Europe

Marketing Communication. Capital at risk. For Professional Investors Only. Please read fund legal documentation before making any final investment decisions.

From Roman aqueducts to the Channel Tunnel, Europe has never lacked ambition when it comes to developing infrastructure. However, it has historically faced challenges translating political and capital commitments into infrastructure development, compounded by regulatory friction that has slowed project delivery even when funding exists. Recently, these constraints have begun to ease, in ways that appear structural. EU institutions, national governments and political alignment in Hungary have converged to lock in a multi-decade infrastructure cycle that appears larger, more permanent, and more accommodative. The headline figures are clear: a proposed €81 billion Connecting Europe Facility in the next EU budget,¹ Germany's €500 billion Infrastructure Fund boosting federal and state investment,² and Ireland’s €275 billion ten-year National Development Plan.³ The tailwinds of these expanding fiscal commitments, combined with deregulation, the pricing power and margins of HALO assets, and opportunities such as Ukraine reconstruction, improve the operating environment for European infrastructure development materially.

Click here to view/download as PDF.

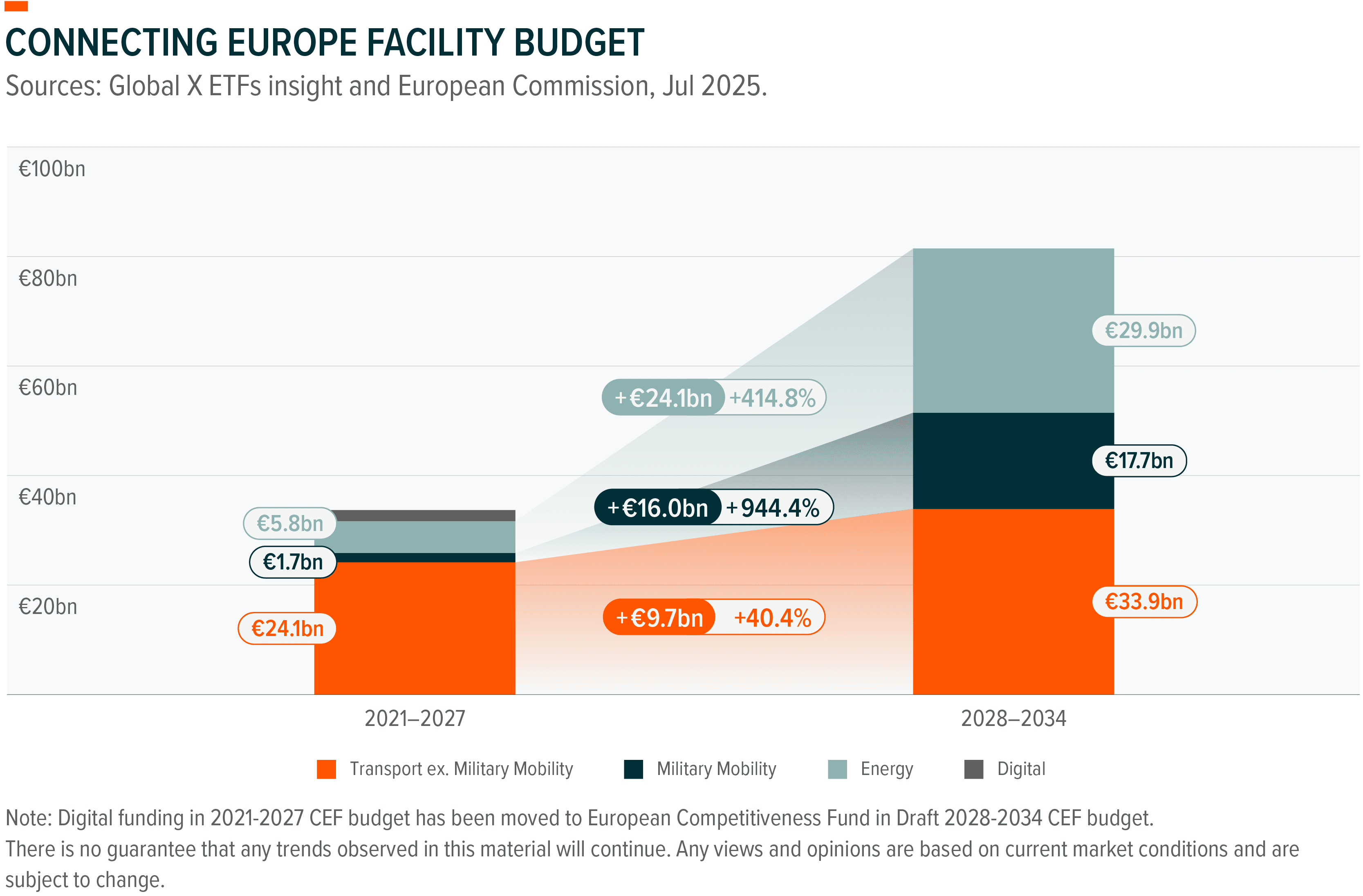

The Connecting Europe Facility (CEF) has long served as the EU's primary instrument for financing cross-border transport, energy, and digital infrastructure. In its proposed 2028-2034 Multi-Annual Financial Framework (MFF), the EU allocated €81.4 billion to CEF III, a significant increase from the €33.7 billion allocation to CEF II in the 2021-2027 MFF.¹³,¹⁴ The most notable increases are in Energy (+€24.1 billion; +414.8%) and Military Mobility (+€16.0 billion; +944.4%),¹⁵ areas which are growing in importance amidst the shifting geopolitical landscape. In December 2025, the Council of the EU adopted a partial mandate on CEF III as part of broader negotiations over the Multiannual Financial Framework for 2028 to 2034.¹⁶ The mandate establishes political consensus on continuing the facility.

