Europe

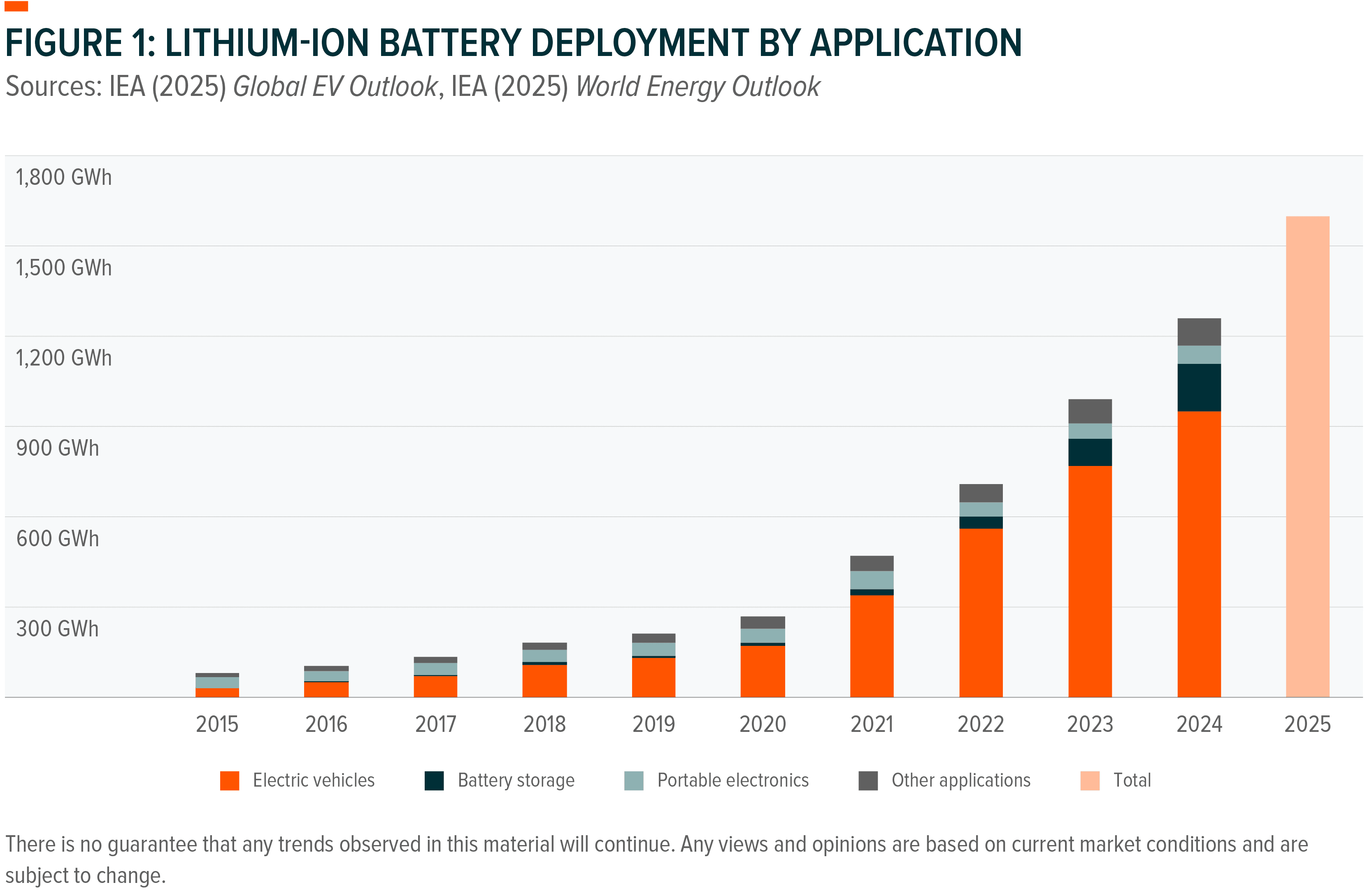

Lithium and battery technology are emerging as critical inputs in the current phase of global power expansion.¹ Incremental electricity demand from AI data centres, electrification and grid resilience is outpacing long-lead supply (eg. nuclear), creating a near- and medium-term capacity gap.² The fastest scalable solution has been to deploy renewable generation paired with batteries, a shift that redirecting lithium demand away from cyclical EV sales, towards more structural Energy Storage Systems (ESS).³,⁴

