Europe

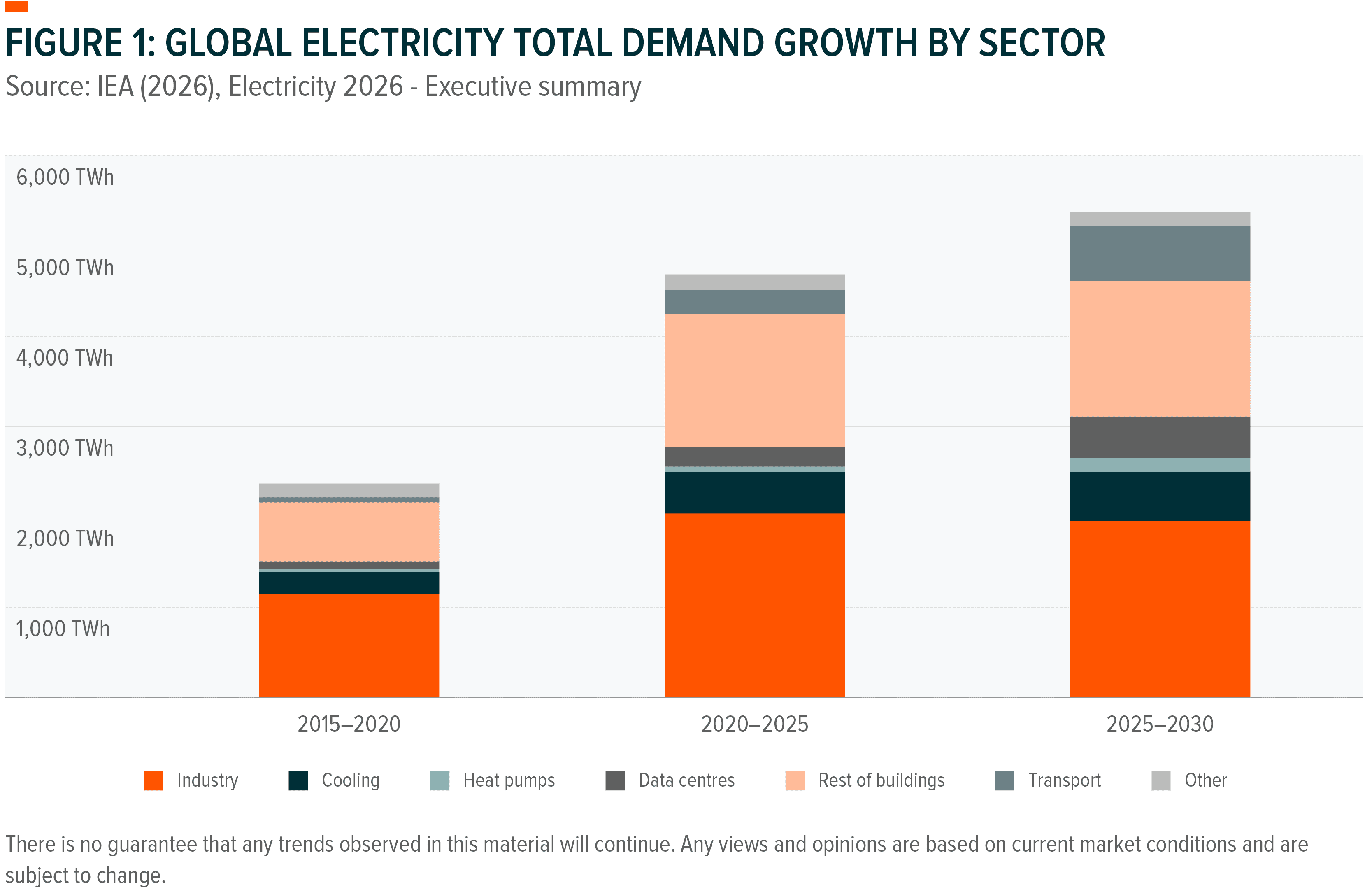

Electricity demand is entering a structurally higher growth phase, driven by AI data centres, and the electrification of industry, construction and transport.¹ Unlike past cycles, much of this incremental demand , high-utilisation, and intolerant of interruption, increasing the premium on reliable baseload power.²

Renewables remain central to electrification, but their intermittency creates a growing need for firm, always-on generation as penetration rises.³ Nuclear power is one of the few scalable sources of low-carbon, dispatchable electricity, positioning it as a critical stabiliser within increasingly complex power systems.⁴

Uranium’s relatively small, contract-driven structure typically amplifies price responses as utilities secure supply earlier and for longer, forming favourable conditions for miners through improved pricing leverage.⁵ The opportunity spans the nuclear value chain, however, from fuel-cycle services, reactor operators, to new technologies that stand to benefit from policy initiatives aimed at reversing decades of underinvestment in nuclear infrastructure.⁶

Diversified exposure across the nuclear value chain captures the structural role of nuclear power in a higher-load grid, rather than relying on a single technology or commodity price outcome.

