Europe

Pharmaceutical giants face an unusual problem: too much capital, not enough time. Between 2026 and 2030, roughly 190 branded drugs will lose patent protection, erasing up to an estimated $400 billion in annual sales.¹ The typical response to this problem is that internal R&D takes too long. Internal R&D takes a decade on average but patents start expiring in 2026, so Big Pharma is buying innovation instead of developing it, and it is what they are buying which has fundamentally changed.²

The $12 billion Novartis paid for Avidity Biosciences wasn’t for a single drug.³ It was for RNA delivery infrastructure, a platform that could generate multiple therapies across different diseases.⁴ Pharmaceutical companies are no longer just backfilling pipelines with late-stage assets but acquiring the technologies that are reshaping how medicine works, from AI-driven drug discovery, liquid biopsy platforms, genomic sequencing at scale to neuroscience and rare disease portfolios.⁵

2025 saw the first patient treated with a personalised gene based-editing therapy (CRISPR) designed specifically for his unique mutation in just six months.¹¹ The FDA subsequently outlined regulatory pathways for such “N-of-1” therapies, validating the shift toward individualised genetic medicine.¹² This may represent a convergence of three critical breakthroughs that appear to be reshaping the pharmaceutical industry.

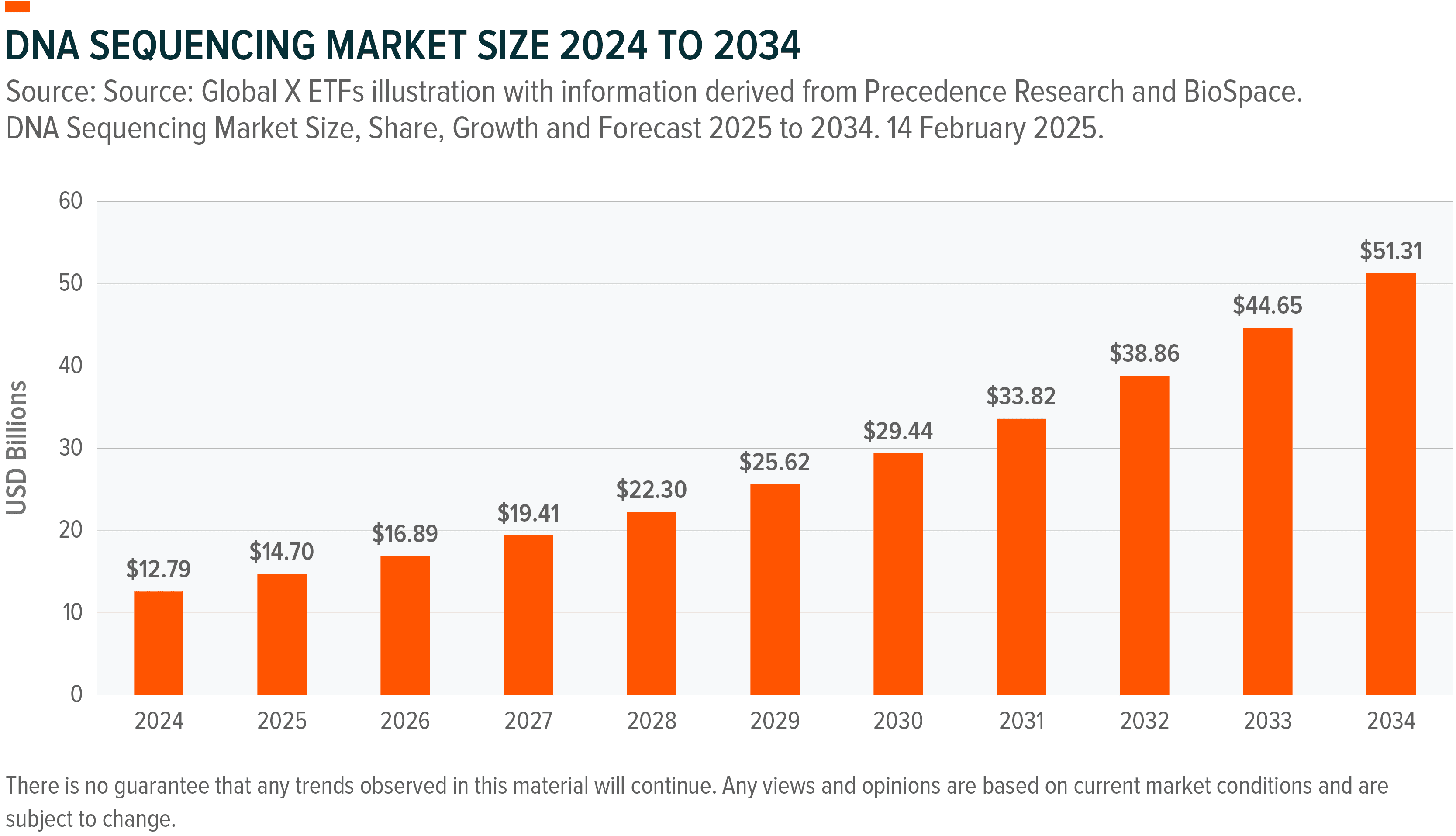

The foundation was economic. When Illumina’s NovaSeq X series crossed the sub-$200 genome threshold in 2023, genetic sequencing transformed from a research tool into something scalable for everyday medicine.¹³