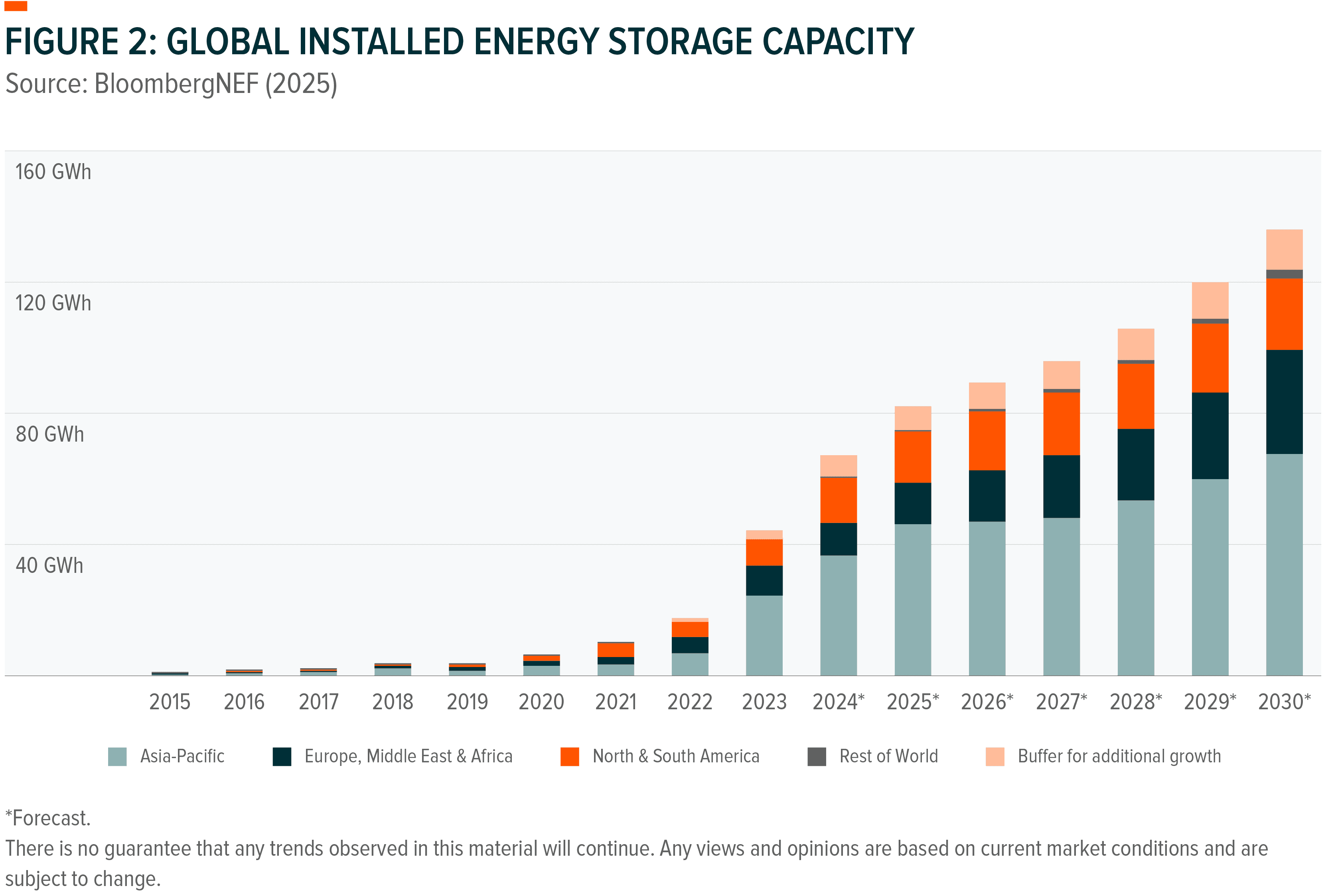

As renewables scale, ESS have provided a practical way to manage intermittent power generation, enhancing grid reliability and stability.⁵,⁶ As a result, storage has moved from a discretionary add-on toward a repeatable component of grid investment, supporting a more durable, infrastructure-like demand profile for lithium and battery technology.⁷

