Europe

Marketing Communication. Capital at risk. For Professional Investors Only.

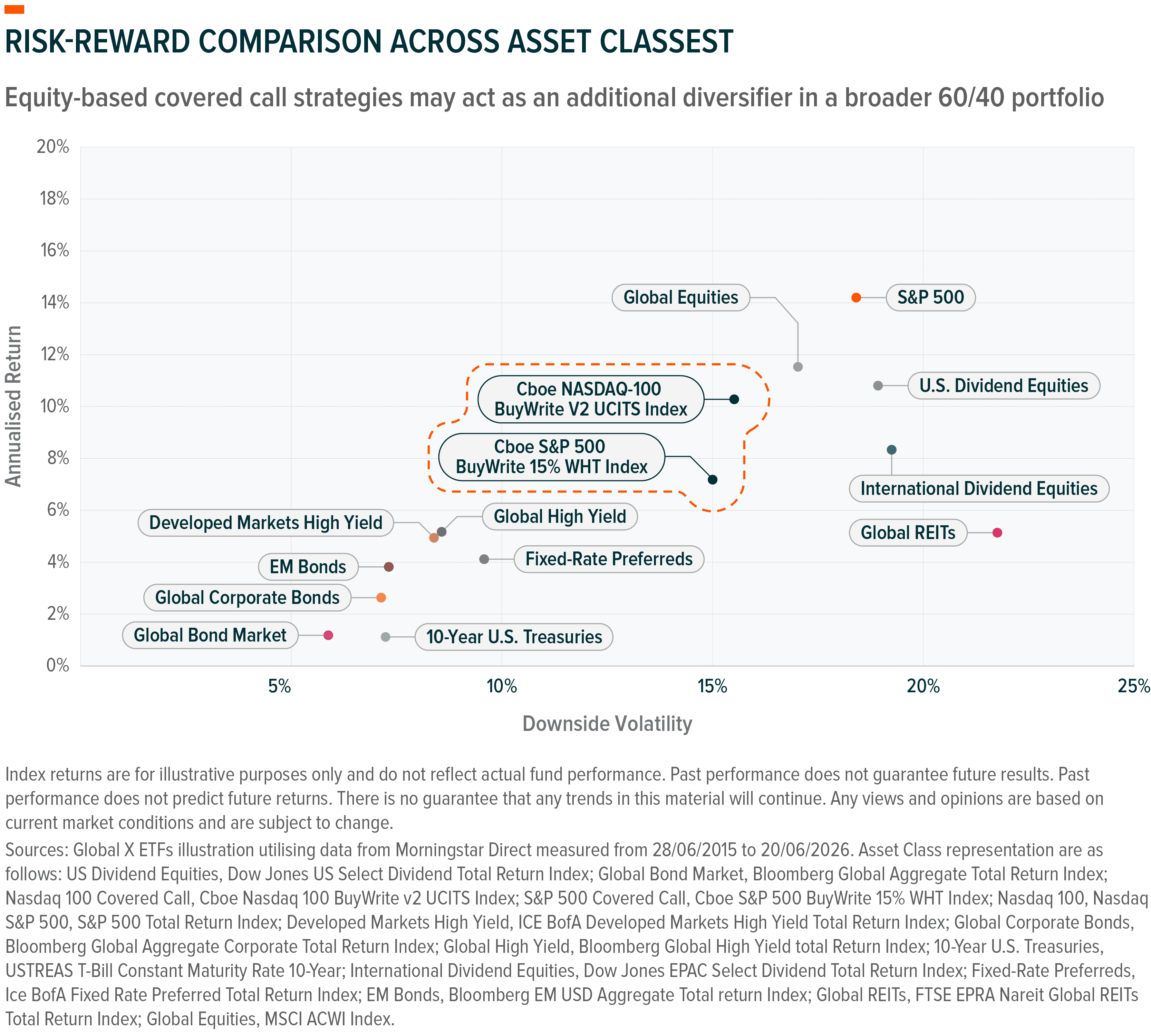

Systematic option writing may be an overlooked tool in institutional portfolio construction. It is designed to leverage sources that conventional portfolios largely leave on the table, the volatility risk premium embedded in equity index options. As allocators reassess the diversification assumptions that underpinned the classic 60/40 framework, covered call strategies may offer a mechanism to extract that premium efficiently, at scale, and within a familiar UCITS structure.