Demand for capital is also increasing. In December 2025, the European Economic and Social Committee called for the EU to increase CEF funding to “at least 100 billion euros”.¹⁷ Similarly, in February 2026, a coalition of more than 40 European transport organisations, led by the International Road Transport Union (IRU), jointly called on the European Commission to allocate at least €100 billion to CEF III.¹⁸ The coalition's case is structural: available funding has consistently fallen short of need, leaving critical cross-border corridors and dual-use transport networks without adequate capital.¹⁹ Notably, the coalition draws an explicit connection between infrastructure investment and defence mobility readiness, framing underfunded road and rail networks as a security vulnerability.²⁰ This appears to broaden CEF III from a climate and connectivity instrument into a security infrastructure instrument, making meaningful allocation increases politically harder to resist.

The second shift is structural. The €577 billion Recovery and Resilience Facility (RRF) ends on 31 August 2026, with the deadline for the European Commission to make payments being 31 December 2026.²¹ It is being replaced by National and Regional Partnership Plans (NRPPs) within a single €771 billion fund covering cohesion, agriculture and security,²² as well as a €234 billion European Competitiveness Fund.²³ NRPPs make the funding channel permanent and disburse against milestones modelled on the RRF.²⁴ The trade-off is visibility: dedicated infrastructure lines are subsumed into single national plans competing with farm support and migration.²⁵ While the RRF funding deadline is close, some countries are seeking ways to access funds after the deadline. Italy and Spain are reportedly building special-purpose vehicles to capture post-deadline RRF spend off central budget.²⁶ Italy itself has secured €166 billion (85%) of its €194 billion funding allocation as of 29 April 2026, following receipt of its ninth instalment of €12.8 billion.²⁷

