Europe

Marketing Communication. Capital at risk. For Professional Investors Only. Please read fund legal documentation before making any final investment decisions.

The infrastructure of capital markets is evolving. For decades, buying, selling and settling financial assets has relied on a patchwork of intermediaries, siloed ledgers and settlement cycles measured in days. That system works, but it is slow, opaque, and expensive, particularly in private markets where manual processes and high minimum ticket sizes shut out all but the largest investors.

Blockchain appears to be filling the gap. The world’s largest financial institutions are adopting shared, cryptographically secured digital ledgers as core plumbing. Two applications sit at the centre of this shift: stablecoins, which provide a digital cash layer, and tokenisation, which provides a digital asset layer. Together, they may compress settlement times, extend market hours and widen access to asset classes long reserved for institutions.

A stablecoin is a digital asset pegged to a reference currency, most commonly the US dollar, and backed one-for-one by cash or short-term liquid assets such as Treasury bills. Stablecoins hold a fixed value and function as programmable, blockchain-native money, enabling near-instant settlement and low-cost cross-border transfers. Tether (USDT) is currently the largest stablecoin, with a market capitalisation of approximately $184 billion, followed by Circle’s USDC at approximately $78 billion.⁸

Tokenisation is the process of issuing a digital representation of an asset, such as a bond, a fund share or a piece of real estate, on a blockchain. The token is the asset’s record of ownership, transferred and settled on a shared ledger. This means faster settlement, greater transparency and the ability to fractionise assets previously accessible only in large denominations.⁹