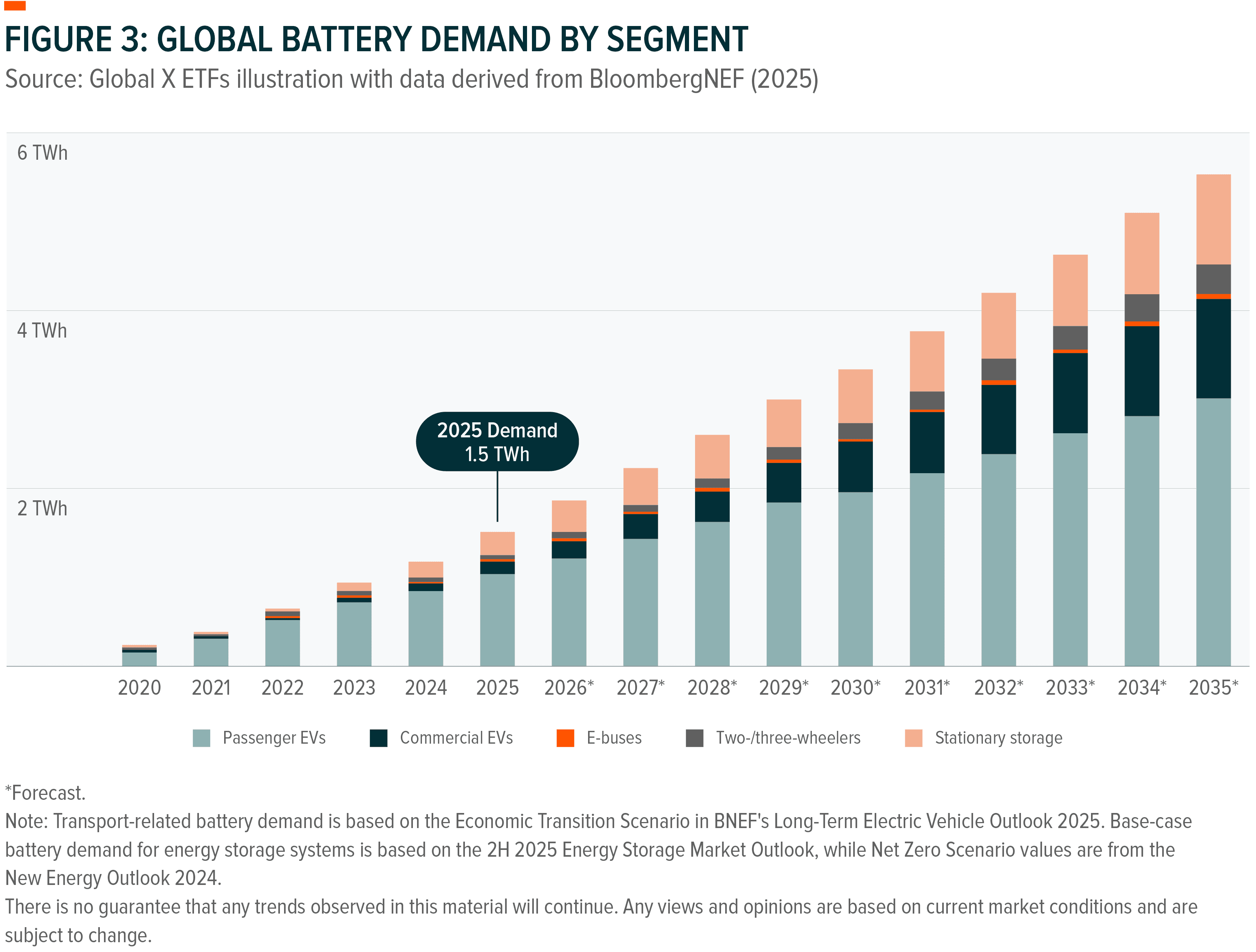

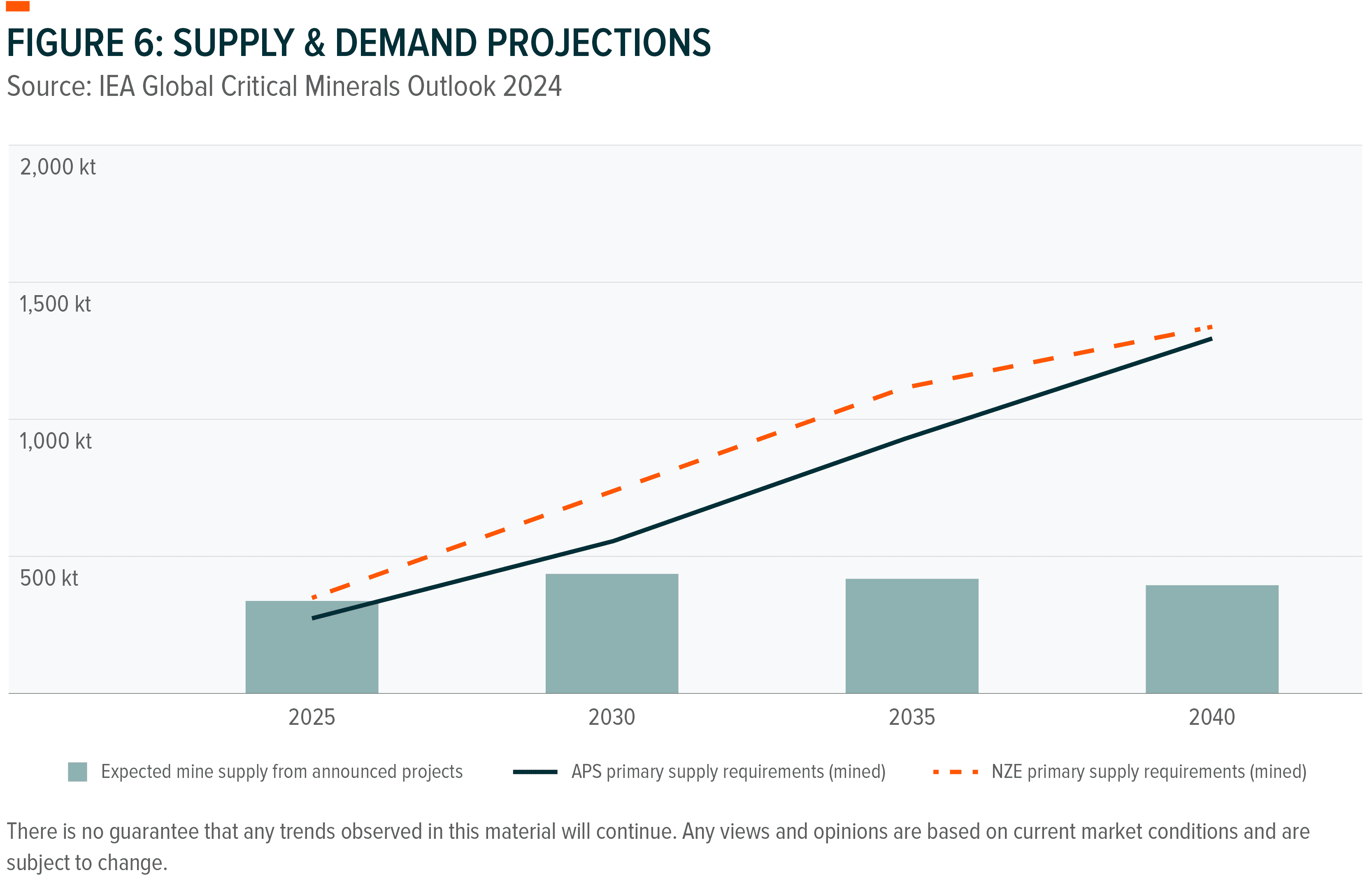

The investment opportunity spans the value chain. Lithium markets are small relative to the capital flowing into grids, making prices sensitive to supply discipline, favouring low-cost miners and integrated chemicals producers.⁸,⁹ Concurrently, battery cells and control software have benefited from the scaling of storage deployments.¹⁰ Diversified exposure across mining, processing and battery technology captures the full power-system build-out, rather than relying on any single segment.¹¹

Unlike EVs, ESS demand is not capped by fleet size or replacement cycles. As power systems evolve, grids can keep adding storage to manage higher renewable shares, peak loads and resilience requirements, reinforcing structural, non-saturating demand.¹⁷