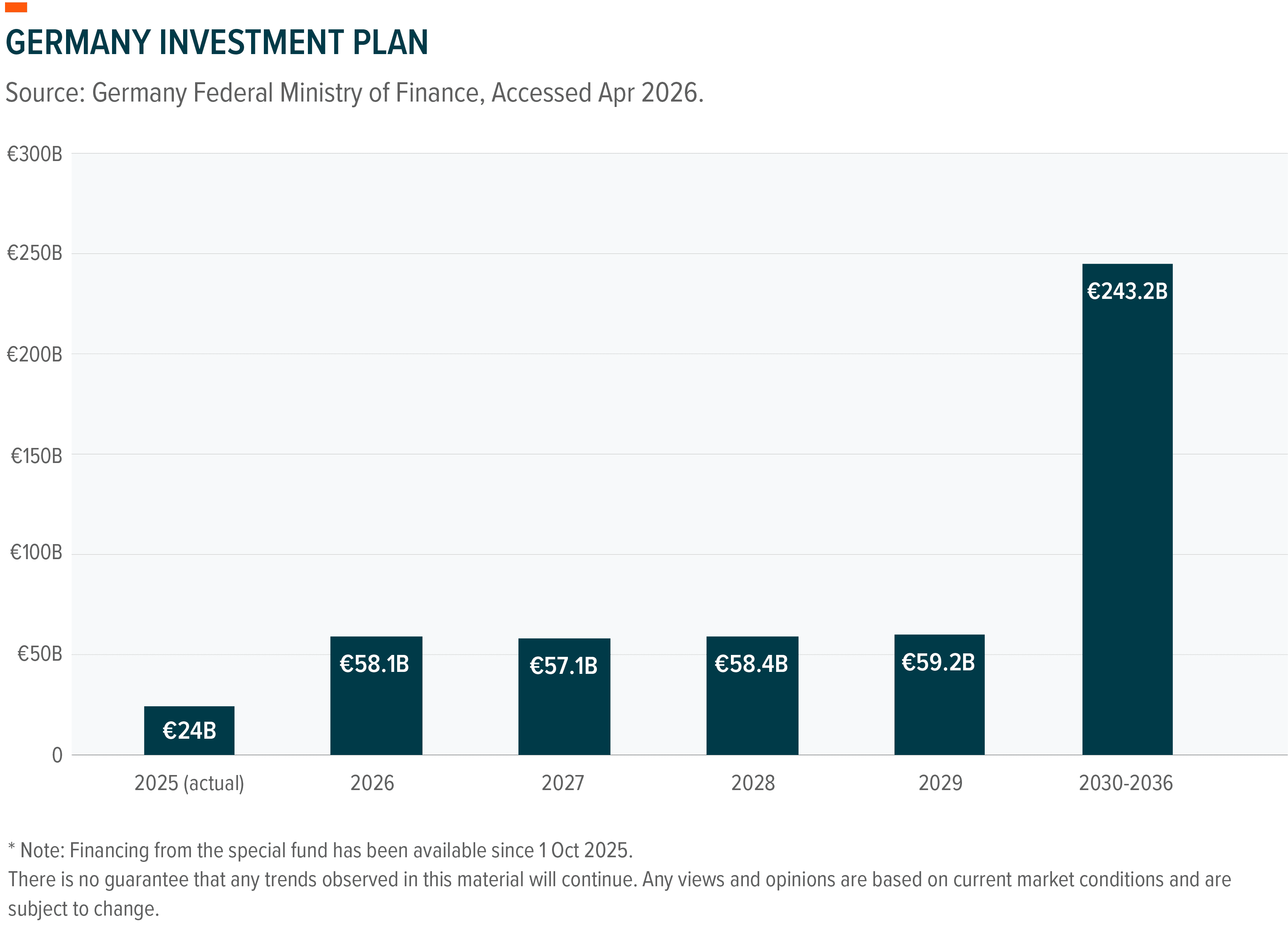

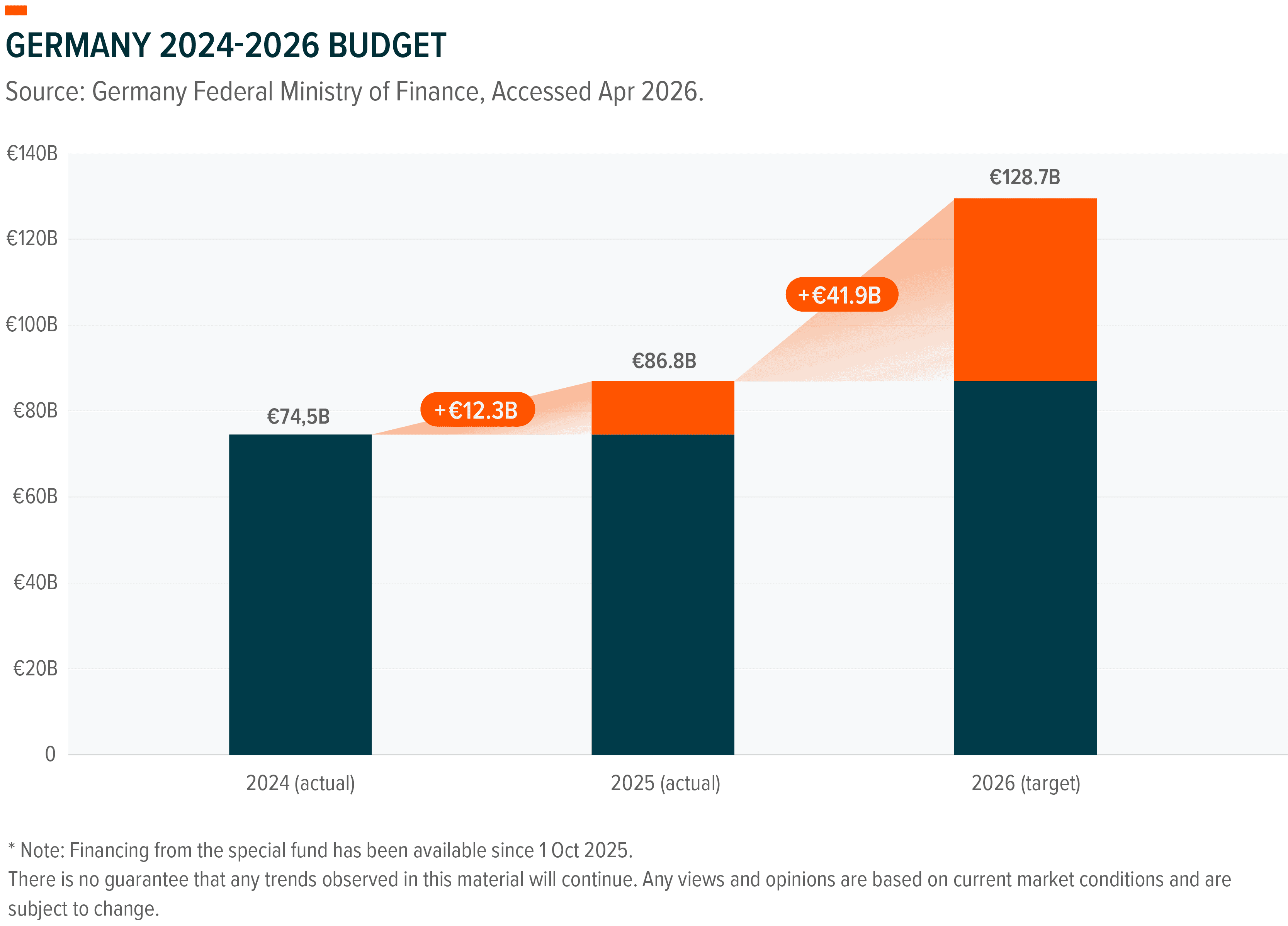

At the national level, Germany's Special Fund for Infrastructure and Climate Neutrality stands apart. Backed by a constitutional amendment, the vehicle provides €500 billion of additional investment capacity over 12 years.²⁸ The disbursements have already begun: €24 billion was deployed in the fourth quarter of 2025 alone, with federal investment spending rising approximately 17% year-on-year.²⁹ In 2026, the government plans to deploy approximately €58 billion from the special fund as part of total federal investment of around €129 billion, the largest peacetime investment programme in modern German history, with transport infrastructure, energy grids, and digitalisation as the primary destinations.³⁰

Capital alone, however, does not build infrastructure. Germany's Federal Modernisation Agenda, agreed between federal and Länder (i.e. state) governments in December 2025, addresses this directly.³¹ Across 200 concrete measures, the agenda targets the planning and administrative delays that have historically seen German infrastructure projects spend as long awaiting approvals as under construction.³² Pairing unprecedented capital with deregulatory intent could improve the risk/return calculus for contractors and concession operators with meaningful German exposure.

Ireland's €275 billion ten-year National Development Plan is among the most ambitious per-capita infrastructure programmes in the OECD.³³ The plan allocates €102.4 billion for 2026 to 2030, of which €22.3 billion is allocated to transport and up to €3.5 billion is allocated towards electricity grid infrastructure.³⁴ Complementing this is the Accelerating Infrastructure Report and Action Plan, published in December 2025, a 30-measure programme structured around legal reform, regulatory simplification, coordination reform, and public acceptance.³⁵ The plan introduces a Critical Infrastructure Bill, streamlines judicial review for strategic projects, and targets the planning delays that have historically converted strong capital commitments into slow project delivery.³⁶ This is the supply-side reform without which funding announcements tend to remain exactly that.