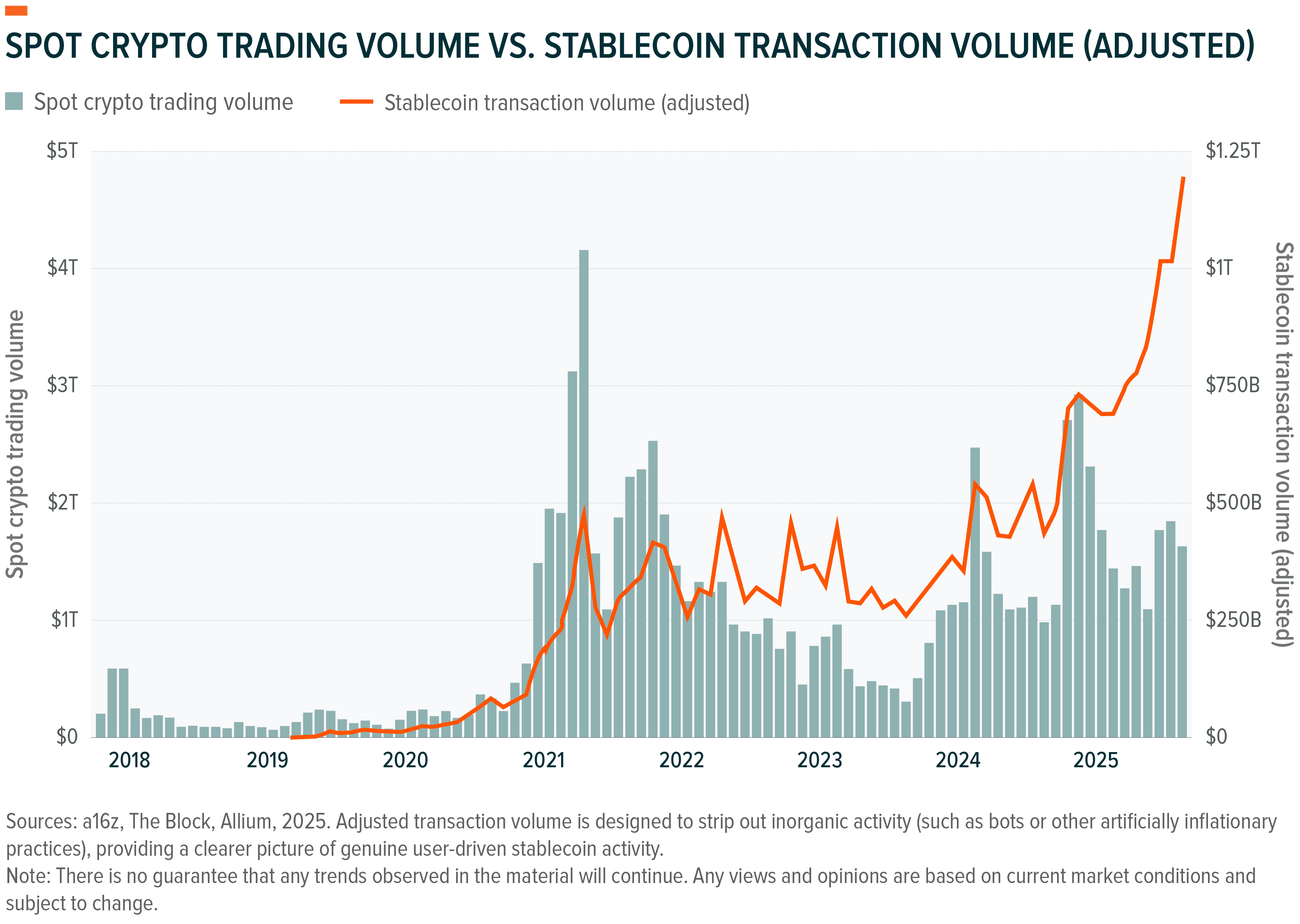

The growth figures tell a clear story. The total market capitalisation of stablecoins rose from $28 billion in 2020 to over $320 billion by early 2026.¹⁰,¹¹ Adjusted annual transfer volume reached approximately $11 trillion in 2025, a figure that now rivals legacy settlement networks.¹² Monthly transfer volumes more than doubled in a single year, from $1.9 trillion in February 2024 to $4.1 trillion in February 2025, while active stablecoin wallet addresses grew 53% over the same period, from 19.6 million to 30 million.¹³ There are now more than 500 million unique wallet addresses globally.¹⁴

Most stablecoin activity today still centres on cryptocurrency trading. The IMF estimates that approximately 80% of stablecoin transactions involve bots and automated systems used for arbitrage and portfolio rebalancing.¹⁵ However, the use case mix appears to be shifting, demonstrated by the decoupling of stablecoin transaction volume and spot crypto trading volume.¹⁶ Cross-border payments are growing rapidly, particularly in emerging markets. In Latin America, 71% of survey respondents used stablecoins for cross-border payments.¹⁷ The economics are compelling; stablecoin remittances could cut fees by up to 60% compared with traditional bank transfers, and settlement happens in seconds rather than days.¹⁸ Corporate treasury operations are another expanding use case, with adoption of stablecoins for working capital and supply-chain settlement rising by approximately 25% in 2025.¹⁹ Visa and Mastercard have begun settling card obligations in USDC on-chain, embedding stablecoins into mainstream payment rails.²⁰