Illumina controls over 80% of the next-generation sequencing market, and its December 2025 partnership with MyOme targeting the Million Person Health Trial, combines genetic sequencing with AI models to predict disease onset 5-10 years before symptoms appear.¹⁴,¹⁵ Economic models suggest this preventive approach could save over $200 billion annually in US healthcare costs.¹⁶

But sequencing data is only as valuable as the sample behind it. Several companies are making breakthroughs in this area. Qiagen’s tools turn raw tissue and blood samples into actionable data. Its QIAseq panels profile tumours and blood cancers comprehensively, powering companion diagnostics for more than 15 FDA‑approved targeted therapies.¹⁷ Bio-Techne supports the next layer of discovery, supplying reagents for genomics and proteomics that accelerate drug development and diagnostics research.¹⁸ Its focus on spatial biology and single-cell analysis, boosted by the Lunaphore acquisition, lets scientists map 100+ biomarkers in a single tissue section, revealing how cells interact in ways traditional tests cannot.¹⁹Together, these companies form the infrastructure on which the precision medicine is built.

That infrastructure also unlocked a parallel transformation in diagnostics. Illumina’s sequencing technology made liquid biopsy viable at scale: instead of invasive tissue samples, doctors can now analyse tumour DNA fragments shed into the bloodstream through a simple blood draw.²⁰,²¹,²² The technology detects genetic changes across an entire genome from a single sample, something that would have been impossible with older, slower, and more expensive sequencing methods.

Clinical adoption is accelerating. In June 2025, the FDA granted Breakthrough Device designation to Guardant Health’s Shield test, which detects early-stage cancers across multiple types with 87% accuracy.²³ For patients already undergoing treatment, Natera’s Signatera platform monitors tumour DNA levels in the blood to track whether therapy is actually working.²⁴ The platform distinguishes tumour DNA from normal cellular debris through advanced computational analysis, giving oncologists a real-time view of disease status without repeated biopsies.²⁵

Natera sharpened this capability further with its December 2025 acquisition of Foresight Diagnostics, which brought technology that increased detection sensitivity tenfold.²⁶ That means earlier detection of recurrence, often before traditional imaging would catch it.

While CRISPR permanently edits genes, RNA therapeutics offer a more flexible approach. Rather than rewriting the genetic blueprint, they modulate how that blueprint is expressed, allowing treatment to be tuned over time.²⁷ The technology comes in two forms:

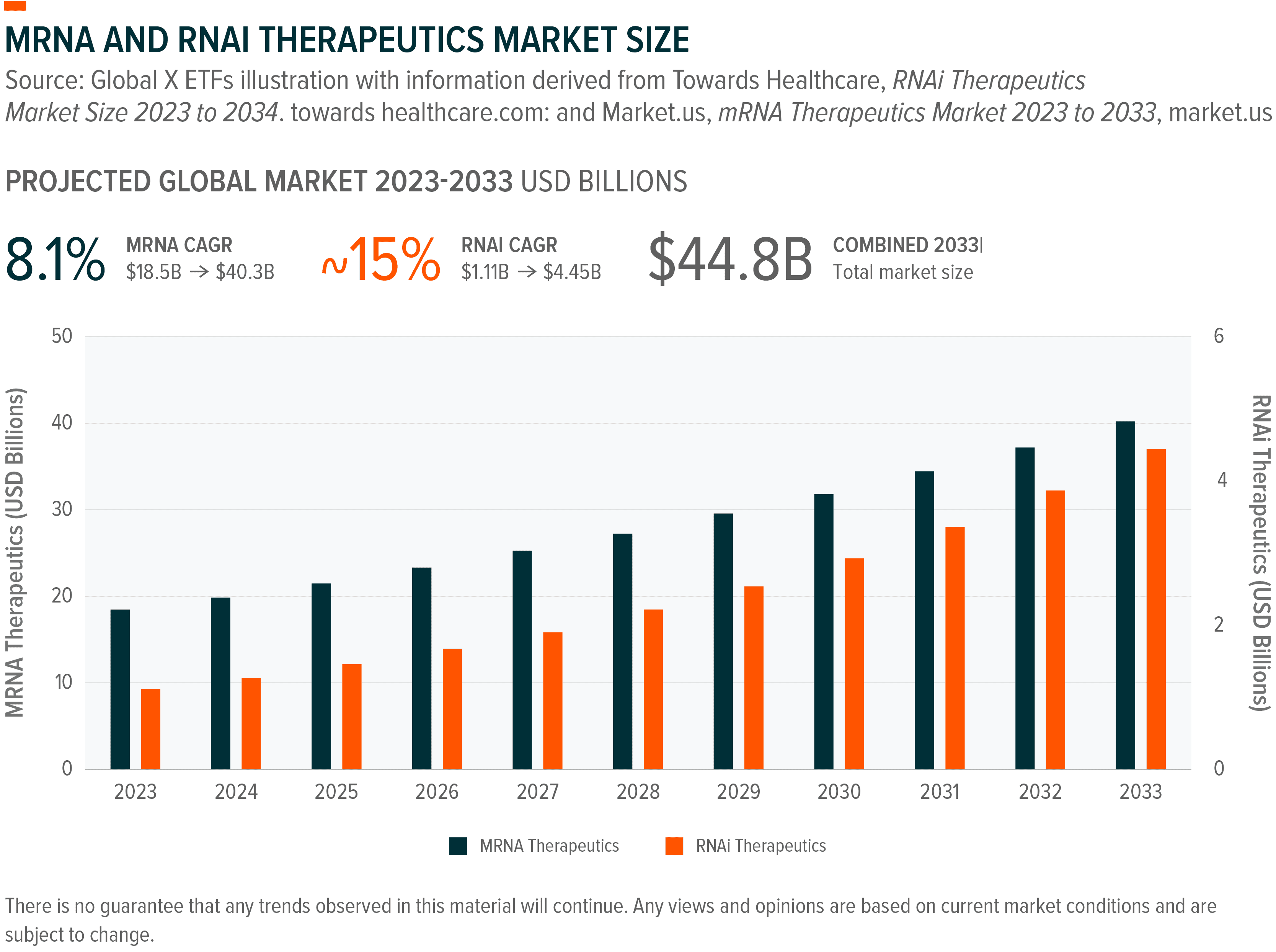

Validated by COVID-19 vaccines, mRNA technology is now expanding into cancer and rare diseases. Instead of editing genes, it delivers temporary instructions for cells to produce specific proteins.²⁸ Moderna has personalised cancer vaccines in Phase 3 trials, with melanoma (skin cancer) data expected in H1 2026.²⁹ Analysts project the global mRNA market size to reach north of $30 billion by 2030, growing at a CAGR of 17% from 2023 base levels.³⁰

RNA Inference (RNAi) works the opposite way by shutting down disease-causing genes before they can produce harmful proteins.³¹ November 2025 marked a turning point, when Arrowhead Pharmaceuticals received FDA approval for Redemplo (plozasiran), its first approved product.³² The drug treats a rare genetic disease affecting approximately 6,500 US patients who have dangerously high triglyceride levels (a type of fat found in blood) that can cause life-threatening complications.³³ In clinical trials, the treatment reduced triglycerides by 80%.³⁴ The approval triggered rapid global expansion, with China approving the drug in January 2026, followed by Health Canada.³⁵ More importantly, the FDA granted Breakthrough Therapy designation in December 2025 for the same drug to treat millions of patients worldwide with severe triglyceride elevation.³⁶

The first patient case demonstrated what’s possible under gene editing technology, but it also exposed the central challenge: personalised genetic medicine only works if it can scale beyond one-off heroic interventions. Traditional CAR-T cancer therapy costs over $500,000 per patient and requires weeks of specialised manufacturing, limiting it to the most severe cases.³⁷

The industry is now pivoting toward “in vivo” approaches where genetic modifications happen directly inside the patient’s body rather than in a laboratory, dramatically reducing both time and cost.³⁸ Companies like REGENXBIO are developing long-acting gene therapies that act as ‘biofactories’ inside the body which are designed to deliver sustained therapeutic benefit from a single administration, replacing the need for repeated treatment.³⁹

