Europe

Loading...

During the first half of 2024 markets found support in the form of decelerating inflation, resilience in jobs, and strong positive revenue revisions for major players in the tech space. The breadth of this rally was narrow, driven by a small constituency of mega-cap names in the Nasdaq 100 Index. However, now that share gains have grown more broad based, where markets may go from here and what investors can do in them represent some big questions. In this environment that features higher valuations, covered call option strategies could make available opportunities to mitigate volatility associated with equity allocations and may generate current income.

Accounts that maintained a healthy exposure to Nasdaq 100 Index constituents despite all the market uncertainty in early 2024 were well rewarded.2 The index has taken a step back in value during April 2024, only to recover and once again trade in the vicinity of its 52-week high. The widely oscillating pricing patterns underscore the high levels of volatility under which the Nasdaq 100 has historically been categorised. And though these periods, amounting to relatively flat growth, may be acceptable in the eyes of investors with a longer time horizon, or those that are comfortable with a bumpy ride on the path to growth, income-driven investors and those seeking to reduce volatility within their respective portfolios might find these peaks and valleys somewhat less appealing.

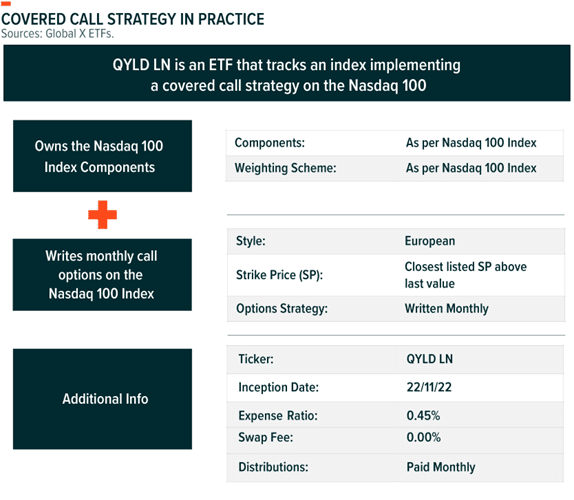

With a covered call option strategy, those who prefer a more conservative approach have the opportunity to take positions in the Nasdaq 100, gaining exposure to a broader base of equities that might not typically be found in baskets of assets designed to produce income. Indeed, with many of the information technology and consumer discretionary companies that make up the Nasdaq 100 unlikely to offer a dividend, income investors are usually less inclined to seek out these positions. However, by harnessing the implied volatility that is associated with the Nasdaq 100 to drive option premiums this becomes a more feasible prospect and risk could be diversified across these potentially less-frequently pursued arenas. The Global X Nasdaq 100 Covered Call UCITS ETF (QYLD LN) may offer a path by which to obtain this exposure. Tracking an index that seeks to generate income by harnessing a covered call strategy, its performance can be observed using its indicated yield relative to some of the more conventional asset classes that would typically be employed.

Pairing a covered call strategy with a broader equity strategy, thereby duplicating exposures to Nasdaq 100 constituents, might seem counterintuitive at first glance when trying to mitigate risk. However, the at-the-money covered call strategy incorporated by the index that the covered call strategy seeks to track could monetise the Nasdaq 100’s volatility to create opportunities that may act as somewhat of a volatility mitigator. That potential income could also supplement an existing growth strategy while offering a portfolio a positive relationship with volatility.

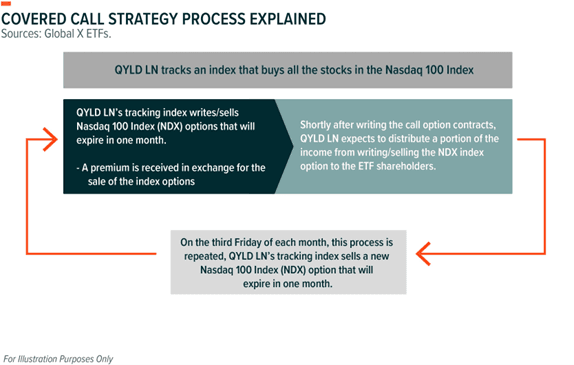

The Global X Nasdaq 100 Covered Call UCITS ETF seeks to track the Cboe NASDAQ-100 BuyWrite v2 UCITS Index (BXNTU). This is an index that operates a rules-based investment policy, including a covered call option overlay. BXNTU’s covered call strategy works in the same way that it might for an individual investor that wants to maintain holdings on a single equity and then write calls on that position to generate income. BXNTU simply uses the broader Nasdaq 100 index as its reference asset and writes its call options against the broader index in exchange for the options’ premiums.