On 12 April 2026, Péter Magyar's Tisza party won Hungary's parliamentary election, securing a two-thirds supermajority and ending Viktor Orbán's 16-year rule. The investment implications are direct. Orbán's systematic resistance to EU rule-of-law conditionality had frozen approximately €17 billion in EU funds destined for Hungary, of which €9.6 billion sits within the RRF and REPowerEU.³⁷ Magyar's mandate to restore compliance creates a credible path to unlocking this capital,³⁸ potentially benefitting companies with existing relationships in Hungary and those with strong pan-European project experience.

The geopolitical dividend extends further. With Orbán's blocking position on Ukraine aid removed, the EU unblocked a €90 billion loan facility to Ukraine within days of the election result.³⁹ Why does this matter? Greater EU foreign and security policy cohesion accelerates defence-infrastructure spending and energy independence investment, both of which flow through the same concession and construction operators. The resulting compression of the geopolitical risk discount on European equities will likely be gradual, rather than immediate, but the direction is clear.

Infrastructure investment is only as effective as the permitting environment that enables it. The EU, alongside national governments, have acknowledged that regulatory burden and fragmentation have become a structural drag on competitiveness.⁴⁰ The legislative response since late 2025 has been broad and direct.

The "One Europe, One Market" Roadmap marks a shift in how Europe builds. The premise is that fragmentation, rather than capital, has slowed down infrastructure development, and the Roadmap treats the 27 permitting regimes, grid codes and procurement rulebooks as the binding constraint.⁴¹ The implication for infrastructure is significant: energy transmission, critical minerals, chips, and AI compute are no longer being pursued as twenty-seven national programmes loosely coordinated in Brussels but framed as single European assets, with a delivery horizon of end of 2027 and quarterly political review binding the three institutions to measurable progress.⁴² That changes the calculus for developers, as projects that previously stalled on jurisdictional friction gain a clearer route to approval, while those waiting for regulatory clarity now have firm dates to plan around.⁴³ At its core, the Roadmap is a proposition that Europe can compress a decade of institutional reform into eighteen months.