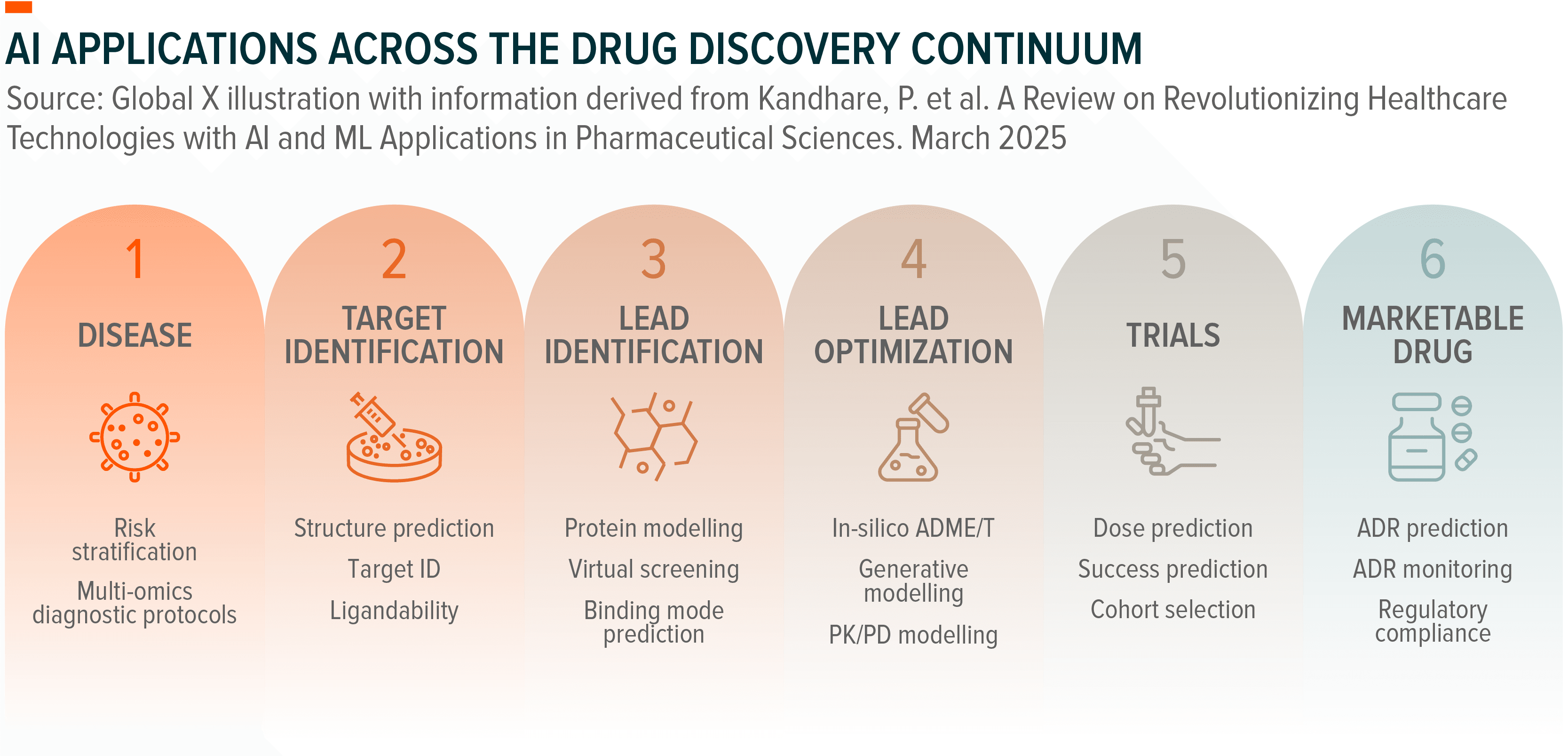

By 2025, AI had moved from experimental promise to a validated drug discovery platform.⁴⁰ The first Phase 2a results from fully AI-designed molecules showed clinical efficacy, and from virtually no AI-designed drugs in trials in 2020, dozens had entered human testing by mid-2025, with progression rates comparable to traditional discovery.⁴¹,⁴² A prime example is Insilico Medicine, a Boston-based company that uses AI to pursue a treatment for idiopathic pulmonary fibrosis (IPF), a deadly disease that ravages lung tissue with thick, stiff scars.⁴³ One AI system identified a previously unknown protein involved in causing the disease; a second designed a molecule to block it.⁴⁴ That molecule became a drug named rentosertib, which has since shown promising safety and efficacy results in early human trials reported last June.⁴⁵,⁴⁶

This kind of timeline compression is emerging as the defining pattern across the industry. Moderna employs machine learning to optimise mRNA sequences for stability and immunogenicity, cutting candidate selection from 18 months to 6 months.⁴⁷ Illumina’s DRAGEN platform uses AI to reduce 30-hour whole genome analysis to under 30 minutes.⁴⁸ Guardant Health and Natera deploy AI models that distinguish tumour-derived DNA from background noise, achieving sensitivity improvements of 3-5x over conventional methods.⁴⁹ Vertex uses computational chemistry and machine learning to predict small molecule interactions, accelerating lead optimisation for cystic fibrosis and pain therapies.⁵⁰ The applications vary but the underlying dynamic is consistent, in that AI is collapsing timescales that were previously fixed.

Pharmaceutical companies have responded by building infrastructure. GPU-based supercomputers purpose-built for drug discovery began coming online in early 2026.⁵¹ Eli Lilly partnered with NVIDIA to launch TuneLab, an end-to-end AI platform designed to accelerate molecular discovery and compress drug development cycles that currently average ten years.⁵² They aren’t alone, with multiple companies now integrating AI throughout their discovery platforms.⁵³

Scaling these capabilities, however, depends on solving persistent data problems. Publicly available structural biology databases contain gaps and errors that limit model precision, and proprietary industry datasets have historically remained siloed.⁵⁴ The AI Structural Biology Network (AISB) represents one attempt to change this through a federated collaboration where major biopharmaceutical companies pool proprietary structural biology data to train AI models while keeping each partner’s data confidential.⁵⁵ Major biopharmaceutical companies, including Bristol Myers Squibb and AstraZeneca, pool proprietary structural biology data to train shared AI models while keeping each partner’s data confidential.⁵⁶,⁵⁷ Designed specifically for drug development rather than basic research, AISB uses federated learning to train AI models on pooled proprietary industry data, with OpenFold3 as its flagship model.⁵⁸

Even the most precisely discovered therapies, though, cannot reach patients without a corresponding revolution in manufacturing. The industry has begun to address this through what it calls Bioprocess 5.0, where it integrates AI, automation, and digital twins (virtual simulations of production environments) to manufacture complex biologics with unprecedented consistency and speed.⁵⁹ Rather than relying on trial-and-error, AI optimises manufacturing parameters in real time, while digital simulations allow changes to be tested without risking actual production runs. As personalised therapies expand from individual patients to broader populations, this infrastructure becomes essential, resolving the same manufacturing bottleneck that once severely limited the early rollout of CAR-T therapy.⁶⁰

