Europe

Marketing Communication. Capital at risk. For Professional Investors Only.

Amid rising macroeconomic and geopolitical uncertainties, some investors may be increasingly reassessing traditional asset allocation approaches. As equity markets face potential downside risks, and fixed income continues to struggle as a reliable diversifier, interest in alternative income strategies, such as defined outcome options and covered calls, appears to be growing.1,2 Simultaneously, the rapid expansion of artificial intelligence is contributing to rising energy demand, which could pressure ageing infrastructure and increase interest in scalable, low-emission energy sources like nuclear.3 In commodities, ongoing trade disputes and supply constraints may heighten the strategic importance of critical minerals, while oil markets face potential headwinds from both supply increases and fluctuating global demand.4,5 Precious metals, particularly gold, could see continued interest as investors seek hedges against inflation and economic uncertainty.6

Key takeaways:

Income Section

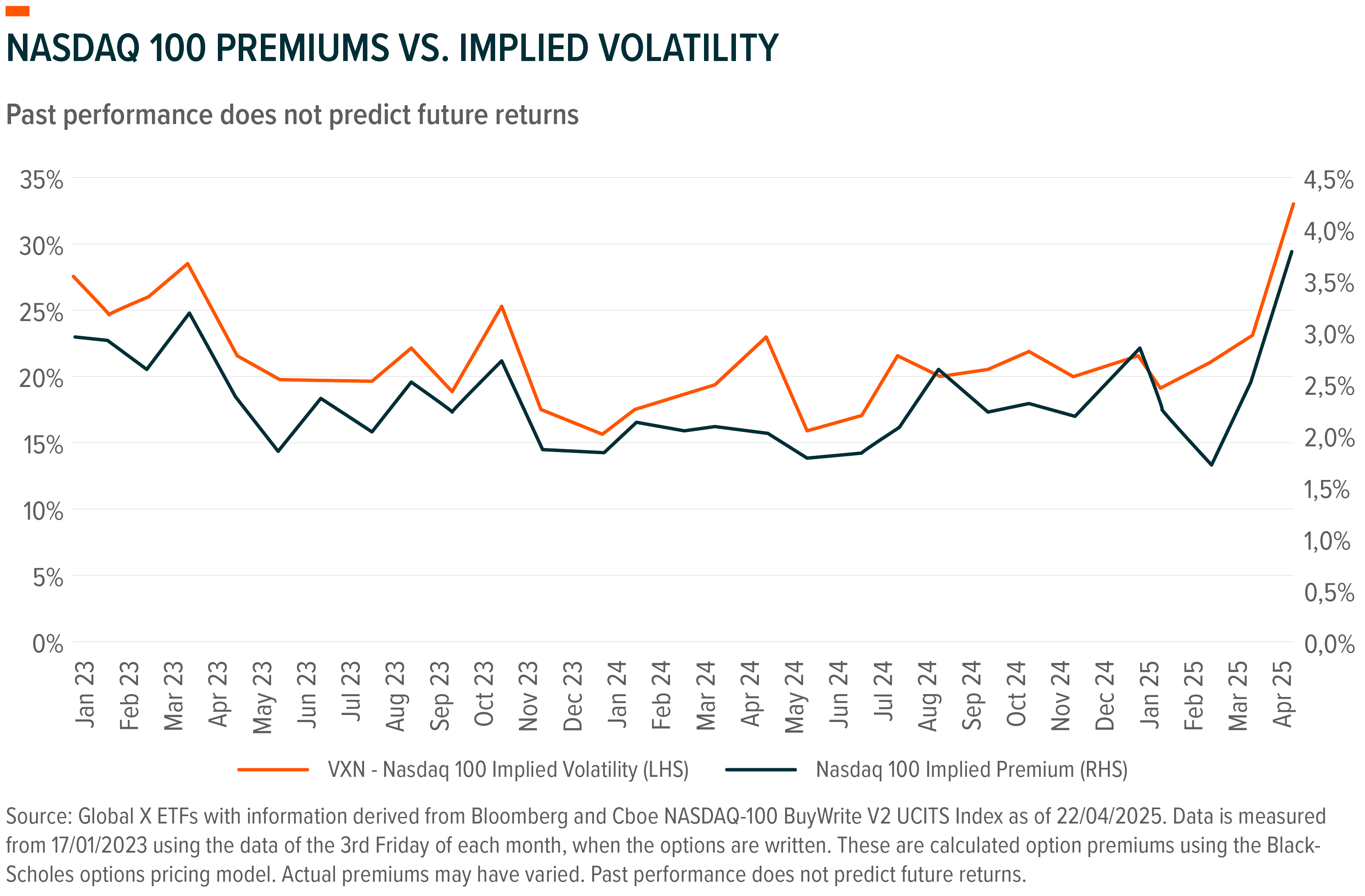

Buffering The Downside – Potentially Managing Further Equity Risk Through Defined Outcome Option Strategies

While US exceptionalism endures due to the strength of its companies, market risks are rising, particularly with growing political interference in institutions like the Fed.7 While economic data has cooled, reflected in the mildly negative economic surprise index, there are no strong signals pointing to an imminent recession.8 Earnings expectations have stayed broadly flat, even as underlying growth shows signs of softening.9 Instead, tariffs have been the key drag on equities year to date, compressing valuations, particularly in technology.10 However, a weakening US dollar, potential continued re-rating of US equities valuations, and a steepening yield curve due to ongoing budget deficits and persistent inflation all possibly suggest a volatile period ahead.11

In such an environment low beta and/or volatility reducing strategies such as defined outcome option-based strategies may help to buffer further equity downside risks whilst offering capped upside participation.

In fixed-income markets, yield curves have steepened, driven by lower trade deficits and persistently high budget deficits.12 This trend reflects mounting inflationary pressure, which potentially challenges the traditional diversification role of treasuries in portfolios.13 Despite expectations, Treasuries may have failed to provide the expected hedge, with 10-year yields remaining surprisingly stable through part of April.14 Federal Reserve Chair Jerome Powell’s recent comments reinforced the view that there is no imminent policy pivot, potentially further limiting upside for bonds.15 In such an environment, the 60/40 portfolio might not have provided the hedge some expected. There is a possible case to be made for long duration bonds in the event of a recessionary scenario; however, with inflation potentially rising in the long term as currently signalled by long term inflation swaps and the bearish re-steepening of the yield curve, these might not provide the hedge and steady income within a portfolio that some investors are aiming for.16