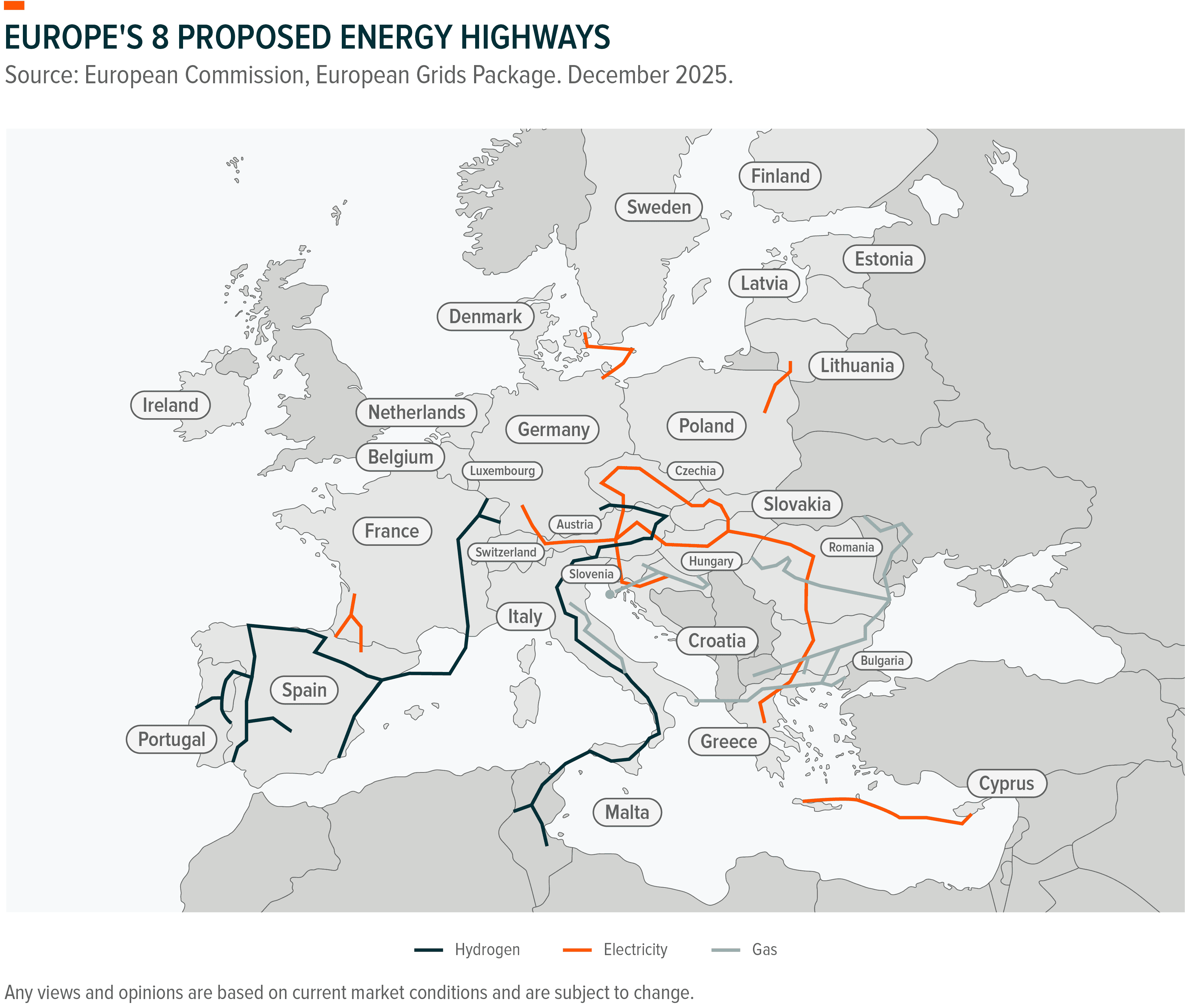

The first test of this proposition is energy. The European Grids Package, published by the Commission in late 2025, proposes a revision of the TEN-E Regulation alongside a dedicated instrument to accelerate permit-granting for cross-border energy infrastructure. Eight strategic energy highways are being fast-tracked,⁴⁴ backed by a proposed five-fold increase in Energy funding from CEF III.⁴⁵ The European Parliament's January 2026 briefing on the TEN-E revision, frames grid development explicitly as a prerequisite for both energy security and climate targets.⁴⁶ Beyond the direct project mandates this could create for grid-adjacent companies, the more important signal that the EU is prepared to use hard legislative instruments rather than exhortation to cut approval timelines.

The same logic applies to industrial capacity. The proposed Industrial Accelerator Act (IAA) aims to lift manufacturing from 14.3% to 20% of EU GDP.⁴⁷ While the focus is on accelerating permitting, three strategic sectors that represent only 15% of EU manufacturing, these sectors serve central roles as upstream suppliers and enablers of downstream industrial ecosystems across a broad range of end industries; construction, mobility, energy, space and defence.⁴⁸ Furthermore, the IAA also introduces “Made in EU” rules around public procurement of markets for European steel, cement, aluminium, EVs and clean technologies, which appear supportive of EU production across these industries.⁴⁹ Importantly, the Act signals that the EU is recalibrating away from a compliance-maximising regulatory posture towards one that prioritises industrial capacity and output.⁵⁰ For European engineering and construction majors, reindustrialisation could create demand for factory infrastructure, energy connections, and logistics networks.

Finally, the discussion of “Made in EU” rules in the IAA also ties into the broader discussion of European competitiveness. Here, the EU’s goal of creating European champions could see a broadening of the terms that the EU considers when assessing mergers, with the goal of consolidation to enable European companies to accelerate innovation and achieve the scale required to compete on the global stage.⁵¹ The “One Europe, One Market” roadmap targets the end of 2026 for the review of merger control guidelines.⁵² Industry consolidation could serve as a catalyst for European companies in critical industries.

At a national level, Germany's Federal Modernisation Agenda and Ireland's Accelerating Infrastructure plan, introduced in the funding section above, reinforce the same logic. These are not aspirational policy documents, but contain named measures, responsible bodies, and implementation timelines. The accompanying Infrastructure Future Act, approved in December 2025, extends "overriding public interest" to motorways, rail, dams and transmission lines, exempts replacement construction from formal planning approval.⁵³ Dublin's Accelerating Infrastructure plan aims to address the judicial-review bottlenecks that stalled MetroLink and Greater Dublin Drainage, with statutory caps on legal costs and a critical-infrastructure bill aiming to compress consenting timelines by up to twelve months.⁵⁴ Together these deregulatory moves convert fiscal commitments into infrastructure development.

Not all infrastructure assets carry the same investment characteristics. At the quality apex sit HALO (‘Heavy Asset, Low Obsolescence’) assets: high-barrier, long-life, operationally essential infrastructure with monopoly-like structures. Airports, cross-border tunnels, and toll roads are some examples. The nature of their quality may be due to a combination of duration, and the difficulty of replacing these assets, creating a structural capacity to raise prices at or above inflation, a valuable characteristic when input costs remain elevated.

Airports combine regulated aeronautical charges that provide returns on invested capital, with substantial non-aeronautical revenues from retail, property, and ancillary services.⁵⁵ Commercial (non-aeronautical) revenues offer flexible, higher-margin growth levers through retail mix, pricing, and property development.⁵⁶ As dwell times extend and passenger volumes recover, airports are increasing retail revenue per passenger through targeted investment in commercial space, tenant mix, and passenger segmentation, not solely through higher traffic.⁵⁷ This form of value creation does not require new concession wins or additional capital deployment.⁵⁸ It compounds quietly within an existing asset base.

Tunnels represent the most extreme form of infrastructure monopoly: there is no competing asset. Getlink, operator of the Channel Tunnel, illustrates how operators in this category can generate returns from financial as much as operational management. Through disciplined refinancing of long-dated debt, the company has reduced its average cost of capital and extended maturity profiles in ways that directly enhance equity returns, independent of revenue growth.⁵⁹ In an interest rate environment that has shifted materially since 2022, the ability to liability-manage intelligently separates good operators from excellent ones.

Toll roads and bridges close the picture. Concession operators of companies such as Vinci, Ferrovial, and Eiffage typically operate under contractual frameworks that typically embed CPI linkage or minimum revenue guarantees, providing explicit inflation protection within the underlying contract structure.⁶⁰ Traffic growth layered on top of inflation-linked base tariffs is a compounding dynamic that the market often underweights when assigning through-cycle multiples to these businesses. With a strong pipeline of public-private partnership projects in Europe,⁶¹ the pipeline for long-duration asset creation is deepening precisely when existing assets are repricing upward.