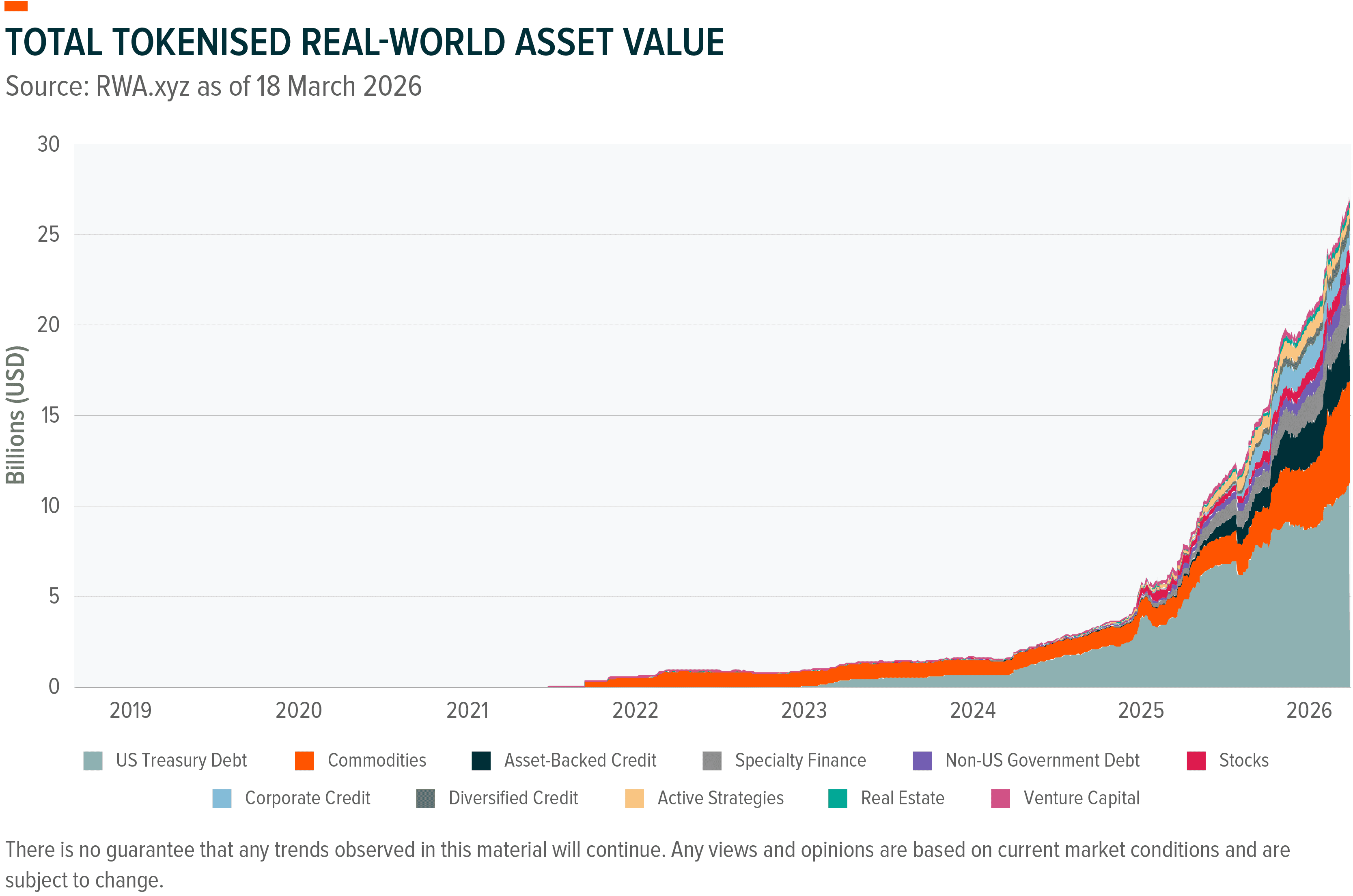

Tokenised assets are on a similar trajectory, if smaller in absolute terms. The on-chain value of real-world assets (excluding stablecoins) grew from approximately $1 billion at end-2022 to $21.4 billion at end-2025, a more-than-twentyfold increase in three years.²¹ Tokenised US Treasuries was the largest segment, followed by commodities and institutional alternative funds.²² The number of individual holders of tokenised RWA assets increased more than sevenfold in 2025, reaching nearly 550,000.²³ Projections for 2030 vary, from $2 trillion at the conservative end to $16 trillion, but all point in the same direction.²⁴,²⁵

Major financial institutions have moved well beyond pilots. BlackRock launched its tokenised Treasury fund, BUIDL, in March 2024.²⁶ It surpassed $1 billion in assets within a year and exceeded $2.5 billion by late 2025.²⁷,²⁸ It now operates across eight blockchain networks and serves as trading collateral on Binance.²⁹

Franklin Templeton launched the first US-registered mutual fund on a public blockchain in 2021 and has since adapted two further money market funds for blockchain distribution and stablecoin reserves under the GENIUS Act.³⁰ JPMorgan launched a tokenised money market fund on Ethereum in December 2025.³¹ Securitize, the platform behind BUIDL, also works with Apollo, Hamilton Lane and KKR amongst other companies. ³²,³³,³⁴ Globally, there have also been discussions between banks to launch stablecoins. Several US banks were in discussions to launch a joint stablecoin.³⁵ Closer to home, nine major European banks, including ING, Unicredit and CaixaBank, announced a consortium in late 2025 to launch a euro-denominated stablecoin.³⁶

Institutional capital usually follows regulatory clarity. Two frameworks matter most.

