Europe

Marketing Communication. Capital at risk. For Professional Investors Only. Please read fund legal documentation before making any final investment decisions.

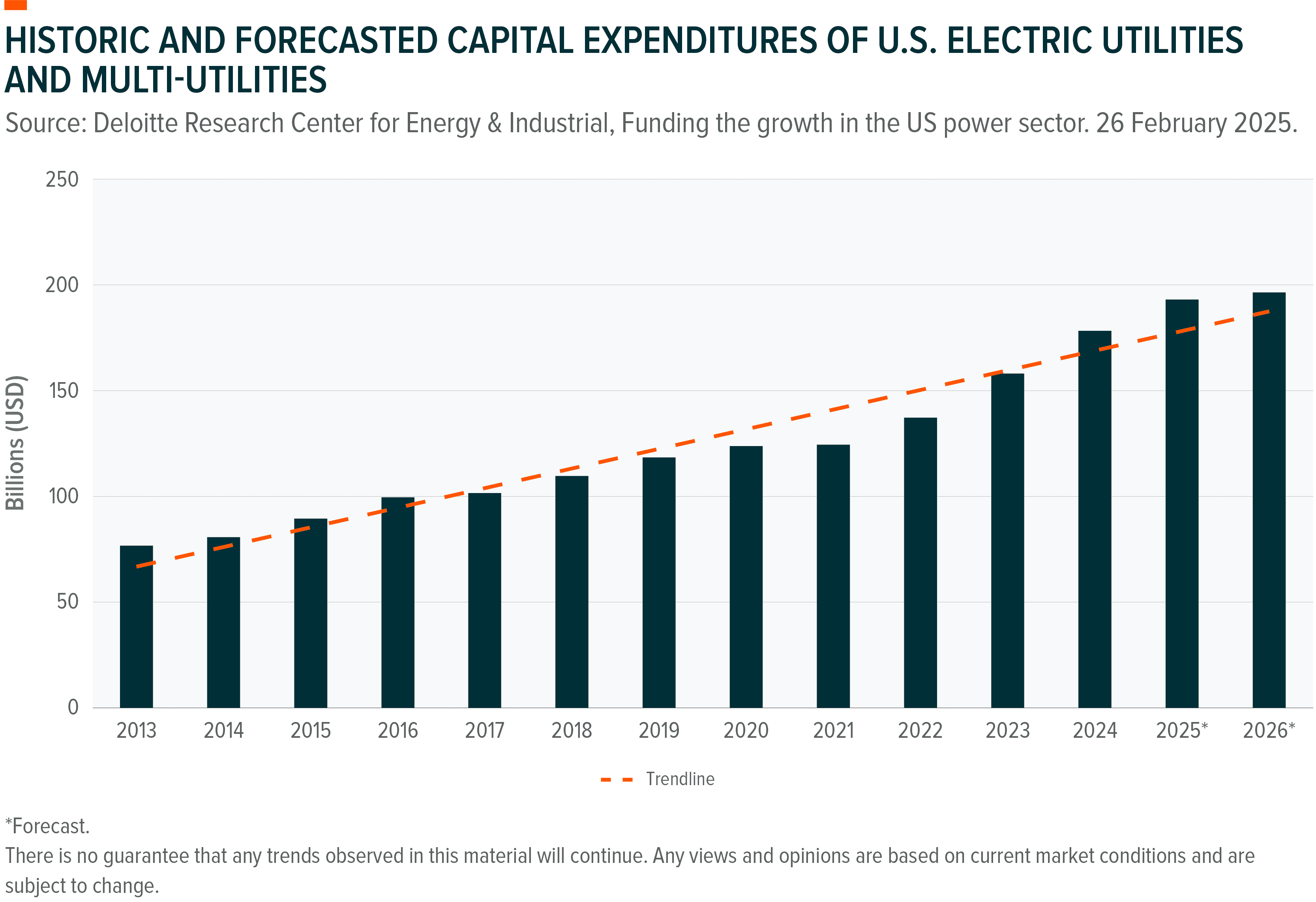

The U.S. power landscape is rapidly changing. After two decades of near-flat growth, U.S. electricity demand is projected to increase by as much as 50% between 2024 and 2040, driven by AI data centres, manufacturing, and electric vehicles.¹ Meeting expanding power needs will likely require a significant buildout of both power generation facilities and power grid infrastructure. U.S. utilities plan to spend at least $1.4 trillion between 2025 and 2030 to grow electricity generation and power grid capacity across the country.²

The Global X U.S. Electrification UCITS ETF (ZAPP LN) seeks to offer investors an opportunity to capture growth across the electricity value chain, from grid infrastructure developers and smart grid technology providers to traditional and alternative electricity generators. Below, we highlight some of the key trends that are driving the dramatic transformation of the U.S. power industry.