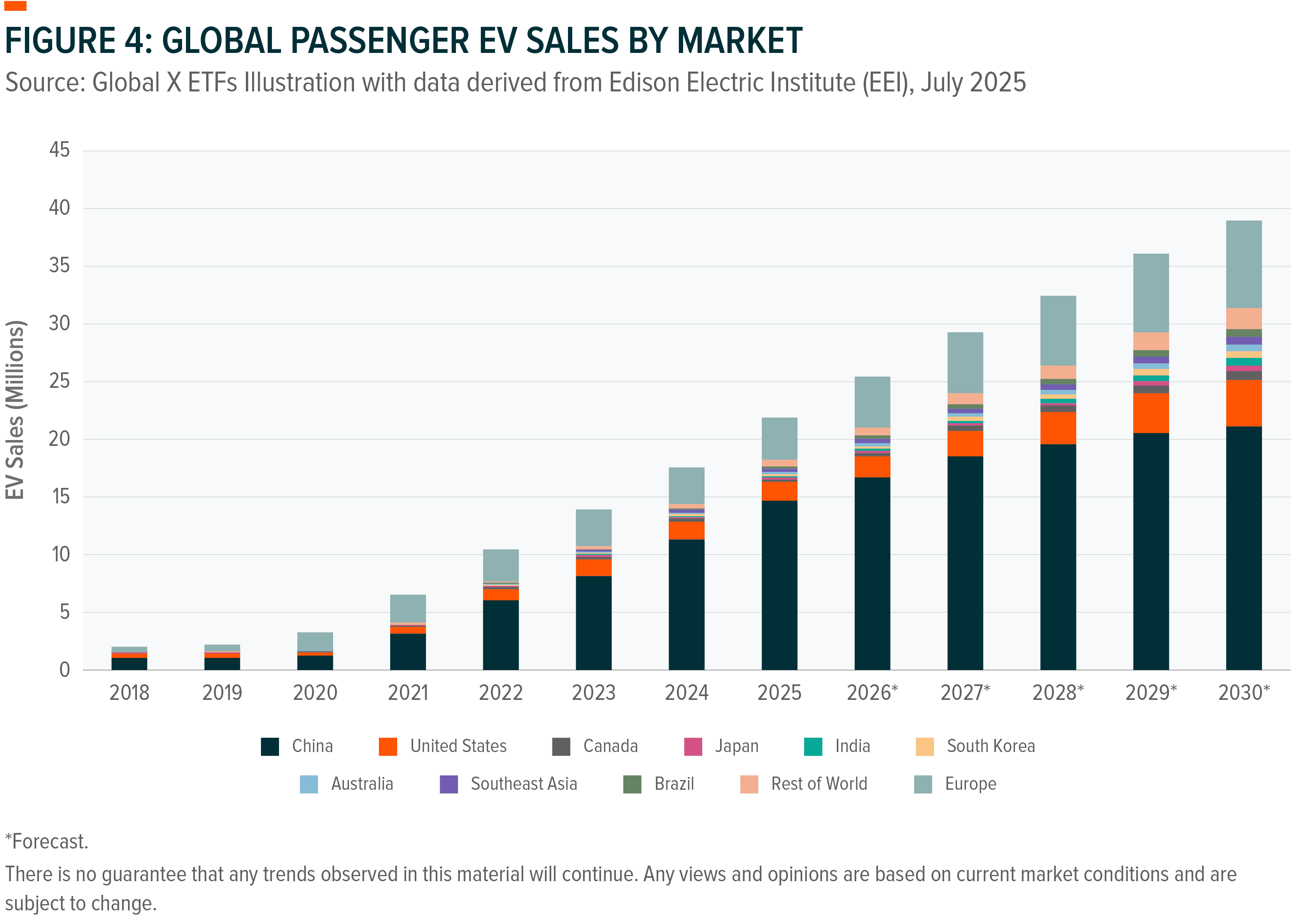

EV adoption remains a multi-decade transition rather than a one-cycle theme. Fleet turnover is slow, replacement demand compounds over time, and emerging markets remain underpenetrated relative to developed markets.²³ While EV demand is more cyclical than ESS, it continues to provide a large, growing base-load of lithium consumption.²⁴

As storage shifts from discretionary to repeatable grid investment, lithium demand may become increasingly tied to infrastructure deployment rather than consumer-led adoption cycles.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1 International Energy Agency (IEA) (2025) The Role of Critical Minerals in Clean Energy Transitions

2 IEA (2024) – Electricity 2024: Analysis and Forecast to 2026

3 BloombergNEF (2025) – Lithium-Ion Batteries: State of the Industry 2025 (v1.2)

4 BloombergNEF (2H 2025) – Energy Storage Market Outlook

5 BloombergNEF (2024) – Global Energy Storage Market Review

6 IEA (2023) – Grid Integration of Renewables

7 BloombergNEF (2025) – New Energy Outlook 2025

8 IEA (2025) – Global Critical Minerals Outlook 2025

9 Benchmark Mineral Intelligence (2024) – Lithium Cost Curve & Incentive Pricing

10 BloombergNEF (2025) – Battery Price Survey

11 IEA (2024) – Net Zero Roadmap Update

12 IEA (2024) Energy and AI (2024)

13 IEA (2025) World Energy Investment

14 International Renewable Energy Agency (IRENA) (July 2025) Renewable Power Generation Costs