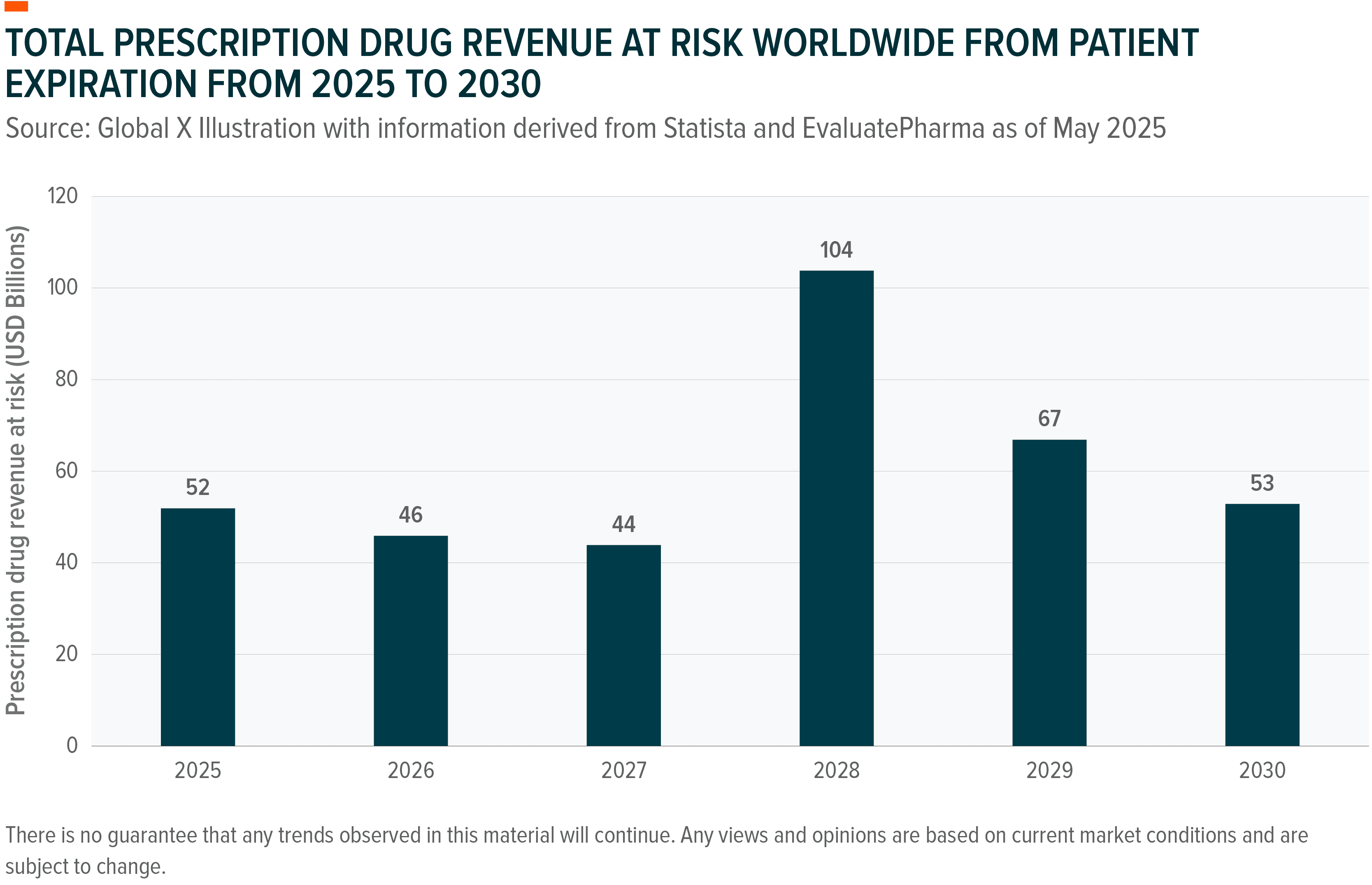

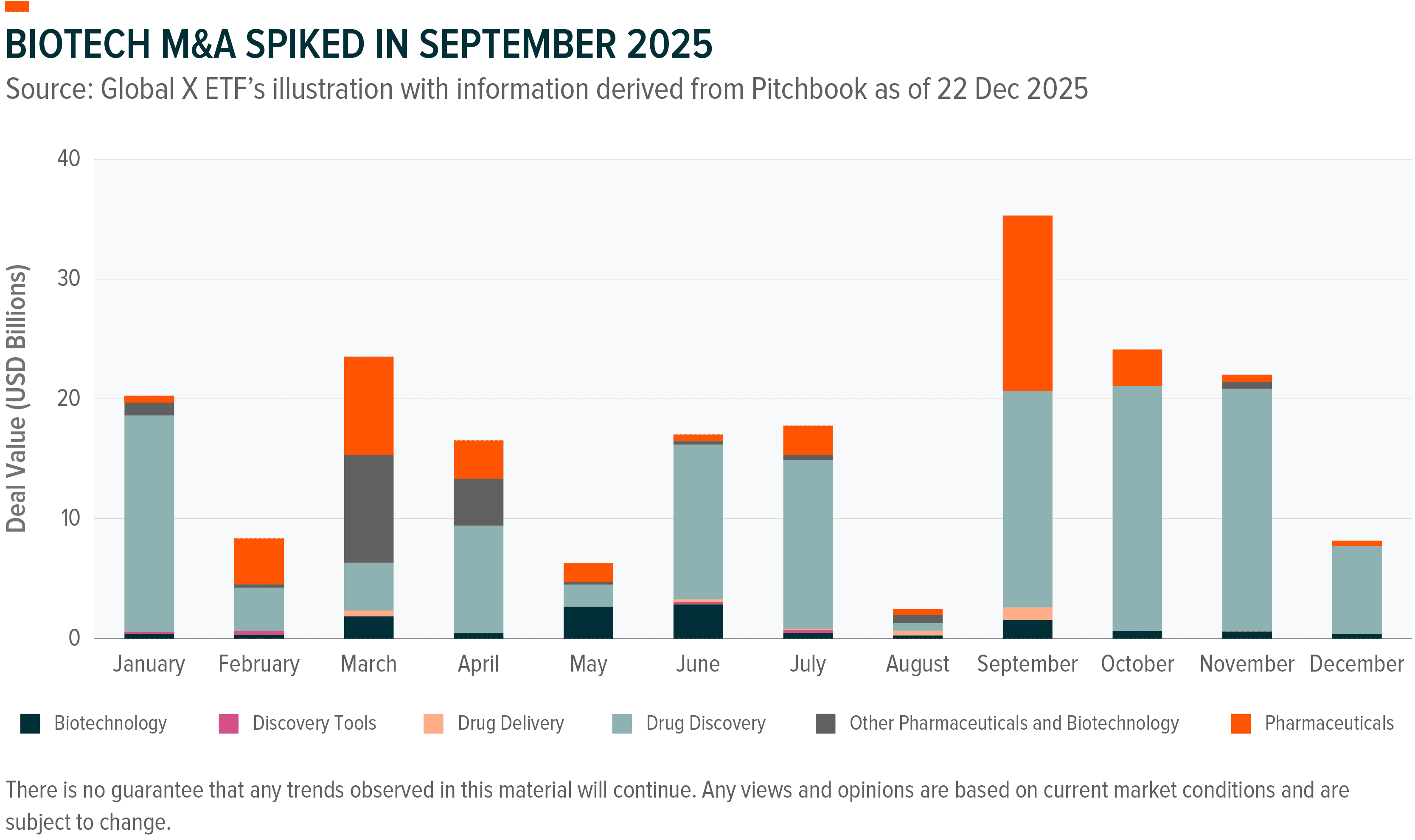

Between 2026 and 2030, an estimated $236 billion to $400 billion in annual branded prescription drug sales face loss of exclusivity as roughly 190 drugs, including 69 blockbusters with annual sales exceeding $1 billion each, come off patent.61 The exposure is concentrated at the top with Merck’s Keytruda ($23.3 billion in Q1-Q3 2025 alone), Bristol Myers Squibb’s Eliquis (projected sales declines of $1.5 to $2.5 billion in 2027), and Novartis’ Entresto (part of a $4 billion revenue gap expected in 2026 from multiple patent losses).⁶¹,⁶²,⁶³,⁶⁴,⁶⁵ This “super-cliff” is widely regarded as the largest cyclical patent expiration wave the industry has faced, potentially dwarfing the 2011-2016 cliff that saw drugs like Lipitor and Singulair lose exclusivity.⁶⁶ Faced with that pressure, pharmaceutical companies have responded not by accelerating internal R&D, which averages a decade, but by buying innovation.

Following a slow start due to U.S. tariff uncertainty, FDA leadership changes, and President Trump’s most favoured nation pricing executive order, biotech M&A picked up momentum in late 2025.⁶⁷ Of the top 10 biopharma M&A deals in 2025, 6 came in the fourth quarter.⁶⁸ 2025 total deal volume reached approximately $240 billion for the full year, representing an 82% surge, with multiple megadeals exceeding $5 billion compared to zero in 2024.⁶⁹,⁷⁰

The strategic shape of dealmaking has also changed. Rather than pursuing horizontal mega-mergers that attract FTC scrutiny, pharmaceutical companies are executing multiple smaller “bolt-on” acquisitions.⁷¹ These deals target late-stage clinical assets or recently approved drugs that can be integrated into existing commercial infrastructure without lengthy development timelines.⁷² Large pharmaceutical companies entered 2025 with substantial balance-sheet capacity, with the top 25 firms collectively holding approximately $1.3-1.4 trillion in deployable capital.⁷³ Industry experts anticipate this trend will continue through 2026 and 2027, with 20 or more acquisitions potentially exceeding $1 billion anticipated.⁷⁴