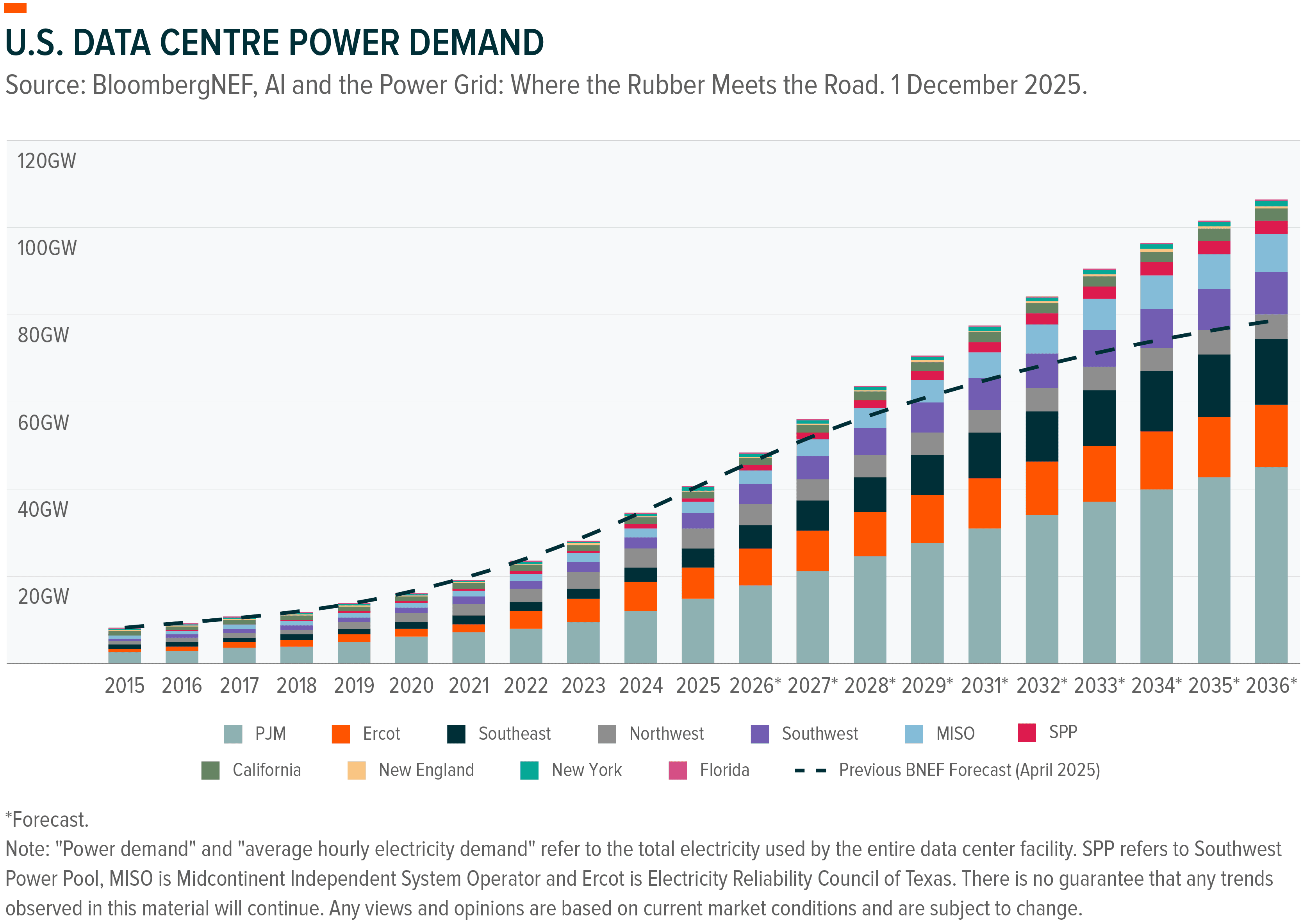

According to the U.S. Department of Energy, data centres could consume as much as 12% of U.S. electricity by 2028, which would be 3x higher than the 4.4% share in 2023.⁶ There are two key reasons behind the explosive power demand growth: 1) more data centres are needed to support AI adoption, and 2) AI data centres are often more power-intensive than traditional data centres. A traditional rack in a data centre is equivalent to the electricity consumption of three houses, while a high-density rack for AI uses electricity equivalent to 80-100 homes.⁷

Given these dynamics, expanding and modernising the power grid is likely essential for the U.S. to maintain economic competitiveness and leadership as AI advances. The speed at which U.S. utilities and other power generators can respond could determine whether the U.S. power grid becomes a constraint or enabler for the development of AI-related infrastructure, such as data centres and semiconductor manufacturing facilities.