BXNTU operates a covered call strategy that covers 100% of its notional portfolio by selling Nasdaq 100 (NDX) index call options, as opposed to writing options on all the stocks that make up the Nasdaq 100 individually. The index uses European style options that cannot be executed by the purchaser until the contract reaches its expiration date, so it may maintain its systematic approach, writing at-the-money options on a monthly basis.

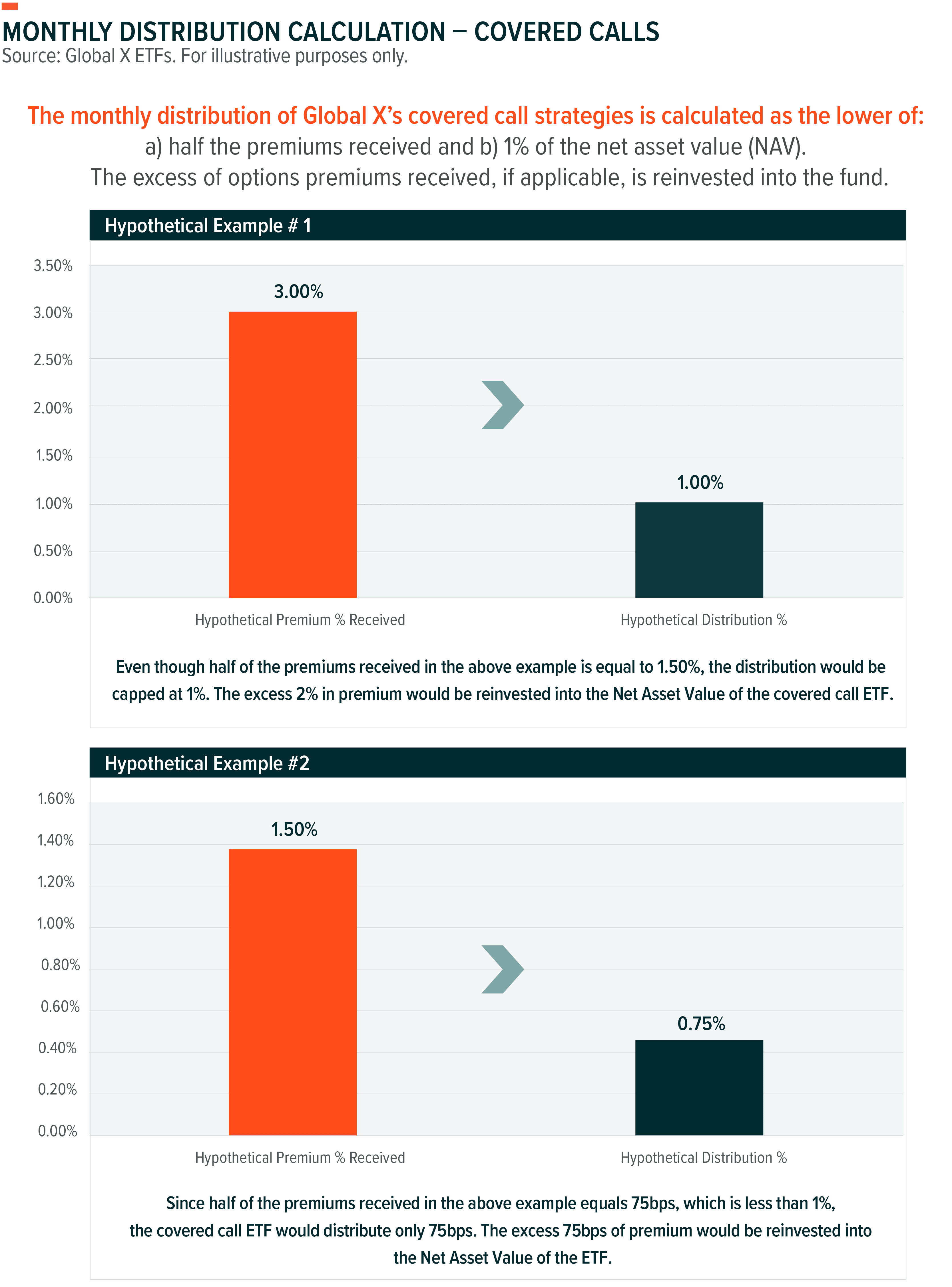

Each month, BXNTU writes calls that are at the money. This means that, at initiation, the strike price of the call is intended to equal the value of the underlying index. If a contract with a strike price that is precisely at-the-money is not available to be sold, BXNTU will seek to write its call options at the closest possible strike price to the reference index’s value that is out of the money. The strategy may allow BXNTU to attract the highest possible premiums for its written calls without selling contracts that are already in a position to potentially be exercised. Based on the premiums that BXNTU is able to attract, QYLD LN implements a distribution policy that will see it distribute in the form of an accumulating share class half of the value of the premiums received or 1% of the fund’s net asset value, whichever is lower. The balance of the premium value is then expected to be reinvested back into QYLD LN.

Tracking an index that writes call options against 100% of the value of its portfolio, QYLD LN forgoes the possibility of realising the capital appreciation generated by the Nasdaq 100 Index. The fund operates in this way so that it may benefit as the index seeks the highest possible premiums in exchange for calls written. It then makes its distributions from its stockpile in an effort to produce a competitive yield.