What has changed most is what companies are buying. The approximately $12 billion acquisition of Avidity Biosciences by Novartis clearly illustrates this strategic shift.⁷⁵ The deal wasn’t primarily about backfilling a single product gap, but about acquiring RNA delivery infrastructure capable of generating multiple therapies across different indications and disease areas.⁷⁶ That platform logic, buying the technology rather than just the drug, now defines most deals in the sector.⁷⁷

Three therapeutic areas dominated 2025 dealmaking, each for distinct reasons. Neuroscience staged a notable comeback with the two largest transactions of the year with Johnson & Johnson’s acquisition of Intra-Cellular and Novartis’ purchase of Avidity.⁷⁸ This represents an “absolute diversion from past trends when oncology dominated,” according to EY Americas life sciences leader Arda Ural.⁷⁹ Advances in RNA therapeutics, gene therapy, and biomarker-driven patient selection are reigniting confidence in central nervous system drug development.⁸⁰ Cardiometabolic assets emerged as a second battleground, fuelled by the GLP-1 revolution and the competitive urgency it has created, as illustrated by the Pfizer-Novo bidding war over Metsera.⁸¹,⁸² Rare diseaseretained its enduring appeal, with Sanofi’s Blueprint acquisition reflecting the continued attraction of genomically defined patient population and the favourable pricing dynamics they support.⁸³

Looking ahead, the conditions that drove last year’s activity remain intact.⁸⁴ The abundance of capital combined with the urgency created by the patent cliff creates a potentially favourable environment for innovative biotech companies with differentiated assets.