In short, the dependent relationship between electricity and AI data centres implies that “electricity is intelligence,” and that the power grid is central to the advancement of AI.⁸ In October 2025, Microsoft CEO Satya Nadella said that “the biggest issue we are now having is not a compute glut, but it’s power – it’s sort of the ability to get the builds done fast enough close to power.”⁹ This may create sizeable opportunities for companies throughout the electrification value chain as AI becomes increasingly engrained in the U.S. economy.

Besides AI, rising industrial activity and the steady electrification of vehicles are projected to expand U.S. electricity demand.¹⁰

Manufacturing: The growth of U.S. manufacturing is also likely to come with a steep power cost. Production facilities can consume large amounts of power, and this is particularly noticeable for strategic industries like semiconductors. TSMC’s first semiconductor fabrication facility in Arizona requires an estimated 2.85GWh of electricity per day, equivalent to the needs of about 100,000 homes.¹¹ The company is reportedly planning to build six fabs total in the Phoenix area, and dozens more are being planned throughout the U.S. by other manufacturers.¹²,¹³

In total, electricity consumption from the industrial sector is forecast to increase 2.1% in 2025 and 3.0% in 2026, compared to 2.2% growth in 2024 and a 1.1% decline in 2023.¹⁴ As a result, the industrial sector’s share of total U.S. electricity consumption is forecast to hold steady at around 25%, even with the growing demand in commercial electricity use from data centres.¹⁵

Electrification of Vehicles: Electric vehicles (EVs) are projected to become an increasingly significant driver of U.S. electricity demand over the next 15 years, with electrification expected to accelerate in the mid-2030s.¹⁶ By 2040, EVs are forecast to reach 10% of total energy demand in the United States.¹⁷ The regions with the most EV demand are expected to be the Northeast, Southeast, and California.

Growing power consumption will likely need to be met by expanding a range of power sources, including nuclear power, renewable energy, and behind-the-meter solutions.

Nuclear Power: Hyperscalers have begun to increasingly explore nuclear power as a solution given that it is a reliable, zero-carbon electricity source.¹⁸ In the past couple of years, tech companies have begun to sign power purchase agreements (PPAs) for both traditional and next-gen nuclear power projects to help meet their growing data centre power needs.¹⁹ In October 2025, for example, Google signed a 25-year PPA with NextEra to secure power from the currently-shuttered Duane Arnold Nuclear Power facility in Iowa, which is now expected to restart in 2029.²⁰ In June 2025, Constellation and Meta signed a 20-year PPA for the 1,121-megawatt (MW) Clinton nuclear power plant in Illinois to support Meta’s operations, beginning in 2027.²¹ In the same month, Amazon and Talen Energy signed a 1,920MW PPA to use the utility’s Susquehanna nuclear power plant in Pennsylvania to power Amazon Web Services’ (AWS) data centres in the region.²² Small modular reactor (SMRs) developers, such as NuScale, have also signed agreements to potentially supply power to U.S. data centres in the future.²³

Renewable Energy: Renewable energy systems also remain viable solutions for both utilities and large load customers due to their scalability, ability to be built close to demand centres, cost competitiveness relative to other power sources, and shorter development timeframes. Solar power alone is projected to account for 52% of new electricity generating capacity from U.S. developers in 2025.²⁴ Solar is also the leading technology for corporate power purchases from hyperscalers. Between January and November 2025, a combined 9.7GW of solar power was contracted by Amazon, Google, Meta, and Microsoft, followed by 1.5GW of wind power, nearly 3.6GW of nuclear power, and nearly 1GW of other sources, such as geothermal and hydropower.²⁵

Behind-the-Meter (BTM) Solutions: BTM solutions, including onsite energy storage systems and hydrogen fuel cells, can help data centre operators and other large electric consumers address some of the potential challenges within the U.S. power grid. Battery energy storage systems can help meet some of the power demand and provide backup solutions, alleviating pressure on the grid. As a result, companies with BTM solutions can potentially secure a faster interconnection to the grid. For example, Aligned Data Centers was able to get a connection for one of its data centres that is “years earlier than would be possible with traditional utility upgrades,” due to the expected benefits of having a 31MW/62MWh battery onsite.²⁶

The hydrogen industry is also gaining momentum as an onsite power solution. In October 2025, Bloom Energy and Brookfield announced a $5 billion partnership to use Bloom’s fuel cells as onsite power solutions at Brookfield’s data centres.²⁷ Brookfield’s Global Head of AI Infrastructure stated that, “this partnership adds a powerful new tool to our global growth strategy, especially in a grid-constrained market environment.”²⁸