Thematic Section

AI Growth May Drive Rising Energy Demand and Focus on Nuclear

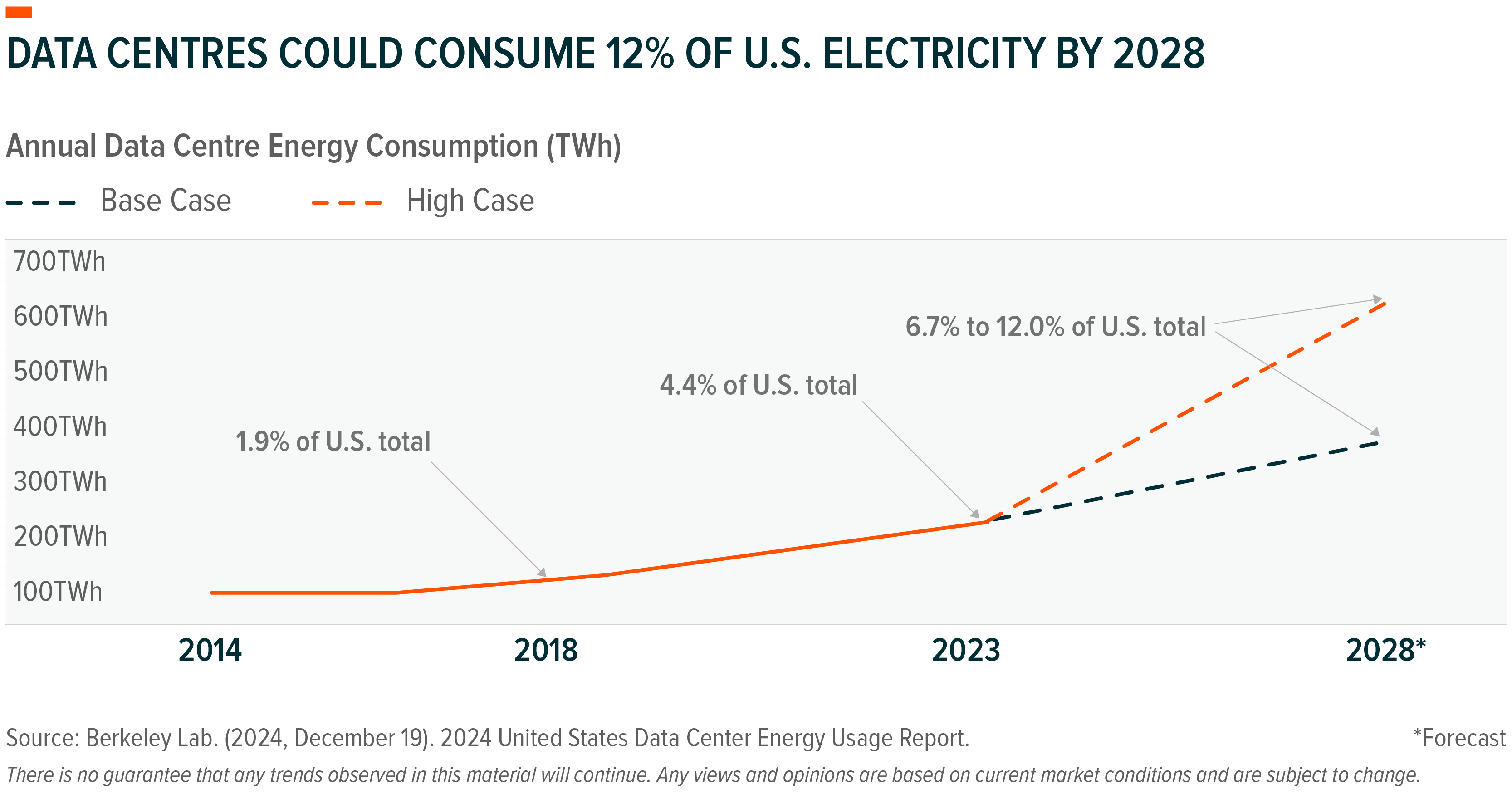

The rapid advancement of artificial intelligence (AI) has introduced capabilities from natural language understanding and autonomous reasoning, to complex pattern recognition.17 Yet behind these breakthroughs could lie a mounting energy demand. Training frontier models such as GPT-4 requires approximately 50 gigawatt-hours of electricity, enough to supply over 6,000 U.S. households for one year.18 The investment into artificial intelligence continues to increase: the ‘big 4’ hyperscalers reported $246 billion in combined capital expenditure in 2024, compared to $151 billion in 2023.19 As AI shifts from model training to real-time inferencing, energy consumption is increasing in aggregate. A single AI-generated query can consume ten times the power of a traditional web search, and complex inferencing tasks, such as video generation, are significantly more intensive.20 ,21 Looking forward, the emergence of agentic systems—Nvidia CEO Jensen Huang recently noted that the amount of computation needed was “easily 100 times more than we thought we needed last year.22 The trajectory is clear: AI’s growth is intrinsically linked to an extraordinary expansion in electricity usage.

This surge in energy demand possibly presents a profound challenge to existing infrastructure. By 2028, U.S. data centres may account for up to 12% of national electricity consumption, while overall utility demand is projected to rise by nearly 50% by 2040.23, 24, 25These demands are testing the limits of an ageing electrical grid, much of which was constructed over half a century ago.26 Transmission backlogs and permit delays have further constrained expansion, particularly in high-growth states like Virginia, which alone accounts for over a quarter of U.S. data centre energy use.27,28 In response, attention is turning toward nuclear energy, particularly next-generation solutions such as small modular reactors (SMRs).29 Governments and private firms alike are positioning nuclear as a critical enabler of clean, scalable base-load power. The United States has committed to expanding nuclear capacity by 35 gigawatts within the next decade, with legislative support through the bipartisan “Advance Act”.30 With electricity demand for data centres potentially tripling by 2030 in Europe, European countries including France, Finland, and Sweden are advocating for nuclear energy’s inclusion in the continent’s decarbonisation agenda.31,32 As AI-driven innovation intensifies, the energy systems and infrastructure that sustain it must evolve at a comparable pace.