Analysts forecast 15% growth in both deal value and count for 2026.⁸⁵ Goldman Sachs anticipates record M&A across sectors, predicting roughly $3.9 trillion total global deal flow.86 Within biopharma, nearly 520 deals worth $230 billion are projected.⁸⁷ Supporting factors include: 1) the persistent patent cliff pressure, 2) reduced US market uncertainty following pharma-administration pricing agreements, 3) Fed rate cuts lowering capital costs, and 4) biotech valuations recovering from spring 2025 lows.⁸⁸

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. DrugPatentWatch. The Patent Cliff Playbook: A Strategic Guide to Tracking and Capitalizing on Pharmaceutical Loss of Exclusivity. 15 December 2025.

2. Schumacher A et al. Benchmarking R&D success rates of leading pharmaceutical companies: an empirical analysis of FDA approvals 2006 to 2022. 2 February 2025.

3. Novartis. Novartis agrees to acquire Avidity Biosciences, an innovator in RNA therapeutics, strengthening its late stage neuroscience pipeline. 26 October 2025.

4. Avidity. The Evolution of RNA Technology. Accessed 27 February 2026.

5. Bain & Company. M&A in Pharmaceuticals: Bigger, Bolder, and Far More Strategic. 2026 Annual Report. Accessed 27 February 2026.

6. Jamalinia & Weiskirchen. Personalized Cancer Therapy. Annals of Translational Medicine 13:2 April 2025 and Nature Reviews Clinical Oncology February 2026.

7. Xu et al. A generative AI discovered TNIK inhibitor for idiopathic pulmonary fibrosis: a randomized Phase 2a trial. Nature Medicine 31, 2602 to 2610 2025.

8. AlphaSense. Biotech and Pharma M&A: 2025 Outlook.

9. EY. Life Sciences M&A Firepower Report 2026. January 8 2026.

10. RD World Online. Life sciences M&A hit $240B in 2025 as Big Pharma preps for patent cliffs. 27 January 2026.

11. R., Antonio. MIT Technology Review. This baby boy was treated with the first personalised gene editing drug. 15 May 2025.

12. US Food and Drug Administration. Innovative Designs for Clinical Trials of Cellular and Gene Therapy Products in Small Populations. September 2025.

13. Illumina. Illumina’s evolutionary NovaSeq X exceeds 200th order milestone in first quarter 2023. 4 April 2023.

14. BioSpace. DNA Sequencing Market Size, Share, Growth and Forecast 2025 to 2034. 14 February 2025.

15. Illumina Inc. Illumina and MyOme Announce Million Person Health Trial. Press Release. December 2025. Accessed 27 February 2026.

16. MyOme. Economic Modeling: Preventive Genomics Could Save $200B+ Annually. White Paper. December 2025.

17. Qiagen N.V. QIAseq Comprehensive Genomic Profiling Panels. Product Portfolio 2025.

18. Bio Techne Corporation. Fiscal Year 2025 Financial Results. Earnings Release 2025.

19. Bio Techne Corporation. Lunaphore Acquisition: Automated Spatial Biology Platforms. Press Release Q3 2025.

20. Illumina. Introduction to NGS. Accessed 10 February 2026.

21. Ibid.

22. Illumina. The promise of circulating tumor DNA, a potential future alternative to invasive tissue biopsies.

23. Guardant Health. Shield Test FDA Breakthrough Designation. June 2025.

24. Natera. Signatera Transforming the management of cancer with personalised testing. Accessed 10 February 2026.

25. Ibid.

26. Ibid.

27. Khorkova et al. Amplifying gene expression with RNA targeted therapeutics. Nature Reviews Drug Discovery 22, 539 to 561. 30 May 2023.

28. Li et al. mRNA Vaccines: Current Applications and Future Directions. MedComm 6:11. 15 October 2025.

29. Moderna. Moderna 2025 Shareholder Letter. 5 January 2026.

30. Grand View Research. mRNA Therapeutics Market 2024 to 2030. Accessed 19 February 2026.

31. Alnylam Pharmaceuticals Website. Pioneering RNA interference Therapeutics. Accessed 27 February 2026.

32. Arrowhead Pharmaceuticals. Arrowhead Pharmaceuticals Announces FDA Approval of REDEMPLO plozasiran. November 18 2025.

33. Ibid.

34. Ibid.

35. Arrowhead Pharmaceuticals. Arrowhead Pharmaceuticals Announces NMPA Approval of REDEMPLO. January 7 2026.

36. Arrowhead Pharmaceuticals. Arrowhead Pharmaceuticals Receives FDA Breakthrough Therapy Designation for Plozasiran in Severe Hypertriglyceridemia. December 2 2025.