Passive equity allocations are not as diversified as they appear. The top ten constituents accounted for approximately 36% of index weight, more than double their share a decade ago, and a level of concentration with few historical precedents.³ When sentiment in that cohort shifts, drawdowns can be swift and disproportionate to any deterioration in the broader economy.

The Warsh Fed has abandoned forward guidance entirely, with the committee now tilting toward hikes rather than cuts and the inflation outlook remaining high and sticky.⁴ Those seeking fixed income yield are simultaneously absorbing duration risk at a moment when the rate path is, by design, unpredictable.

Premium income is derived from implied volatility rather than from credit spreads, dividend yields, or rate sensitivity.⁵ It requires no directional view on rates and no exposure to corporate earnings cycles. Crucially, the removal of Fed forward guidance may re-anchor short-end volatility structurally higher, lifting implied vol across the surface, with wider vol bands potentially translating directly into larger option premiums.⁶ The income cushion may improve the strategy's risk-adjusted total return profile relative to unhedged equity exposure, particularly in volatile or range-bound markets where premium income is highest and index gains are modest.

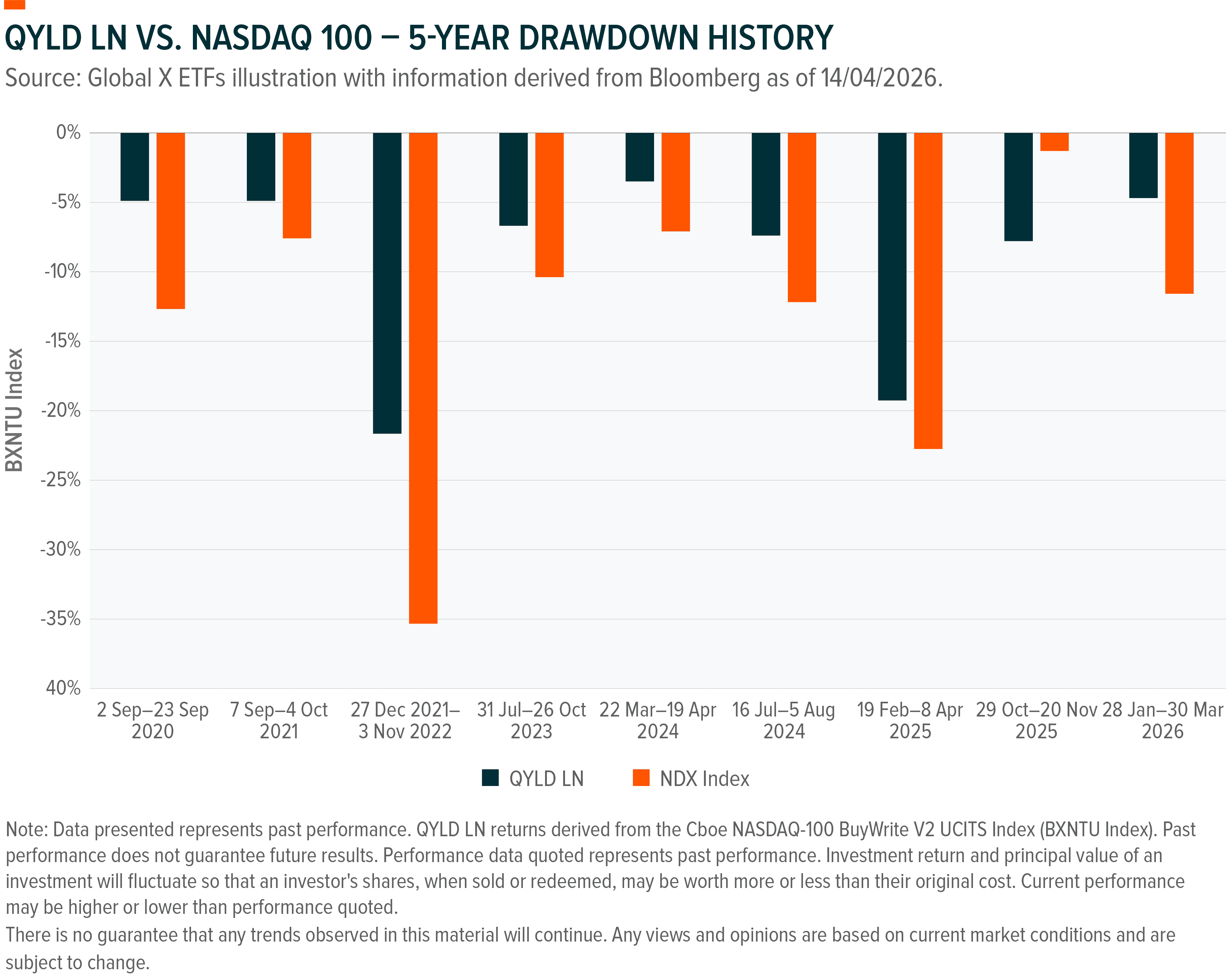

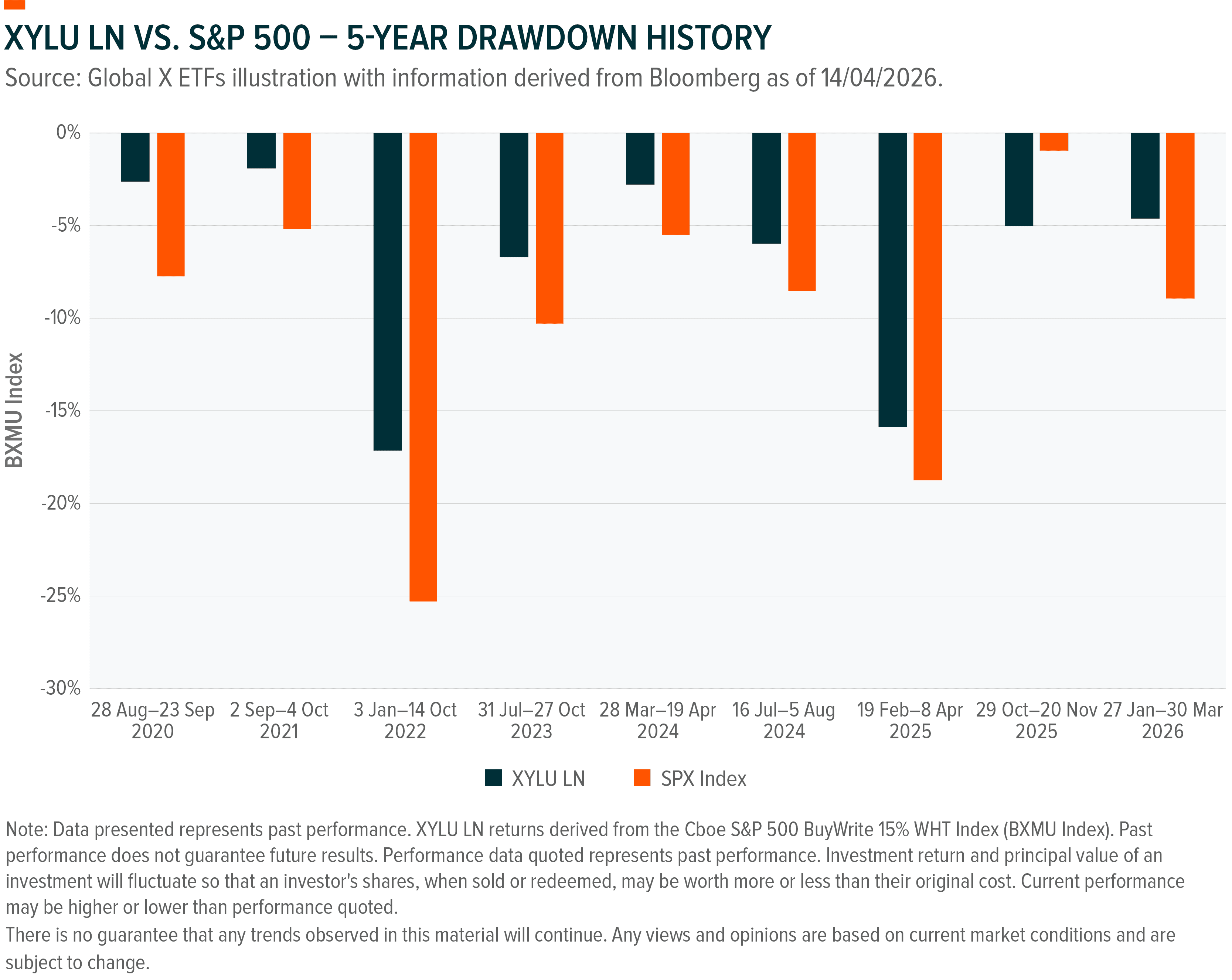

A covered call strategy holds a long position in an equity index, either physically or via a total return swap and periodically writes call options on that same index, typically on a monthly, weekly or daily basis. The premium received is the strategy's primary income source. Call option writing generates a premium and in exchange, the strategy caps its upside participation at the option's strike price for the life of the option contract. If the index closes below the strike at expiry, the option expires worthless and the strategy retains the full premium. If the index closes above, the gains on the underlying equity exposure are offset by the payout on the short call. Either way, the premium received reduces the strategy's downside somewhat relative to an unhedged equity position. The result is a strategy with meaningfully lower equity beta than an unhedged index position. At the money implementations have historically exhibited beta in the 0.50 to 0.60 range, making covered calls a structurally lower volatility way to maintain equity market exposure.⁷