The GENIUS Act, signed into law on 18 July 2025, is the first comprehensive US federal framework for stablecoins.³⁷ It requires issuers to back payment stablecoins one-for-one with dollars or low-risk liquid assets, mandates licensing through federal or state regulators, and subjects issuers to Bank Secrecy Act obligations.³⁸ The Office of the Comptroller of the Currency published proposed implementing rules in February 2026, with the regime expected to take full effect by January 2027 at the latest.³⁹,⁴⁰ With the framework now in place, U.S. regulators are expected to clarify capital requirements, custody standards, and cross-border oversight. The developments could accelerate global policy alignment and increase institutional participation in stablecoin.

The Markets in Crypto-Assets (“MiCA”) Regulation became fully applicable on 30 December 2024, establishing uniform EU-wide rules for crypto-asset issuers and service providers.⁴¹ Its stablecoin provisions require full liquid-asset backing and mandatory audits.⁴²,⁴³ Alongside MiCA, the EU's DLT Pilot Regime provides a sandbox for trading and settling tokenised securities on distributed ledgers.⁴⁴ In December 2025, the Commission proposed raising the issuance threshold from €6 billion to €100 billion and expanding eligible asset classes.⁴⁵

Tokenised funds are experiencing significant growth. BCG estimates they could reach $600 billion in AUM by 2030, a trajectory comparable to the early growth of ETFs.⁴⁶ Money market funds are leading, with total on-chain AUM exceeding $10 billion by end of January 2026.⁴⁷