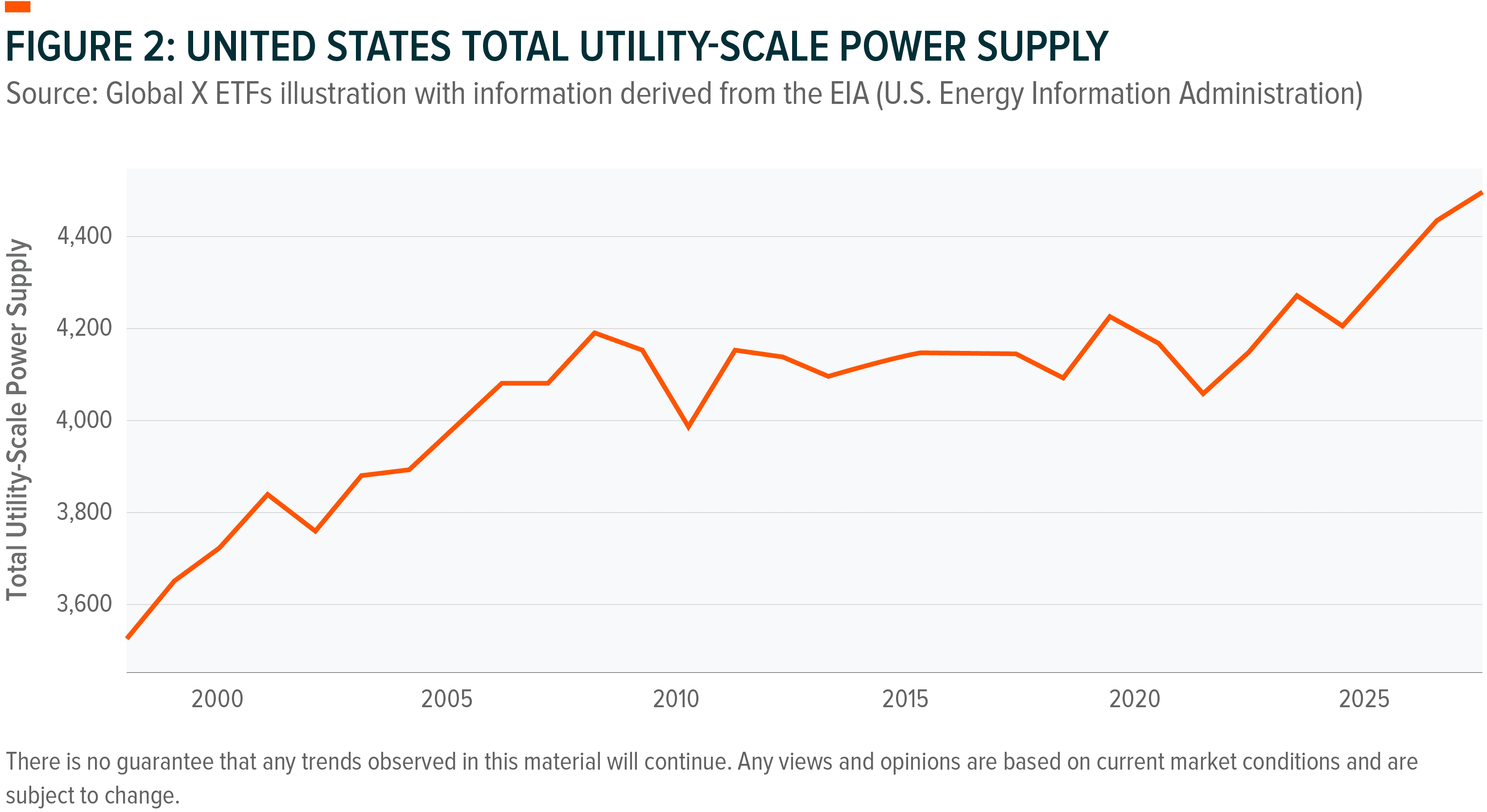

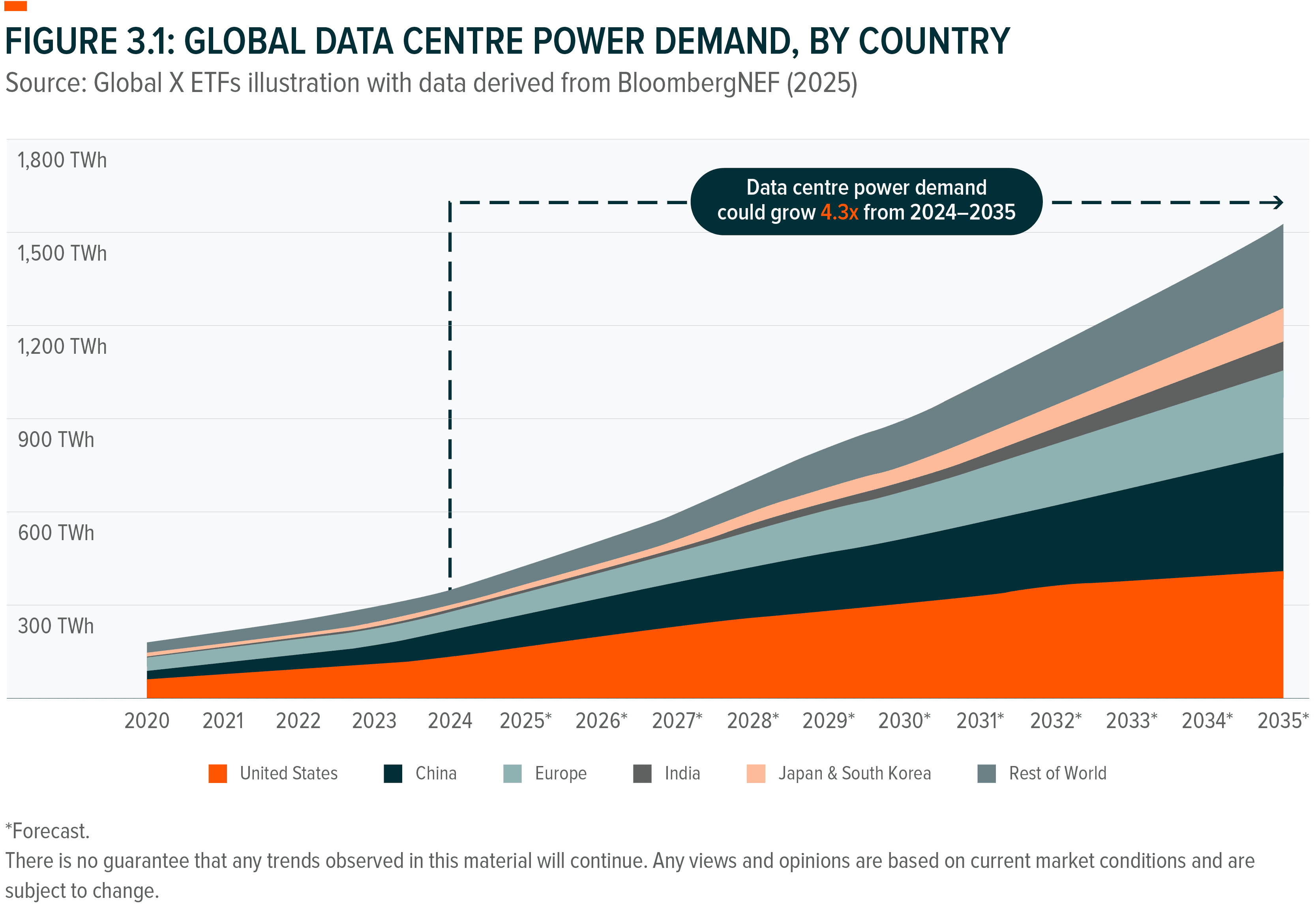

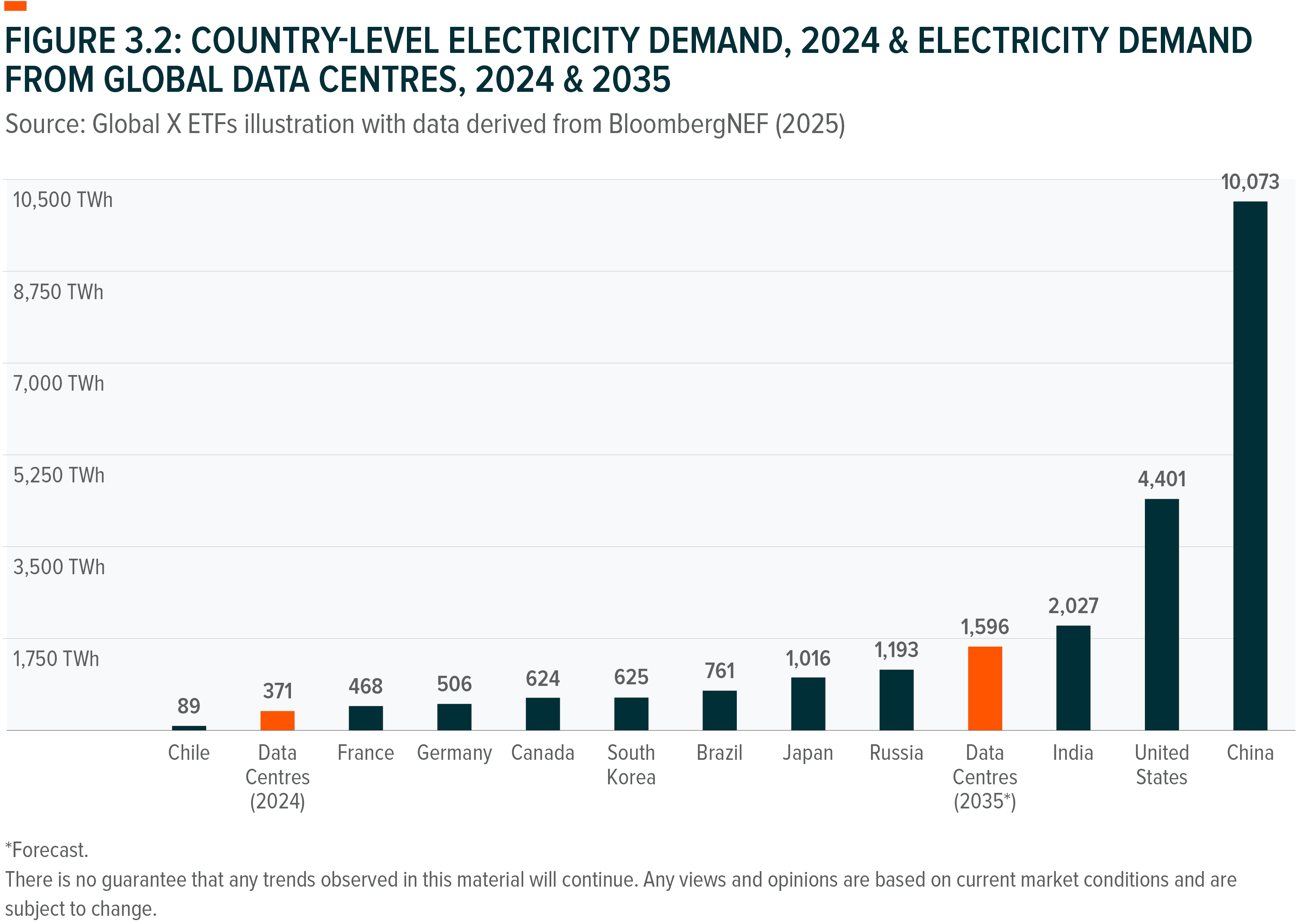

Global electricity demand is re-accelerating following more than a decade of flat growth between 2008 and 2021.⁷ The type of demand now driving growth is fundamentally different from past cycles, with data centres adding a large, always-on source of incremental load, growing at ~15% per year through 2030.⁸

Against this backdrop, nuclear’s role is being re-framed from legacy generation to a strategic source of clean, firm capacity, supporting reliability as power systems absorb higher, always-on demand.¹²