Commodities Section

Trade Disputes and Export Curbs May Raise the Stakes in Critical Minerals Markets

Amid escalating trade tensions, China has imposed export restrictions on seven rare earth elements in retaliation for U.S. tariffs.33 While China's imports from the U.S. remain limited, its dominance in critical mineral production means these restrictions could significantly tighten global supply.34 Notably, neodymium and praseodymium—key to magnet manufacturing—were excluded, likely to preserve leverage for future controls.35

These export curbs, combined with broader trade frictions, may lead to medium-to-long-term price increases for critical minerals.36 Although short-term fluctuations are possible if global economic growth slows, sustained geopolitical uncertainty could pressure markets upward.37

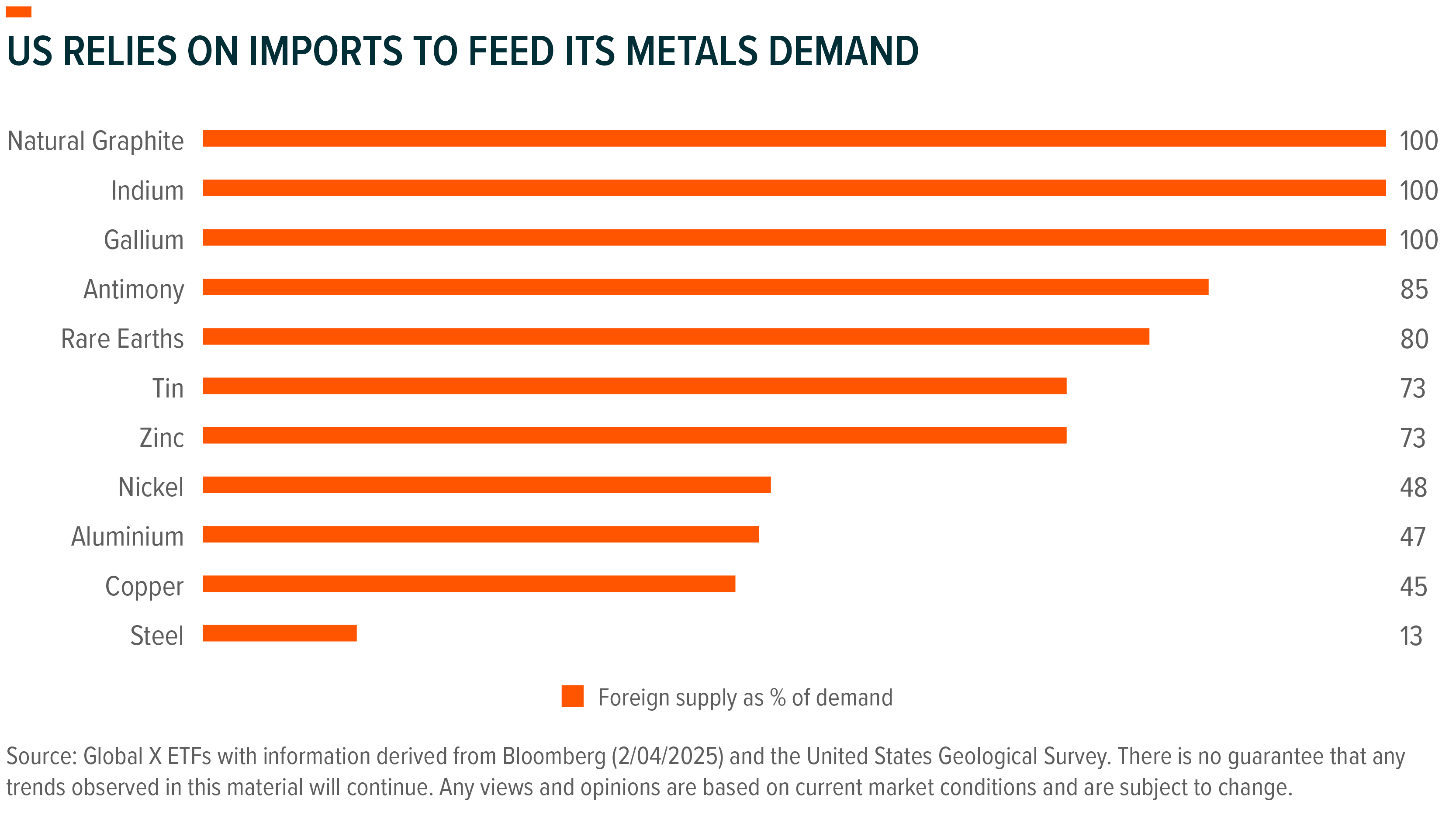

China mines and processes roughly 61% and 92% of the world’s rare earths and plays a major role in the supply of gallium, germanium, and antimony.38,39 Past behaviour suggests it may use these controls strategically.40 Given China's heavy involvement in these markets, further tightening could disrupt global supply chains and delay shipments.

The United States is particularly exposed, importing 70% of its rare earths from China.41 This dependency raises the risk of domestic bottlenecks and inflationary pressures in critical sectors.

In response, President Donald Trump issued an executive order under Section 232 of the Trade Expansion Act, launching a probe into whether U.S. reliance on imported critical minerals threatens national security.42 The investigation seeks to address vulnerabilities in sectors like semiconductors and defence and reflects a broader shift toward reshoring supply chains and reducing reliance on strategic adversaries.43

Oil market fundamentals seem to be turning bearish, as trade tensions, weak demand, and rising supply may pressure prices.44 Worries of a global economic slowdown, and that the trade turmoil could impact oil demand, may continue amid further escalation of Donald Trump’s trade war.45

The Trump administration’s policies could continue to inject uncertainty into the oil market.46 On one hand, the administration’s goal to increase domestic oil and gas production by 3 million barrels per day by 2028 could further exacerbate a supply glut.47 Conversely, some measures could tighten the markets, such as further sanctions or restrictions on Venezuela, Iran, and Russia’s oil flows. 48 49 50