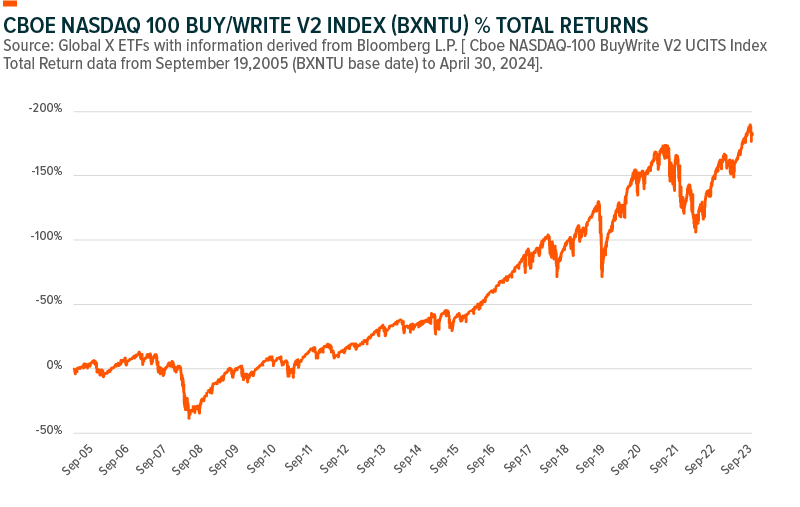

There is latitude in how the potential income that may be generated by a position in QYLD LN could be used. That said, this income is oftentimes absent from the fund’s price chart when displayed across various investment research platforms. This undertaking might result in QYLD LN displaying a negative price trend since its inception. However, the potential opportunity for reinvestment might be important to consider. Looking at the total returns of BXNTU from its base date, with 100% of all premiums reinvested back into the index, may give a differentiated understanding of QYLD LN’s potential capabilities.

Past performance is not a guarantee of future results.

The Global X Nasdaq 100 Covered Call UCITS ETF operates under the methodology that its distributions are made as a function of an accumulating share class. As such, aforementioned efforts to reinvest potential income are more streamlined than some funds that might make distributions in cash. Reinvestment into QYLD LN provides it the opportunity to leverage BXNTU’s covered call writing strategy more aggressively, potentially boosting NAV and creating a broader notional balance on which the index can sell contracts. This contributes to the trend that is exhibited in the total return chart provided above, which highlights how shareholders could benefit should all distributions have been reinvested and remained a part of NAV since the index’s inception.