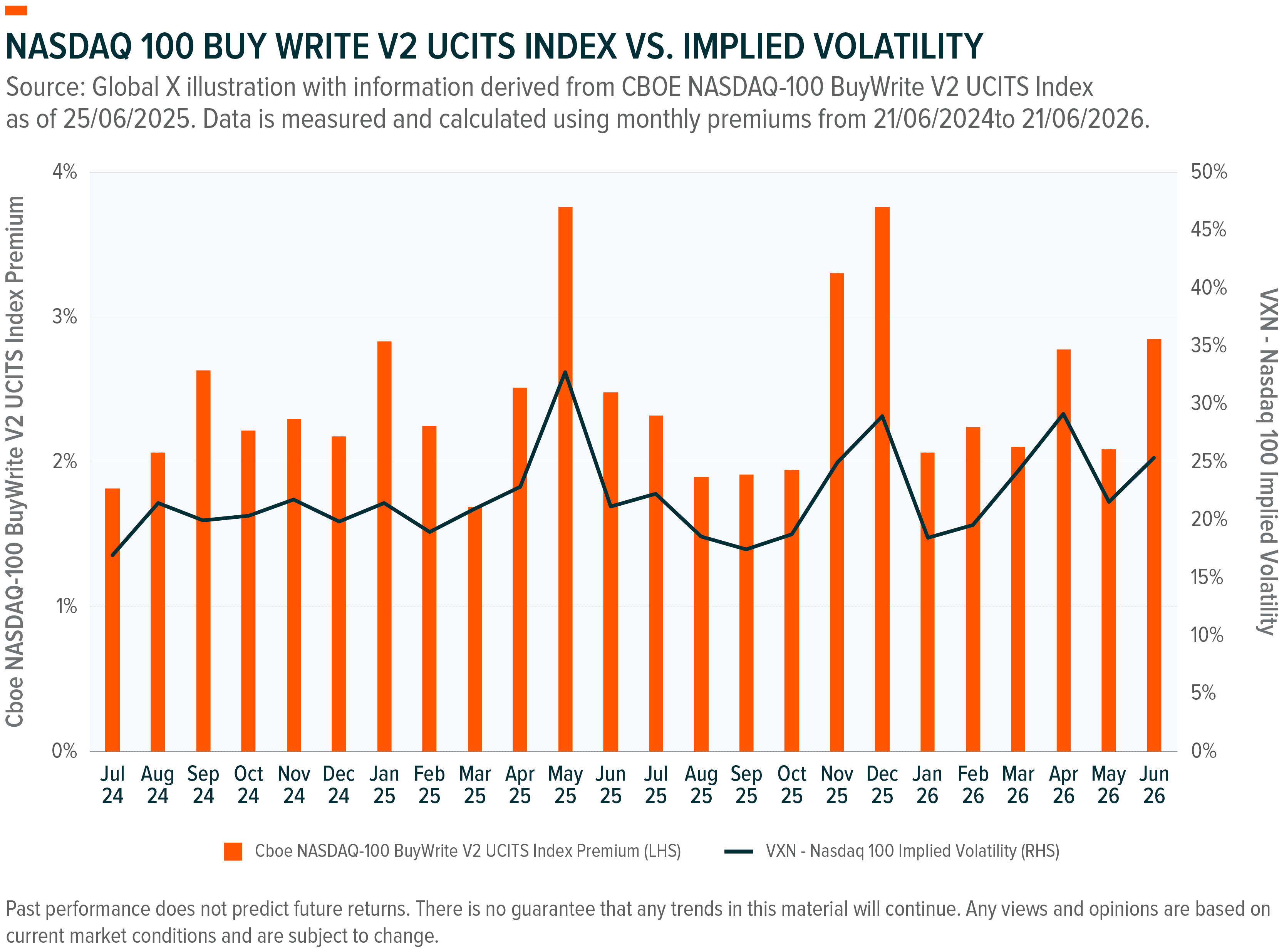

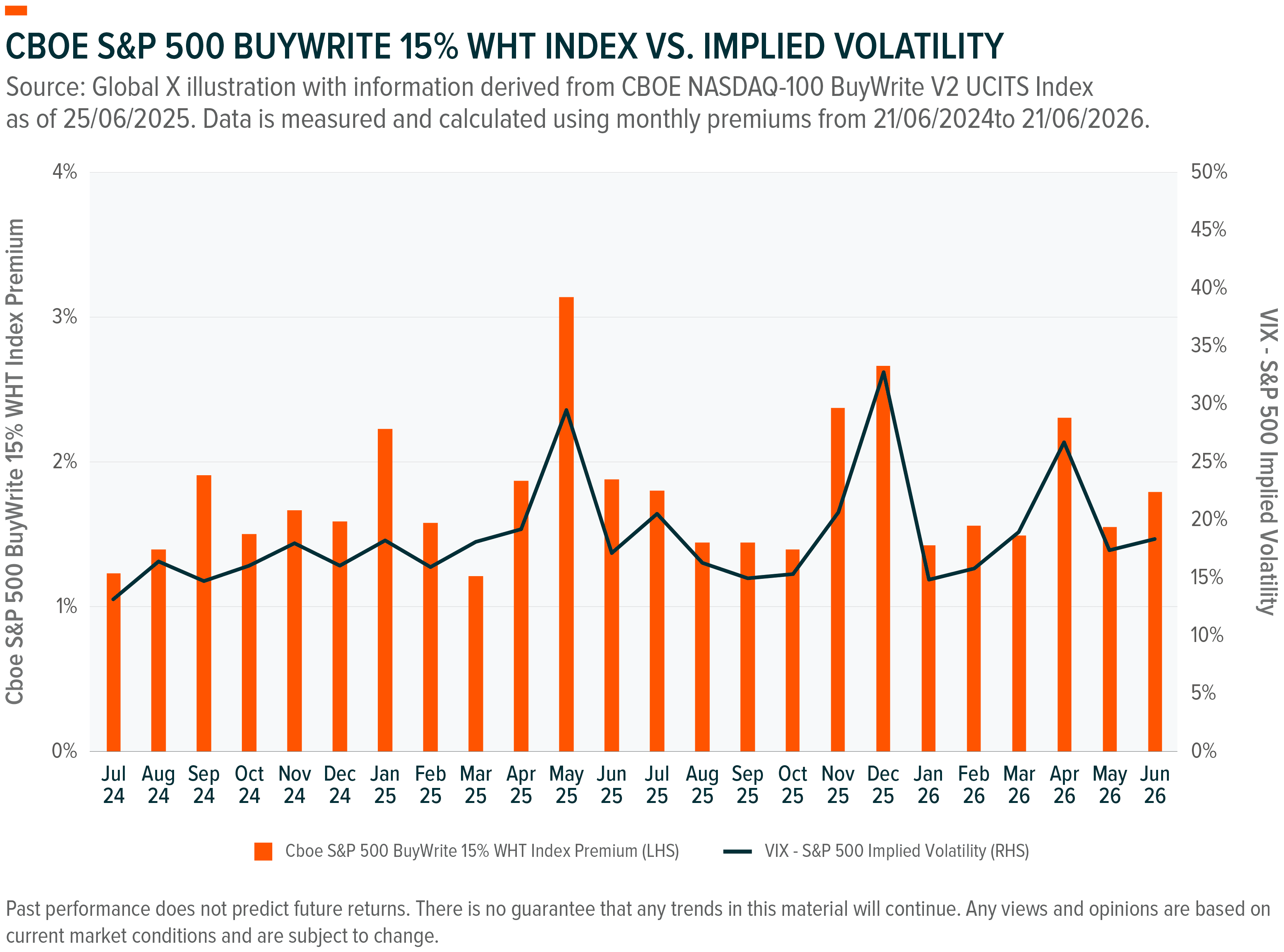

The size of the premium, and therefore the income yield is primarily determined by implied volatility (IV).⁸ Options are priced to reflect the probability distribution of future index moves, when volatility expectations are elevated, option premiums expand, and the income a covered call strategy can generate is correspondingly higher. This is the mechanism that makes covered calls particularly relevant in more volatile environments. Macro uncertainty around rates, geopolitical risk, and event-driven market moves can all contribute to sustained periods of elevated IV, meaning the income available from systematic option writing could be meaningfully higher than in lower-volatility regimes.⁹ This dynamic, monetising the volatility of the underlying index through systematic option writing, is what distinguishes covered calls from conventional income strategies. The premium is compensation for volatility exposure, not credit or duration risk. The Nasdaq 100 is especially well-suited to this approach as it has structurally higher volatility relative to the S&P 500, which has historically translated into larger premiums at comparable strike levels.¹⁰

The income profile can be further shaped by three design variables. Strike selection determines the trade-off between income and retained upside. At-the-money (ATM) writes collect the highest premium but sacrifices all near-term index participation, while out-of-the-money (OTM) writes preserve some upside at the cost of a lower premium. Notional coverage determines what proportion of the equity exposure is overwritten; higher coverage raises income but caps a greater share of the underlying position. The option roll frequency affects how quickly time decay is captured and how sensitive the strategy is to changes in the volatility surface between resets. Passive index-replication frameworks fix these parameters systematically whilst active strategies adjust them dynamically in response to the prevailing options environment.

The asset base for covered call strategies has grown substantially. Covered call UCITS ETF assets under management reached approximately $7.83 billion as of June 2026, underpinned by $1.77 billion in cumulative YTD inflows.¹¹ Nasdaq 100 linked strategies account for the largest share, reflecting the index's structural advantages for premium generation, meaningfully higher realised and implied volatility than the S&P 500, combined with some strategies allowing for market participation that preserves residual upside even after the call overlay is applied.¹² Covered calls are the dominant driver of European option-ETF demand at this stage of the adoption cycle.¹³

Global X ETFs Europe has built out a UCITS covered call suite spanning four at the money systematic call writing strategies on the Nasdaq-100 (QYLD LN), S&P 500 (XYLU LN), Euro Stoxx 50 (SYLD LN), and DAX (DYLD LN), with a combined AUM of approximately €1.11 billion as of May 2026.¹⁴