15 IRENA (2024) Electricity Storage Valuation Frameworks

16 Benchmark Mineral Intelligence (2025) Lithium demand by end-use

17 Ibid

18 IEA (2025) IEA Global EV Outlook 2025

19 IEA (2025) World Energy Investment 2025

20 Bloomberg Data (Accessed February 2026)

21 Bloomberg (2024) Does Switching Your Gas Guzzler for an EV Make Financial Sense?

22 McKinsey & Company (December 2024) The battery chemistries powering the future of electric vehicles

23 OECD (2024) Global EV Outlook 2023

24 BloombergNEF (2019) Will the Real Lithium Demand Please Stand Up? Challenging the 1Mt-by-2025 Orthodoxy

25 IEA (2025) Batteries and Secure Energy Transitions

26 IEA (2024) IEA Renewables 2024

27 International Renewable Energy Agency (IRENA) (July 2025) Renewable Power Generation Costs in 2024

28 IEA (2024) Batteries and Secure Energy Transitions

29 Ibid

30 BloombergNEF (2025) Energy Storage Market Outlook

31 IEA (2025) Digitalisation and Energy

32 Ibid

33 Reuters (July, 2025) Global energy investment set to hit record $3.3 trillion in 2025, IEA says

34 Discovery Alert (November, 2025) China’s Lithium Rally Sparks Global Supply Chain Transformation

35 Reuters (June, 2025) Rio Tinto bets lithium will retain its battery metal crown

36 US Department of Energy (2025) Loan support and critical minerals strategy

37 Lithium Americas (2025) Building industrial-scale battery-grade lithium carbonate production capacity at Thacker Pass