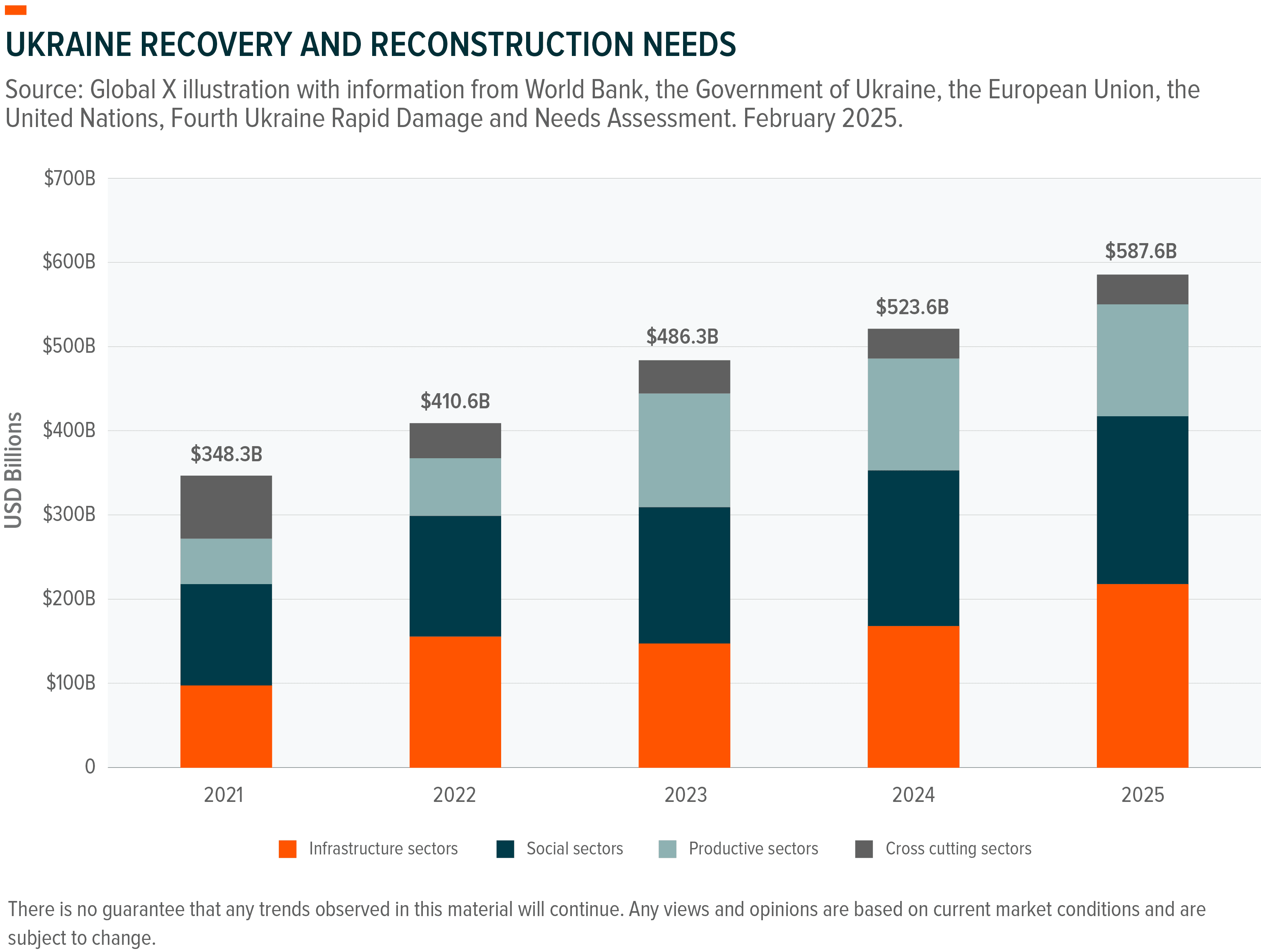

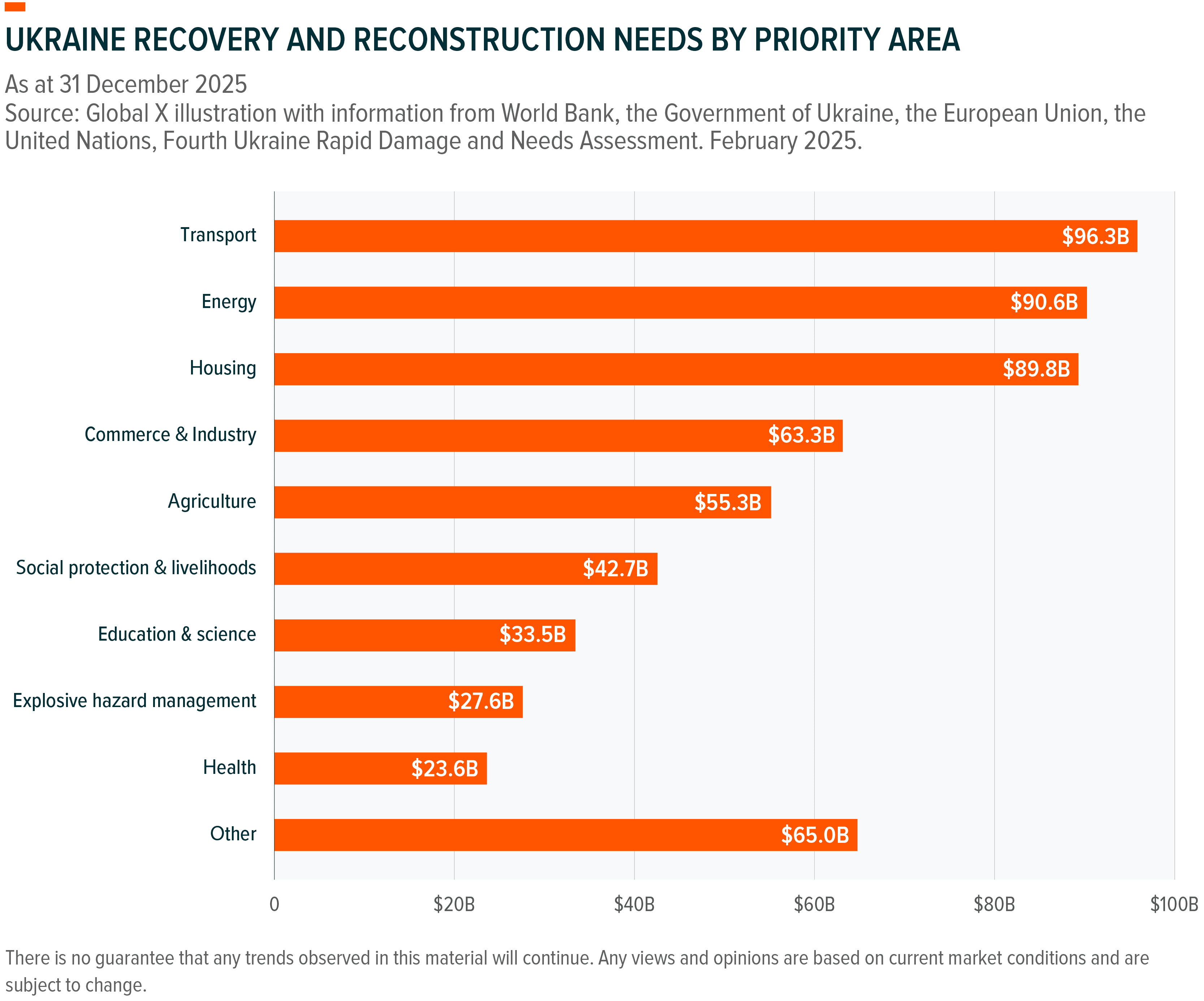

Beyond Europe's internal investment cycle, the prospect of Ukrainian reconstruction represents a demand catalyst of a different order. As of December 2025, the total cost of Ukraine's reconstruction and recovery was estimated at nearly $588 billion over the next decade, almost three times Ukraine's 2025 GDP.⁶² The estimate rose 12% from the prior year, driven partly by a 21% increase in damage to energy infrastructure.⁶³ Transport needs alone exceed $96 billion, while energy exceeds $91 billion.⁶⁴

The financing architecture is already in place. The EU's Ukraine Facility commits €50 billion between 2024 and 2027 in grants and loans, structured around macro-financial support and reform-linked disbursements tied to EU accession progress.⁶⁵ The Ukraine Investment Framework, the facility's investment arm, has been reinforced to €9.5 billion in guarantees, targeting an overall €40 billion in mobilised investment across energy, digital, transport, and manufacturing.⁶⁶ The €90 billion EU loan, unblocked following the Hungarian election result, adds a further layer of state liquidity that enables Ukrainian procurement to proceed at scale.⁶⁷

This will likely have a direct and structural impact on European infrastructure development companies. European construction and engineering majors are the natural counterparties for large-scale civil infrastructure contracts. As the security environment stabilises and procurement pipelines mature, the companies best positioned to win this work are those with existing pan-European operations, proven multi-jurisdictional delivery track records, and the balance sheet capacity to pre-finance mobilisation costs. Ukraine's EU accession path also matters. The progressive adoption of EU procurement standards, environmental assessments, and project financing norms means the reconstruction programme is being structured, from the outset, in a way that is accessible to European listed infrastructure firms rather than exclusively to bilateral state contractors.⁶⁸,⁶⁹