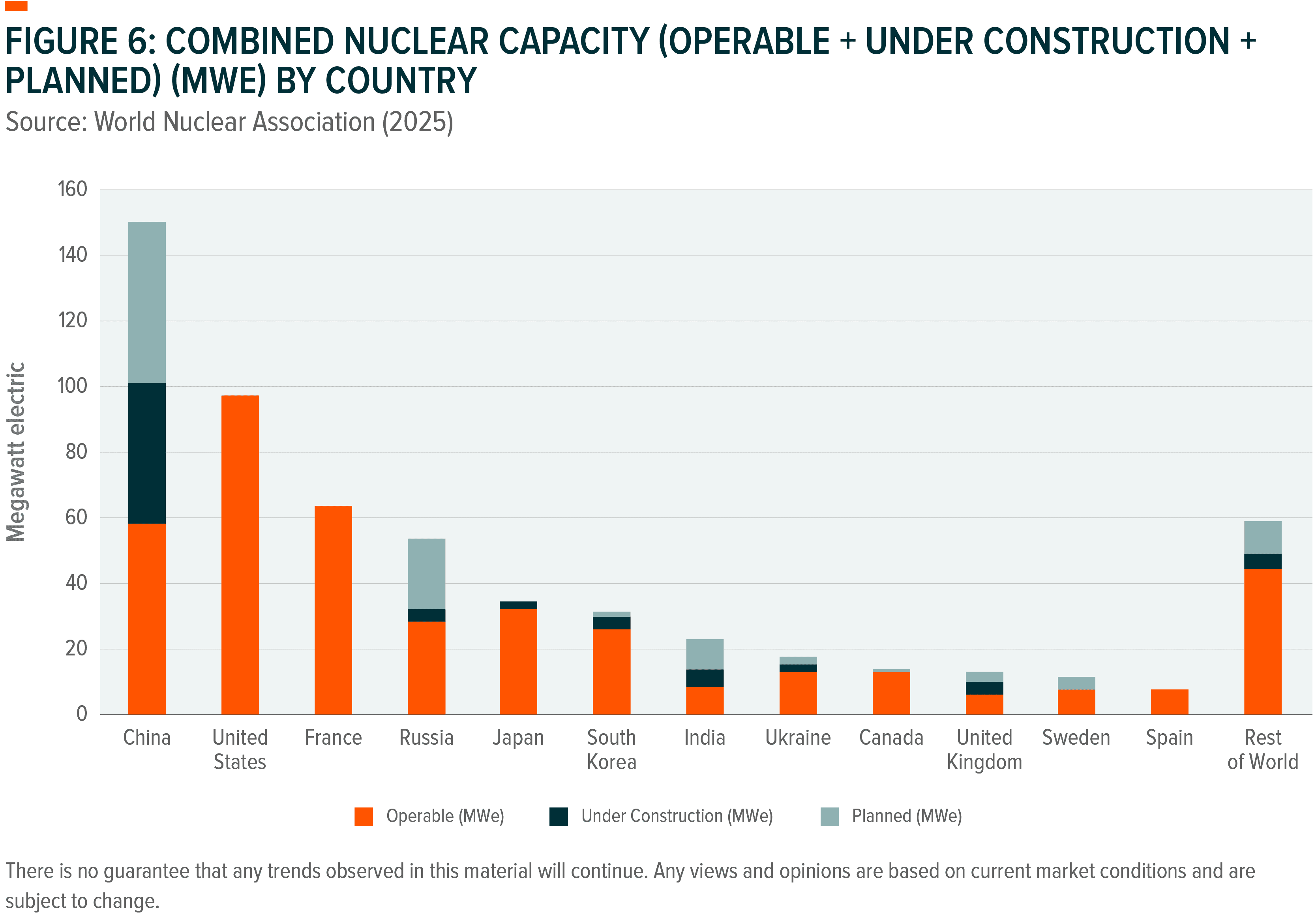

While new nuclear construction attracts headlines, the existing reactor fleet is the dominant driver of near- and medium-term uranium demand.¹³

These decisions can convert uncertain future demand into committed, multi-decade fuel requirements.

Once a reactor is life-extended, uranium demand becomes contractual rather than discretionary; insensitive to short-term power prices; anchored over decades, not cycles.¹⁸ This creates a durable base of uranium consumption even if new-build timelines slip.¹⁹

