quarter results - Apple