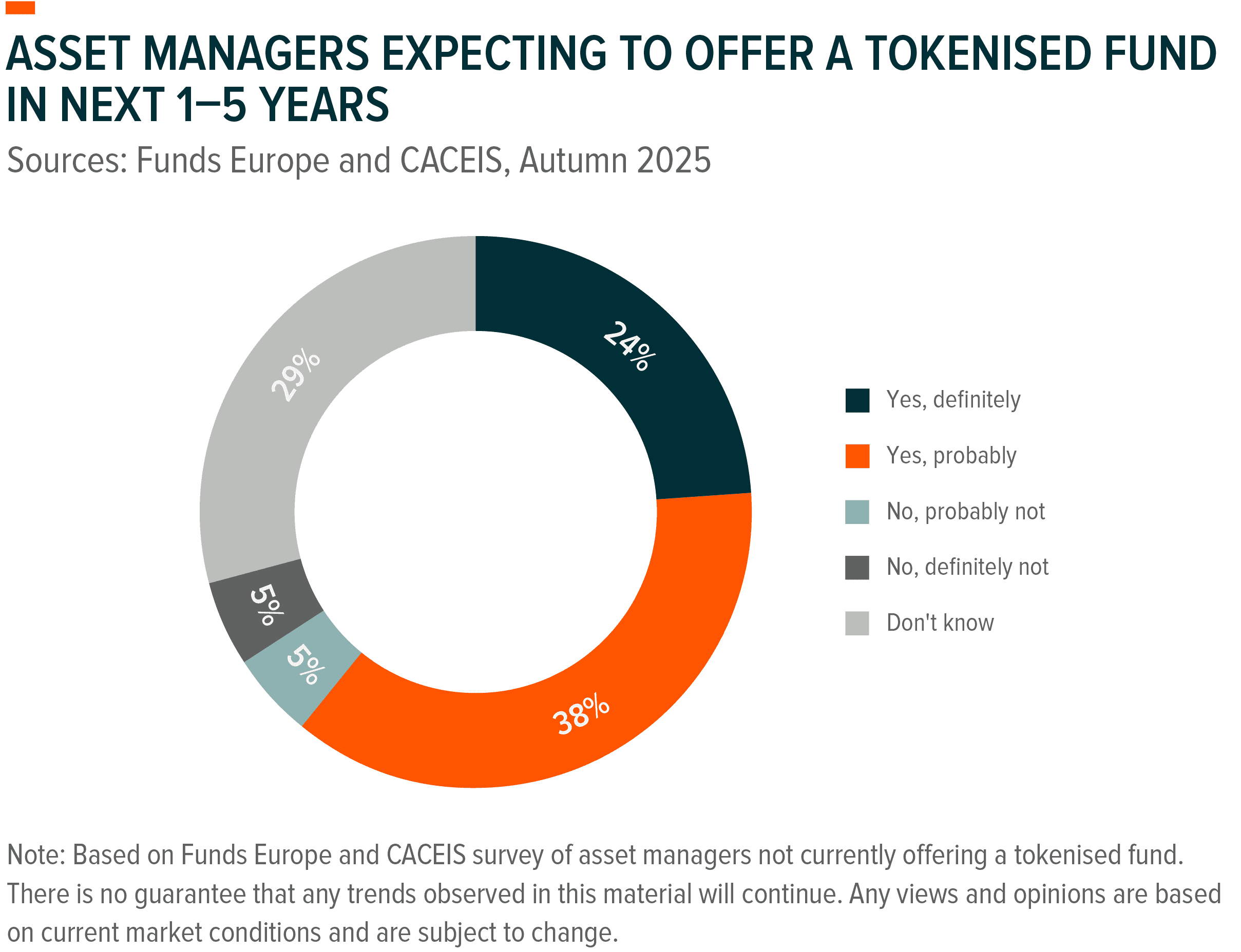

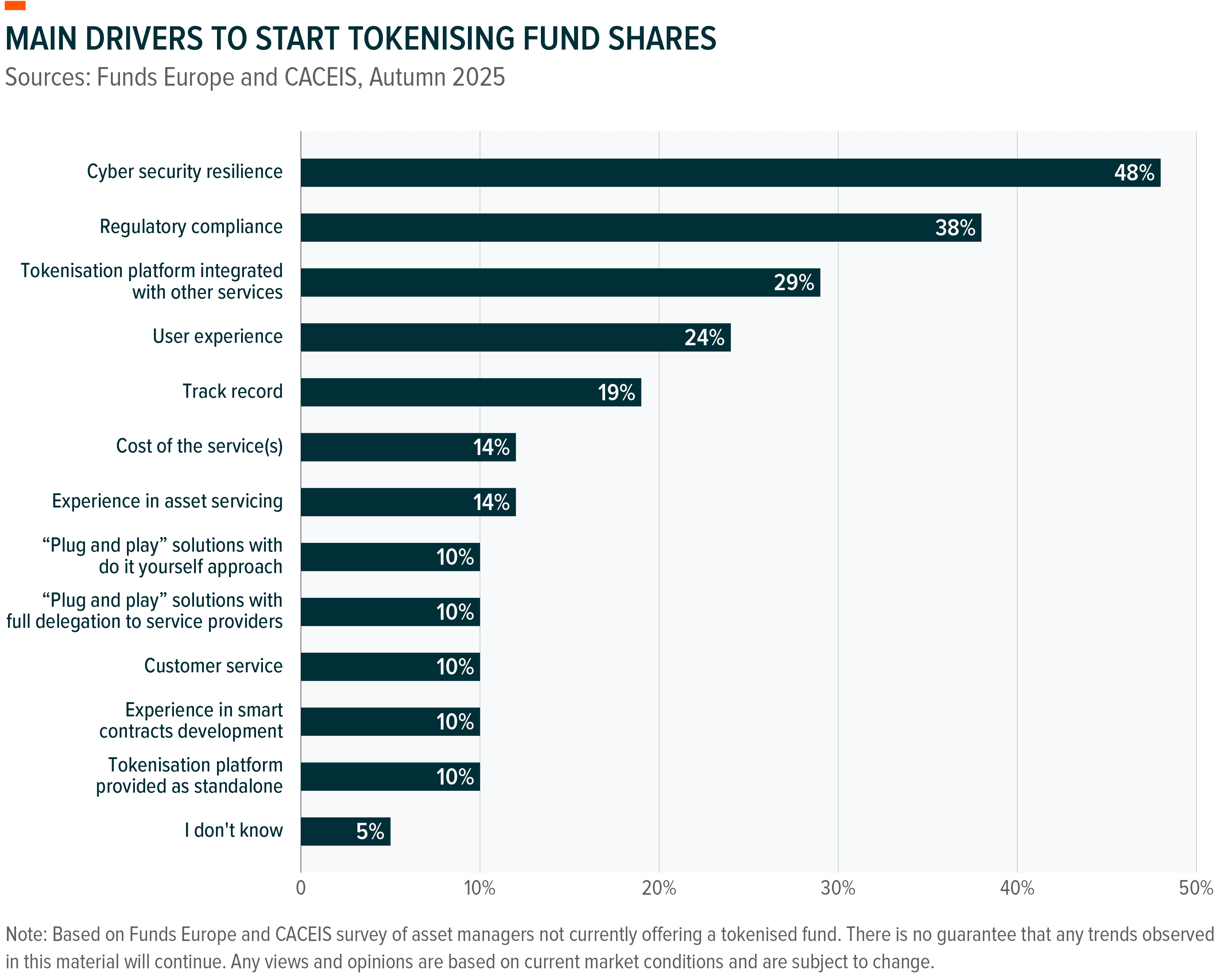

Fund managers are preparing accordingly. The Funds-Europe-CACEIS Digital Assets Survey found that 62% of asset managers without a tokenised fund expect to launch one within five years, with over half citing anticipated investor demand as the primary driver.⁴⁸ Among asset owners, 88% describe demand as moderate or high.⁴⁹

For investors, the practical implications of stablecoins and tokenisation are worth spelling out.

Access is the most obvious change. Private credit, real estate, and alternative funds have traditionally required minimum constraints of $1 million or more, locking out smaller allocators and limiting diversification. Tokenisation enables fund shares to be divided into smaller units, lowering entry thresholds considerably. ADDX, a private market exchange backed by SGX, already offers tokenised fund shares with minimum as low as $10,000.⁵⁰ Hamilton Lane and KKR have both issued tokenised feeder funds through Securitize, opening access to institutional-grade private equity strategies that were previously out of reach for most investors.⁵¹,⁵²

Efficiency is the second. Tokenised funds can pay dividends daily, rather than monthly, settle transactions near-instantly rather than on T+1 or T+2 cycles, and operate 24/7. BlackRock’s BUIDL fund, for example, pays daily yield from its underlying Treasury holdings and allows 24/7 peer-to-peer transfers.⁵³ Fund tokens can also serve as collateral for trading; a feature already live on Binance and other venues.⁵⁴

Liquidity is the third, though it comes with caveats. Tokenised assets can in principle trade on secondary markets at any hour. In practice, secondary liquidity remains thin outside money market funds and Treasuries.⁵⁵ Investors should assess redemption terms and market depth.

The Mirae Asset Stablecoins and Tokenisation UCITS Index, which is tracked by the Global X Stablecoin and Tokenisation UCITS ETF, seeks to provide diversified exposure the growth of companies that derive meaningful economic exposure from tokenised asset markets. The index provides exposure to four key sub-themes in this space:

Stablecoins and tokenisation have moved from theory to practice. The world’s largest asset managers are already running tokenised funds, while the US and EU have built legislative frameworks to support the development of stablecoins and tokenisation. While stablecoins and tokenisation are currently a small fraction of global financial markets, the infrastructure is still developing, and the institutional commitment is growing. This is worth watching closely.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Macquarie Group, Stablecoins are Starting to Reshape Payments and Banking. 10 March 2026.