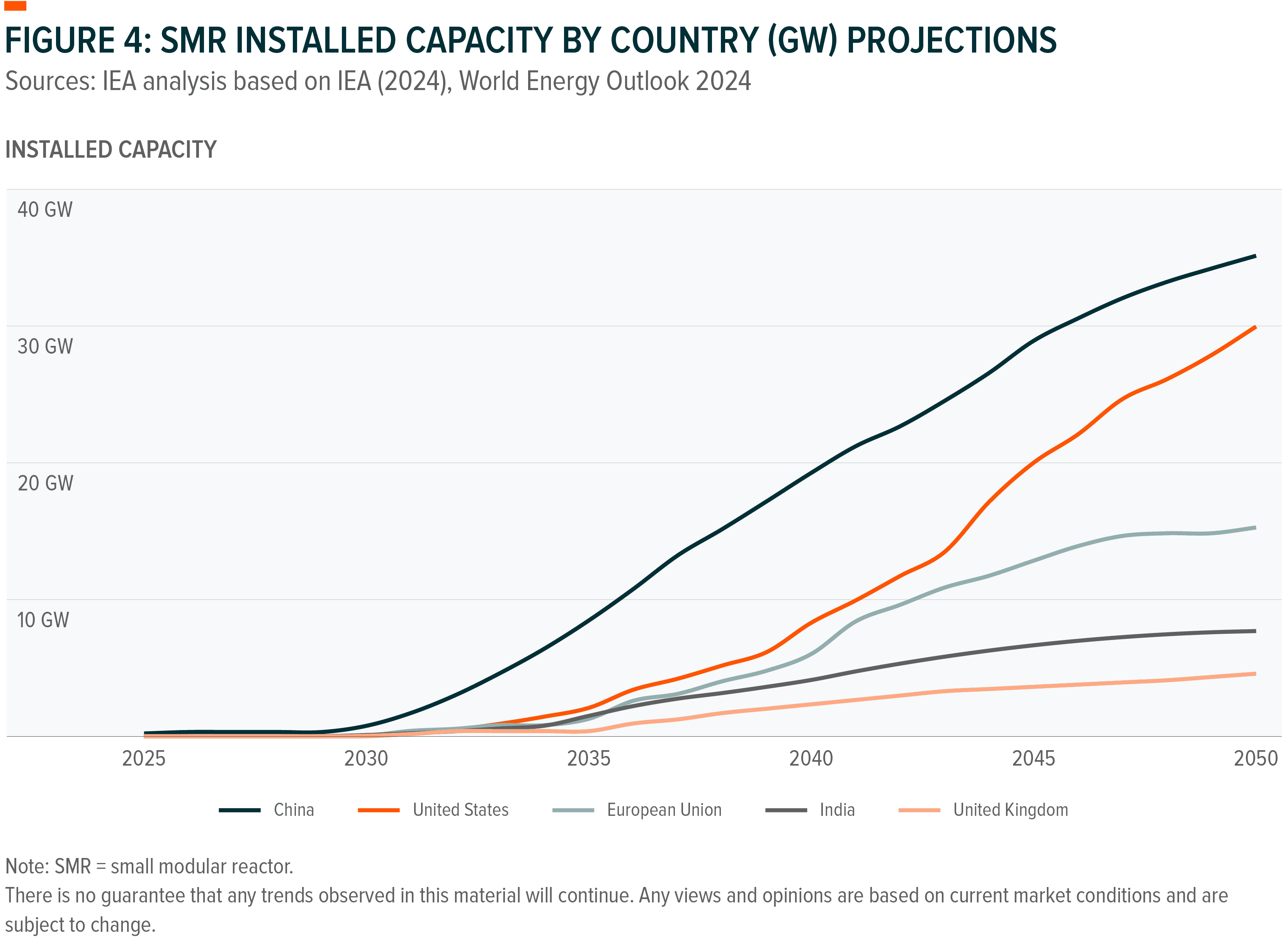

SMRs aim to shift nuclear from a small number of large, bespoke projects toward a more scalable model: smaller pre-fabricated units, more output flexibility, and faster replication over time.²⁰ The addressable market expands into:

Data centres illustrate the problem SMRs are designed to solve: large, power-hungry facilities that require continuous, reliable power.²² This has driven interest and agreements between the SMR developers and hyperscalers.²³

SMRs introduce long-term optionality that extends the nuclear growth runway beyond existing technologies.²⁴ They also deepen the investment case for the fuel cycle, as many advanced designs increase requirements for higher-assay fuels (e.g., HALEU), creating new bottlenecks across enrichment, fabrication, and transport that Western public policy is aggressively seeking to solve through investment.²⁵