37. Drug Discovery News. Blockbuster drugs face a massive patent cliff in 2026. 24 February 2026.

38. Drug Target Review. In vivo CAR T: Faster, cheaper, and more effective cancer cure. 16 December 2024.

39. PR Newswire. REGENXBIO Highlights Key 2026 Catalysts. 11 January 2026.

40. Drug Discovery News. AI in Drug Discovery: From Hype to Clinical Validation. January 2025.

41. Pharmaceutical Technology. First Phase IIa Results for AI Designed Drugs Show Promising Efficacy. September 2025.

42. Drug Discovery News. AI in Drug Discovery: From Hype to Clinical Validation. January 2025.

43. ScienceNews. Have we entered a new age of AI enabled scientific discovery. 18 February 2026.

44. Ibid.

45. Ibid.

46. Ibid.

47. Moderna Inc. Machine Learning for mRNA Sequence Optimization. Technology White Paper 2025.

48. Illumina Inc. DRAGEN Platform: AI Accelerated Genomic Analysis. Technical Overview 2025.

49. Clinical Chemistry. AI Models Improve ctDNA Detection Sensitivity 3 to 5 times. Vol 71 2025.

50. Vertex Pharmaceuticals. Computational Chemistry and AI in Drug Discovery. R&D Overview 2025.

51. CAS Insights. Pharmaceutical Companies Build AI Supercomputers for Drug Discovery. December 2025.

52. Eli Lilly and Company. NVIDIA and Lilly Announce Co Innovation AI Lab to Reinvent Drug Discovery In the Age of AI. Press Release January 2026.

53. Goldman Sachs. Holdings AI Integration Analysis. Healthcare Equity Research January 2026.

54. Apheris. AI Structural Biology Network. Accessed 10 February 2026.

55. Ibid.

56. Pharmaphorum. Three more pharmas join OpenFold3 AI consortium. 10 February 2026.

57. Ibid.

58. Apheris. AI Structural Biology Network. Accessed 10 February 2026.

59. Lin F. Bioprocess 5.0: Straddles the Human AI Divide to Scale Next Gen Therapies. 15 September 2025.

60. Ibid.

61. DrugPatentWatch. The Patent Cliff Playbook: A Strategic Guide to Tracking and Capitalizing on Pharmaceutical Loss of Exclusivity. 15 December 2025.

62. Zacks. Will Keytruda Continue to Aid Merck’s Top Line in Q4 Earnings. 14 January 2026.

63. FiercePharma. With declining sales of legacy meds, BMS leans on new growth drivers to weather the storm. 5 February 2026.

64. Proclinical. Top 10 drugs with patents due to expire in the next five years. 16 February 2024.

65. DrugPatentWatch. The Patent Cliff Playbook: A Strategic Guide to Tracking and Capitalizing on Pharmaceutical Loss of Exclusivity. 15 December 2025.

66. Foley & Lardner LLP. Will the Next Patent Cliff Further Spur M&A Activity and What Does That Mean for Companies Right Now. 29 September 2025.

67. CNBC. Biotech M&A Hesitates Amid Tariff Uncertainty and Policy Changes. Q1 to Q2 2025.

68. EY. 2025 Biotech M&A: Six of Top Ten Deals Close in Q4. Annual M&A Report December 2025.

69. AlphaSense. Biotech M&A Surges 82% in 2025 to $240B Total Value. Industry Analysis December 2025.

70. S&P Global Market Intelligence. Multiple $5B+ Biotech Megadeals in 2025 vs. Zero in 2024. M&A Tracker 2025.

71. Harutyunyan A. Deal Forma. Large Cap Biopharma M&A 2024 to Q2 2025. 30 September 2025.

72. Ibid.

73. Bloomberg Intelligence. Top 25 Pharma Companies Hold $1.3 to $1.4 Trillion in M&A Firepower. January 2025.

74. EY Americas. 20+ Deals Exceeding $1B Expected in 2026 to 2027. M&A Forecast December 2025.

75. Novartis. Novartis agrees to acquire Avidity Biosciences, an innovator in RNA therapeutics, strengthening its late stage neuroscience pipeline. 26 October 2025.

76. MedCity News. Novartis Continues RNA and Neuroscience Growth Strategy With $12B Avidity Bio Acquisition. 28 October 2025.

77. Bain & Company. M&A in Pharmaceuticals: Bigger, Bolder, and Far More Strategic. 2026 Annual M&A Report.

78. PharmaVoice. Pharma’s Top Deals in 2025. December 2025.

79. EY. Quote from Arda Ural, EY Americas Life Sciences Sector Leader. Neuroscience M&A Represents Absolute Diversion. December 2025.

80. Nature Reviews Neurology. RNA Therapeutics and Biomarkers Reignite CNS Drug Development Confidence. Vol 21 2025.

81. BioPharma Dive. Cardiometabolic Assets Dominate 2025 M&A Activity. December 2025.

82. Pfizer Inc. Pfizer Wins Bidding War, Acquires Metsera for $10 Billion. Press Release November 2025.

83. BioPharma Dive. Cardiometabolic Assets Dominate 2025 M&A Activity. December 2025.

84. Morgan Stanley. Merck, J&J, Novartis, Sanofi, BMS Identified as Likely 2026 Acquirers. Equity Research January 2026.

85. ING. Come Together: Pharma M&A set to accelerate in 2026. 20 January 2026.

86. Evaluate Pharma. 2026 Biotech M&A Forecast: 15% Growth in Value and Deal Count. January 2026.

87. Pharma Intelligence. 520 Biopharma Deals Worth $230B+ Projected for 2026. M&A Database January 2026.

88. JPMorgan Healthcare Conference. Four Factors Supporting 2026 M&A Acceleration. Conference Proceedings January 2026.