In 2025 and 2026, U.S. utilities and multi-utilities companies could spend $194 billion and $197 billion, respectively, on power generation assets and grid infrastructure. Between 2025 and 2030, investments from utilities could total $1.4 trillion, which would be about double the amount invested over the past 10 years.²⁹ Based on a September 2025 report, utilities expect 60GW of large load capacity growth through 2030, and 93GW by 2035.³⁰

In addition to rising demand, many utilities are facing the need to replace or modernise ageing infrastructure assets, with nearly half of transmission assets at least 20 years old.³¹ U.S. utilities also face growing risks from extreme weather and climate change. In the first half of 2025, 48% of utility customers in the United States experienced a power outage, and extreme weather caused nearly half of the outages.³²

Meeting future power needs from data centres, manufacturing facilities, and EVs likely requires large-scale deployment of grid infrastructure and power generation assets across the United States. Nuclear power, renewable energy, energy storage, and hydrogen fuel cells are among the solutions that utilities and companies can utilise to meet rising demand. For investors, we believe This could create an opportunity throughout the entire U.S. electrification value chain, from grid developers and technology developers to the traditional and alternative electricity generators.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. American Clean Power (ACP), U.S. National Power Demand Study. March 2025.

2. Deloitte Research Center for Energy & Industrials, Funding the growth in the US power sector. 26 February 2025.

3. American Clean Power (ACP), U.S. National Power Demand Study. March 2025.

4. Hostert, D., Kimmel, M., Berryman, I., Pegios, K., Quintero, R., Song, S., Verma, A., & Vasdev, A., BloombergNEF, New Energy Outlook: Energy and Climate Scenarios that Connect the Dots. 15 April 2025.

5. Deloitte Research Center for Energy & Industrials, Funding the growth in the US power sector. 26 February 2025.

6. Lawrence Berkeley National Laboratory, 2024 United States Data Center Energy Usage Report. December 2024.

7. S&P Global Market Intelligence, The AI Supercycle – A Catalyst for Datacenter and Energy Evolution. 18 September 2025.

8. Partridge, B. & Yergin, D., Fireside Chat with Daniel Yergin. Datacenter & Energy Innovation Summit 2025, Washington, DC. 18 September 2025.

9. Gerstner, B. (Host), Spotify, All things aI w @altcap @sama & @satynadella. A Halloween Special. BG2 w/ Brad Gerstner. [Audio podcast episode]. In BG2Pod with Brad Gerstner and Bill Gurley. 31 October 2025.

10. American Clean Power (ACP), U.S. National Power Demand Study. March 2025.

11. Tarasov, K., CNBC, TSMC says first advanced U.S. chip plant ‘dang near back’ on schedule. Here’s an inside look at the Arizona fab. 13 December 2024.

12. Taiwan Semiconductor Manufacturing Company (TSMC), TSMC Arizona. Accessed December 12, 2025.

13. Z2 Data, Where Are All The North American Semiconductor Fabs Being Built (2024 Edition)? 4 October 2024.

14. U.S. Energy Information Administration, Short-Term Energy Outlook. 7 October 2025.

15. Ibid.

16. American Clean Power (ACP), U.S. National Power Demand Study. March 2025.

17. Ibid.

18. S&P Global Market Intelligence, The AI Supercycle – A Catalyst for Datacenter and Energy Evolution. 18 September 2025.

19. Bird & Bird, Nuclear Project PPAs. 2 December 2025.

20. Google, Our new agreement with NextEra Energy will bring Iowa’s only nuclear plant back to life. 27 October 2025.

21. Constellation, Constellation, Meta sign 20-Year Deal for Clean, Reliable Nuclear Energy in Illinois. 3 June 2025.

22. UtilityDive, Talen to sell Amazon 1.9 GW from Susquehanna nuclear plant. 11 June 2025.

23. NuScale, NuScale Proudly Supports TVA and ENTRA1 Energy Announcement of Landmark 6-Gigawatt Small Module Reactor (SMR) Deployment Program. 3 September 2025.

24. U.S. Energy Information Administration, Short-Term Energy Outlook. 7 October 2025.

25. BloombergNEF, Corporate PPA Deal Tracker. November 2025. 9 December 2025.

26. LatitudeMedia, Data centers are beginning to embrace batteries for onsite power. 3 November 2025.

27. Bloom Energy, Brookfield and Bloom Energy Announce $5 Billion Strategic AI Infrastructure Partnership. 13 October 2025.

28. Ibid.

29. Deloitte Research Center for Energy & Industrials, Funding the growth in the US power sector. 26 February 2025.

30. Wood Mackenzie, US utilities have committed to 116GW of large load capacity growth, equal to 15.5% of current US peak demand. 4 September 2025.

31. International Energy Agency (IEA), Building the Future Transmission Grid. 25 February 2025.

32. J.D. Power, Disasters Become a Fact of Life for Many U.S. Electric Utility Customers. October 2025.