The investment case is not predicated on a near-term peace settlement. The Ukraine Facility and Ukraine Investment Framework are already disbursing funds and mobilising investments, with recovery and reconstruction projects, particularly in energy, transport and housing, being financed and implemented on an ongoing basis, including during the ongoing war.⁷⁰,⁷¹ The reconstruction opportunity adds an optionality layer that the market has not yet systematically priced.

The roadmap shaped by these four drivers points to an infrastructure investment cycle in Europe that has matured from cyclical recovery to structural compounding. A deepening and more permanent funding base, a regulatory environment undergoing genuine structural reform, and HALO assets appear positioned to compound returns through inflation linkage and operational leverage do not often arrive simultaneously. The traditional objection to European infrastructure, that capital is announced but rarely deployed, is being addressed with legislative instruments and administrative reforms designed to close the gap between ambition and execution.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. European Parliament, Connecting Europe Facility 2028-2034: Financing EU infrastructure networks. December 2025.

2. Germany Federal Ministry of Finance, The Special Fund for Infrastructure and Climate Neutrality. Accessed 30 April 2026.

3. Government of Ireland, National Development Plan Review 2025. 18 November 2025.

4. European Parliament, Connecting Europe Facility 2028-2034: Financing EU infrastructure networks. December 2025.

5. European Parliament, National and regional partnership plans, European territorial cooperation and EU facility 2028-2034. January 2026.

6. Politico, Orbán’s rival faces uphill battle to unfreeze €17B in EU funds. 9 April 2026.

7. Noerr, Federal modernisation agenda: federal and state governments agree on measures to modernise the state. 7 January 2026.

8. Ireland Department of Public Expenditure, Infrastructure, Public Service Reform and Digitisation, Government publishes Accelerating Infrastructure - Report and Action Plan. 24 January 2026.

9. European Commission, One Europe, One Market Roadmap of the European Parliament, the Council of the European Union and the European Commission. 24 April 2026.

10. European Commission, Commission proposes upgrade of the EU's energy infrastructure to lower bills and boost independence. 10 December 2025.