2. Ibid.

3. RWA.xyz data, Accessed 30 March 2026.

4. Funds Europe & CACEIS, Digital Assets Survey. February 2026.

5. Congress.gov, S.1582 — GENIUS Act. 18 July 2025.

6. European Securities and Markets Authority, Markets in Crypto-Assets Regulation. 2024.

7. Ledger Insights, EU Commission Floats Major DLT Pilot Regime Upgrade. 4 December 2025.

8. Macquarie Group, Stablecoins are Starting to Reshape Payments and Banking. 10 March 2026.

9. McKinsey, From Ripples to Waves: The Transformational Power of Tokenizing Assets. 20 June 2024.

10. Citi GPS, Stablecoin 2030. April 2025.

11. CryptoTicker, Stablecoin Market Cap Hits $320 Billion as Institutional Adoption Goes Vertical. 15 March 2026.

12. Macquarie Group, Stablecoins are Starting to Reshape Payments and Banking. 10 March 2026.

13. Artemis & Dune, The State of Stablecoins 2025: Supply, Adoption & Market Trends. 19 March 2025.

14. Transak, Global Money Movement Report 2025. 2025.

15. IMF, Understanding Stablecoins. 2025.

16. A16z, State of Crypto 2025: The year crypto went mainstream. 22 October 2025.

17. Fireblocks, State of Stablecoins 2025. 2025.

18. Transak, Global Money Movement Report 2025. 2025.

19. CoinLaw, Stablecoin Market Share by Chain Statistics 2025. September 2025.

20. Macquarie Group, Stablecoins are Starting to Reshape Payments and Banking. 10 March 2026.

21. RWA.xyz data, Accessed 30 March 2026.

22. Ibid.

23. Ibid.

24. McKinsey, From Ripples to Waves: The Transformational Power of Tokenizing Assets. 20 June 2024.

25. BCG/ADDX, Relevance of On-chain Asset Tokenization in 'Crypto Winter'. September 2022.

26. Securitize, BUIDL Surpasses $1B in AUM. 13 March 2025.

27. Ibid.

28. CoinDesk, BlackRock’s $2.5B Tokenized Fund Gets Listed as Collateral on Binance. 14 November 2025.

29. Fortune, BlackRock’s $2.5 Billion Tokenized Money Market Fund Gets Boost with Binance Tie-Up. 14 November 2025.

30. Franklin Templeton, Tokenized money market funds: The bridge to a new financial infrastructure. 9 June 2025.

31. J.P. Morgan Asset Management, J.P. Morgan Asset Management Launches Its First Tokenized Money Market Fund. 15 December 2025.

32. Securitize, Hamilton Lane’s $2.1B Fund Now Available on Securitize. 31 January 2023.

33. Securitize, BUIDL Surpasses $1B in AUM. 13 March 2025.

34. Fortune, BlackRock’s $2.5 Billion Tokenized Money Market Fund Gets Boost with Binance Tie-Up. 14 November 2025.

35. Wall Street Journal, Big Banks Explore Venturing Into Crypto World Together With Joint Stablecoin. 22 May 2025.

36. ING, Nine major European banks join forces to issue stablecoin. 25 September 2025.

37. Congress.gov, S.1582 — GENIUS Act. 18 July 2025.

38. Ibid.

39. OCC, Bulletin 2026-3: GENIUS Act Regulations. 25 February 2026.

40. Sullivan & Cromwell, GENIUS Act Implementation: OCC Issues Proposed Rules. 17 March 2026.

41. European Securities and Markets Authority, Markets in Crypto-Assets Regulation. 2024.

42. Ibid.

43. Norton Rose Fulbright, Regulating Crypto-Assets in Europe: Practical Guide to MiCA. 2024.

44. European Securities and Markets Authority, DLT Pilot Regime. 2026.

45. Ledger Insights, EU Commission Floats Major DLT Pilot Regime Upgrade. 4 December 2025.

46. BCG, Tokenized Funds: The Third Revolution in Asset Management Decoded. 29 October 2024.

47. RWA.xyz, Global Market Overview. Accessed 30 March 2026.

48. Funds Europe & CACEIS, Digital Assets Survey. February 2026.

49. Ibid.

50. BCG/ADDX, Relevance of On-chain Asset Tokenization in 'Crypto Winter'. September 2022.

51. Securitize, Securitize Launches Fund for Tokenized Exposure to KKR. 13 September 2022.

52. Securitize, Hamilton Lane’s $2.1B Fund Now Available on Securitize. 31 January 2023.

53. Securitize, BUIDL Surpasses $1B in AUM. 13 March 2025.

54. Fortune, BlackRock’s $2.5 Billion Tokenized Money Market Fund Gets Boost with Binance Tie-Up. 14 November 2025.

55. McKinsey, From Ripples to Waves: The Transformational Power of Tokenizing Assets. 20 June 2024.