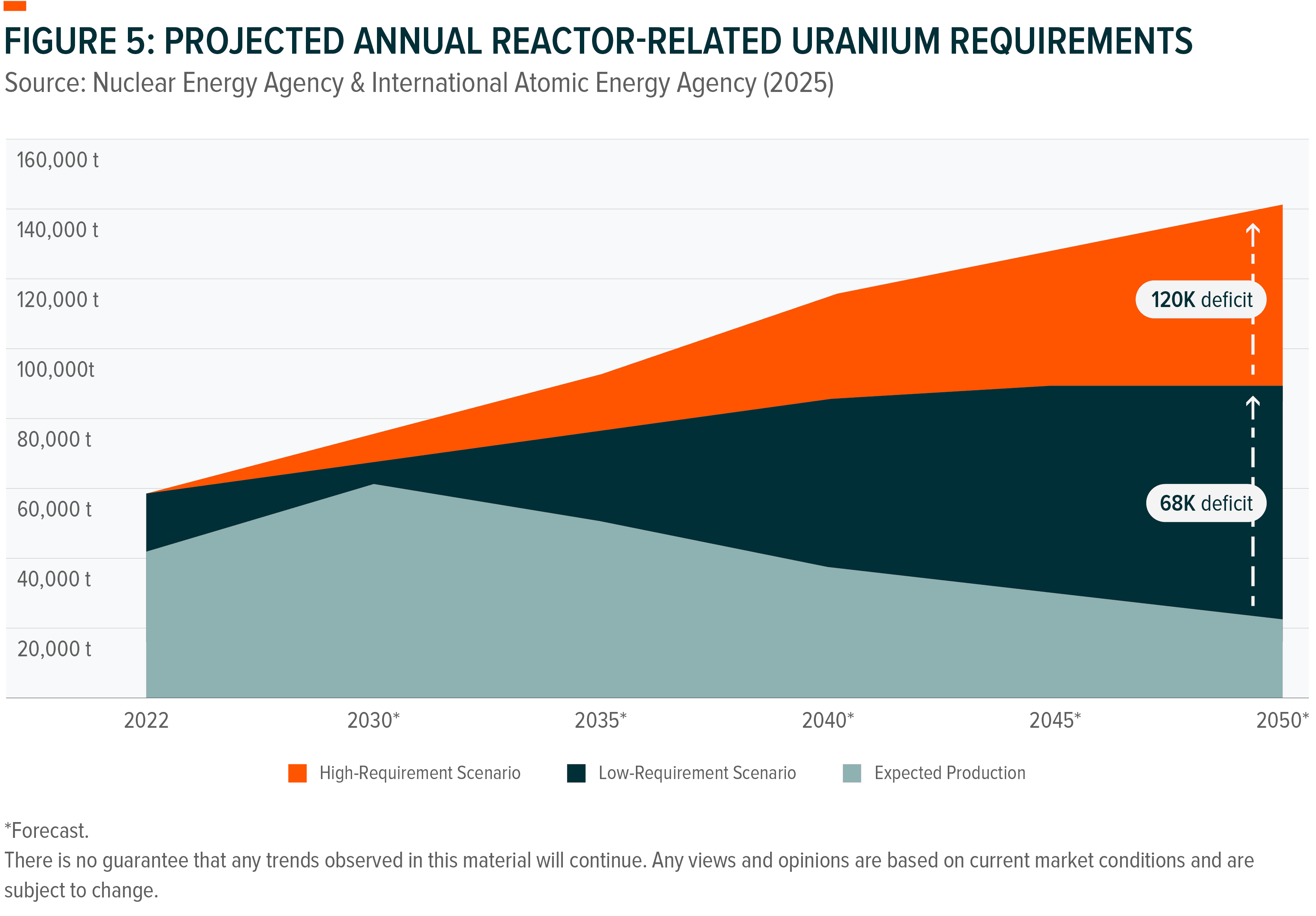

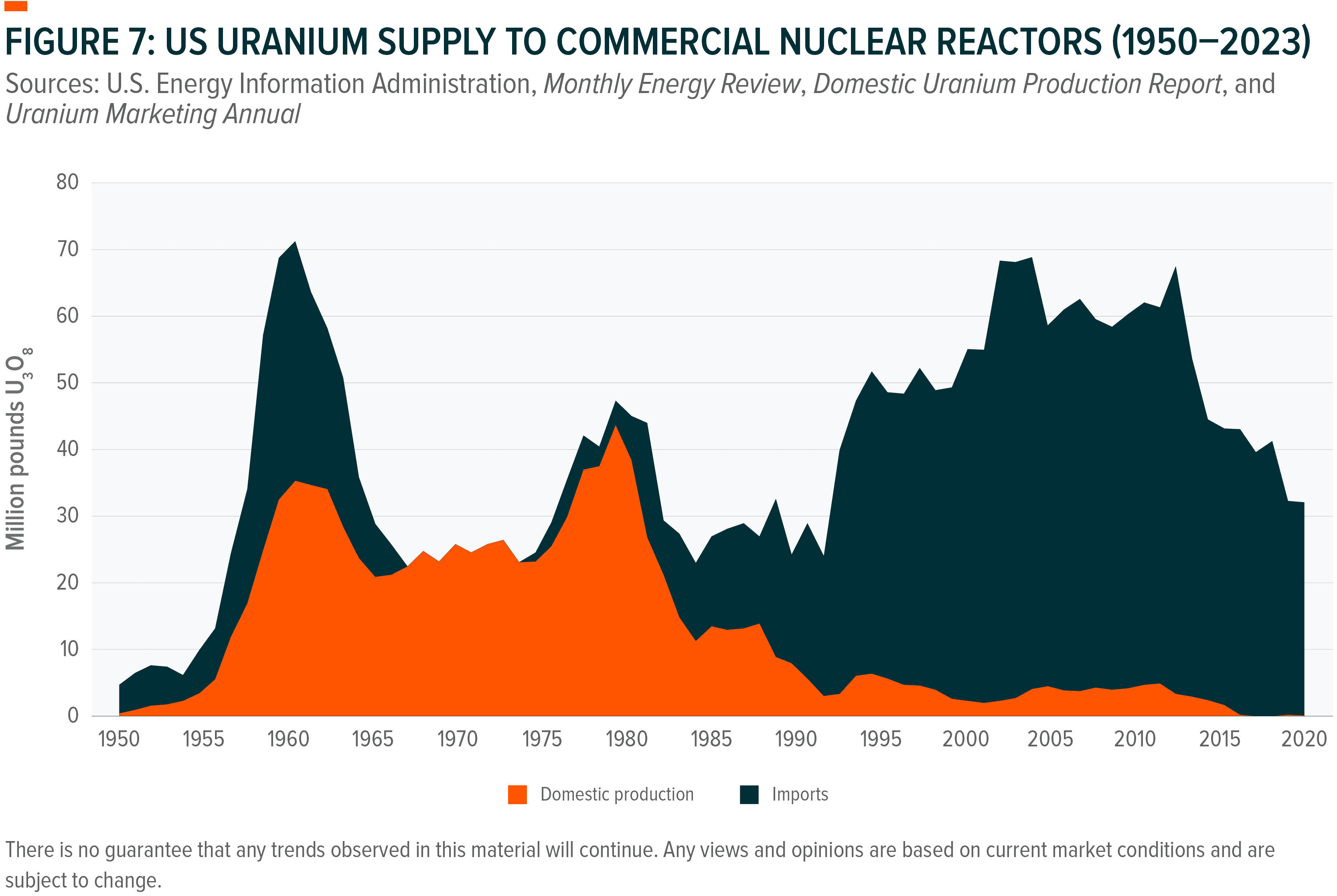

Fuel costs represent a small share of total nuclear operating costs, while fuel availability is existential to reactor operation.²⁹ As a result, utilities prioritise security of supply over price optimisation, particularly once reactors are operating or extended.³⁰

Because the market is small, supply-constrained, and dominated by price-insensitive buyers:

This creates a more infrastructure-like return profile than previous nuclear cycles.

Uranium demand is binary and contractual –once fuel is committed, demand becomes highly inelastic, limiting downside elasticity relative to other commodities.⁴³

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1 International Energy Agency (IEA) (2025) Global Energy Review 2025

2 Bank of America Institute (2026) Nuclear energy: Who, what, where, when, why?

3 BloombergNEF (2024) Clean Electricity Breaks New Records; Renewables on Track for Another Strong Year: BloombergNEF

4 U.S. Department of Energy (2025) What is Generation Capacity?

5 Nuclear Energy Agency (2024) Uranium: Resources, Production and Demand

6 Ibid

7 Ember (2025) Demand and supply changes in 2024

8 IEA (2025) Energy demand from AI