11. European Parliament, Industrial Accelerator Act: In “A new plan for Europe's sustainable prosperity and competitiveness”. 20 March 2026.

12. ClearBridge, Inflation and Higher Rates: What They Mean for Infrastructure. April 2026.

13. European Commission, A dynamic EU Budget for the priorities of the future - The Multiannual Financial Framework 2028-2034. 16 July 2025.

14. European Commission, Connecting Europe Facility 2021-2027 adopted. 20 July 2021.

15. European Commission, A dynamic EU Budget for the priorities of the future - The Multiannual Financial Framework 2028-2034. 16 July 2025.

16. European Council, MFF: Council adopts partial mandate on the Connecting Europe Facility (CEF III). 15 December 2025.

17. European Economic and Social Committee, Connecting Europe Facility - 2028-2034. 12 December 2025.

18. IRU, Open letter: A competitive and resilient Europe requires a stronger EU transport budget. 23 February 2026.

19. Ibid.

20. Ibid.

21. European Commission, Questions and answers on the implementation of NextGenerationEU – The road to 2026. 4 June 2025.

22. European Parliament, National and regional partnership plans, European territorial cooperation and EU facility 2028-2034. January 2026.

23. European Commission, European Competitiveness Fund. Accessed 30 April 2026.

24. European Parliament, National and regional partnership plans, European territorial cooperation and EU facility 2028-2034. January 2026.

25. Ibid.

26. Oxford Economics, EU recovery spending should continue after 2026. 29 Oct 2025.

27. European Commission, Commission greenlights Italy's ninth payment request for €12.8 billion under NextGenerationEU. 29 April 2026.

28. Germany Federal Ministry of Finance, The Special Fund for Infrastructure and Climate Neutrality. Accessed 30 April 2026.

29. Ibid.

30. Ibid.

31. Noerr, Federal modernisation agenda: federal and state governments agree on measures to modernise the state. 7 January 2026.

32. Ibid.

33. Ireland Government: Department of the Taoiseach, Government publishes updated National Development Plan. 22 July 2025.

34. Government of Ireland, National Development Plan Review 2025. 18 November 2025.

35. Government of Ireland, Department of Public Expenditure, Government Publishes Accelerating Infrastructure Report and Action Plan. Dec 2025.

36. Ibid.

37. Politico, Orbán’s rival faces uphill battle to unfreeze €17B in EU funds. 9 April 2026.

38. Financial Times, EU in talks with Hungary’s Péter Magyar on workaround for frozen funds. 29 April 2026.

39. Bloomberg, Ukraine to get €90 Billion EU Loan After Hungary Drops Veto. April 2026.

40. Enrico Letta, More Than A Market. April 2024.

41. European Commission, One Europe, One Market Roadmap of the European Parliament, the Council of the European Union and the European Commission. 24 April 2026.

42. Ibid.

43. Ibid.

44. European Commission, Commission proposes upgrade of the EU's energy infrastructure to lower bills and boost independence. 10 December 2025.

45. European Parliament, Connecting Europe Facility 2028-2034: Financing EU infrastructure networks. December 2025.

46. European Parliament, Guidelines for trans-European energy infrastructure: Revision of the TEN-E Regulation. 23 January 2026.

47. European Commission, Proposal for a regulation of the European parliament and of the council establishing a framework of measures for the acceleration of industrial capacity and decarbonisation in strategic sectors and amending regulations (EU) 2018/1724, (EU) 2024/1735 and (EU) 2024/3110. 4 March 2026.

48. Ibid.

49. Ibid.

50. Ibid.

51. Financial Times, EU to relax merger rules in bid to create ‘European champions’. 16 April 2026.

52. European Commission, One Europe, One Market Roadmap of the European Parliament, the Council of the European Union and the European Commission. 24 April 2026.

53. Freshfields, Infrastructure Future Act in Germany.26 January 2026.

54. Government of Ireland, Accelerating Infrastructure Report and Action Plan.16 April 2026.

55. Airports Council International, State of the Airport Non-Aeronautical Business: From Traffic Recovery to Value Reinvention. 17 March 2026.

56. Airports Council International, Maximizing Non-Aeronautical Revenues: Key to Airport Financial Sustainability. 8 May 2025.

57. Airports Council International, State of the Airport Non-Aeronautical Business: From Traffic Recovery to Value Reinvention. 17 March 2026.

58. Roland Berger, Commercial effectiveness at modern airports: Lessons from European airports. November 2024.

59. Getlink, Annual and Quarterly Reports. Accessed April 2026.

60. ClearBridge, Inflation and Higher Rates: What They Mean for Infrastructure. April 2026.

61. European Investment Bank, Market Update: Review of the European Public-Private Partnership Market in 2024. March 2025.

62. World Bank Group, European Commission, United Nations and Government of Ukraine, Updated Ukraine Recovery and Reconstruction Needs Assessment (RDNA5), February 2026.

63. Ibid.

64. Ibid.

65. European Commission, Ukraine Facility. December 2025.

66. European Commission, EU Steps Up Support for Ukraine’s Recovery, Reconstruction, and Modernisation. November 2025.

67. Bloomberg, Ukraine to get €90 Billion EU Loan After Hungary Drops Veto. April 2026.

68. Lead with Europe, Procurement under the Ukraine Facility: new rules and requirements for procuring entities. 5 November 2025.

69. European Business Association, Ukraine overhauls its PPP regime, facilitating reconstruction and investment. 19 June 2025.

70. European Commission, Ukraine Facility. Accessed 30 April 2026.

71. European Commission, Ukraine Investment Framework. Accessed 30 April 2026.