On the supply side, OPEC, the key player in balancing global oil supply, continues to impact the market. In a surprise announcement on 3rd April, they said they would add more than 400,000 barrels per day back into the global market, a supply boost three times larger than previously signalled, potentially further pressuring oil fundamentals.51

At the same time, precious metals' role as a potential hedge against economic uncertainty could continue to support their value in the next months. Markets continue to favour ‘safe-haven’ assets such as gold and silver amid geopolitical tensions, particularly with the US trade war, which has triggered a significant dollar weakening.52

Additionally, fears of stagflation in the US, where inflation risks are rising while economic growth slows, have potentially made gold and silver more attractive as possible inflation hedges.53 Indeed, central banks have been accumulating gold for example, in March, the People's Bank of China continued its five-month streak of adding gold to reserves.54 Not only did central banks' demand increase, but retail investors in China poured billions into gold-backed exchange-traded funds amid rising trade tensions.55

However, in times of financial stress, investors may sell gold to meet margin calls or to fill gaps in their equity portfolios, especially after its significant gains earlier this year.56 This could explain short-term pullbacks in gold prices. Indeed, gold’s vulnerability to profit-taking may be high after a historic rally; however, the positive structural view remains intact.57

As crosscurrents from geopolitics, evolving technology, and market volatility continue to shape the investment environment, portfolios may benefit from a more adaptive and diversified approach. Alternative income strategies could offer a buffer against equity drawdowns, particularly in scenarios where bonds underperform their historical hedging role. The rise of AI and its associated energy needs may prompt greater focus on the future of power generation, particularly in areas like nuclear. Commodities are becoming increasingly influenced by political and strategic developments, with rare earth supply dynamics and oil market imbalances potentially contributing to further price instability. Meanwhile, gold may retain its role as a potential hedge during periods of heightened uncertainty. These shifts suggest a landscape where flexibility, prudence, and awareness of evolving macro trends could be key to managing risk and uncovering opportunities.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

Bloomberg (03/04/2025) Gold’s Drop to Prove Fleeting in Stagflation Backdrop