9 North American Electric Reliability Corporation (NERC) (2025) 2024 Long-Term Reliability Assessment

10 Ibid

11 Ibid

12 Ibid

13 World Nuclear Association (2026) Nuclear Power in the World Today

14 Ibid

15 IEA (2023) Nuclear Power and Secure Energy Transitions

16 U.S. Department of Energy (2024) Civil Nuclear Credit Program

17 Ibid

18 Ibid

19 World Nuclear Association (2026) Nuclear Power Reactors

20 Ibid

21 Ibid

22 Ibid

23 World Nuclear News (2026) Meta announces ‘landmark’ agreements for new nuclear

24 Ibid

25 U.S. Department of Energy (2025) HALEU Availability Program

26 Ibid

27 Ibid

28 Ibid

29 World Nuclear Association (2023) Economics of Nuclear Power

30 T. Rowe Price (2025) Restoring America’s nuclear energy capacity—Digging in to potential impacts and implications

31 U.S. Energy Information Administration (2025) U.S. nuclear generators import nearly all the uranium concentrate they use

32 Centrus (2025) Centrus Energy Secures Contract Extension from Department of Energy to Continue HALEU Production

33 Ibid

34 Reuters (2026) Westinghouse megadeal set to revitalize nuclear supply chain

35 Reuters (2026) US awards $2.7 billion worth of orders to boost uranium enrichment

36 Ibid

37 Ibid

38 Ibid

39 Ibid

40 Ibid

41 Ibid

42 Ibid

43 Ibid