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Global X with data derived from Bloomberg Terminal for State Street SPDR S&P 500 ETF Trust as of 25 June 2026.

2. Global X with data derived from ETF Book classified as option-based strategies filtered down to Covered Call UCITS ETFs as of 25 June 2026.

3. Ibid.

4. CNBC. Here are the five big takeaways from Kevin Warsh’s first meeting as Fed chairman. 17 June 2026.

5. Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy, 81(3), 637-654.

6. Financial Times. Kevin Warsh’s push to axe Fed guidance may lift US borrowing costs, investors warn. 21 June 2026.

7. Global X illustration with information derived from Bloomberg Terminal as of 29 June 2026. Data is measured as weekly beta over a two year period from 29 June 2024 to 29 June 2026 for 1) Cboe NASDAQ-100 BuyWrite V2 UCITS Index against the Nasdaq 100; 2) Cboe S&P 500 BuyWrite 15% WHT against the S&P 500; 3) EURO STOXX 50® Covered Call ATM against the Eurostoxx 50 and 4) DAX Covered Call ATM Index against the DAX Index.

8. Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy, 81(3), 637-654.

9. Penn Mutual Asset Management. When Fear Leads Reality: Inside 2026’s Volatility Surge. 26 March, 2026.

10. Yahoo Finance. CBOE NASDAQ 100 Volatility (VXN) and CBOE Volatility Index (VIX) historical data. As of 29 June 2026.

11. Global X with data derived from ETF Book classified as option-based strategies filtered down to Covered Call UCITS ETFs as of 25 June 2026.

12. Ibid.

13. Ibid.

14. Ibid.