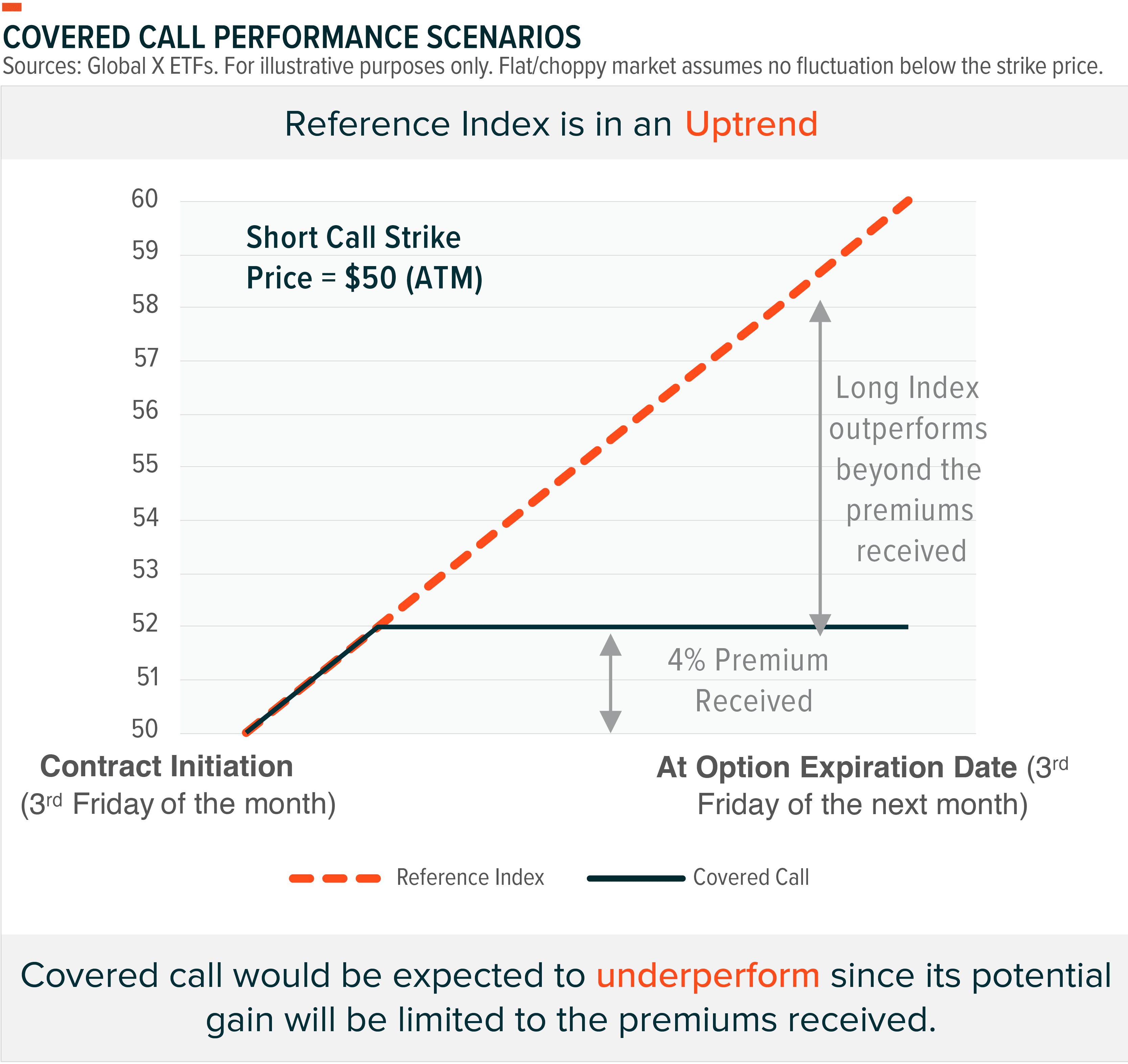

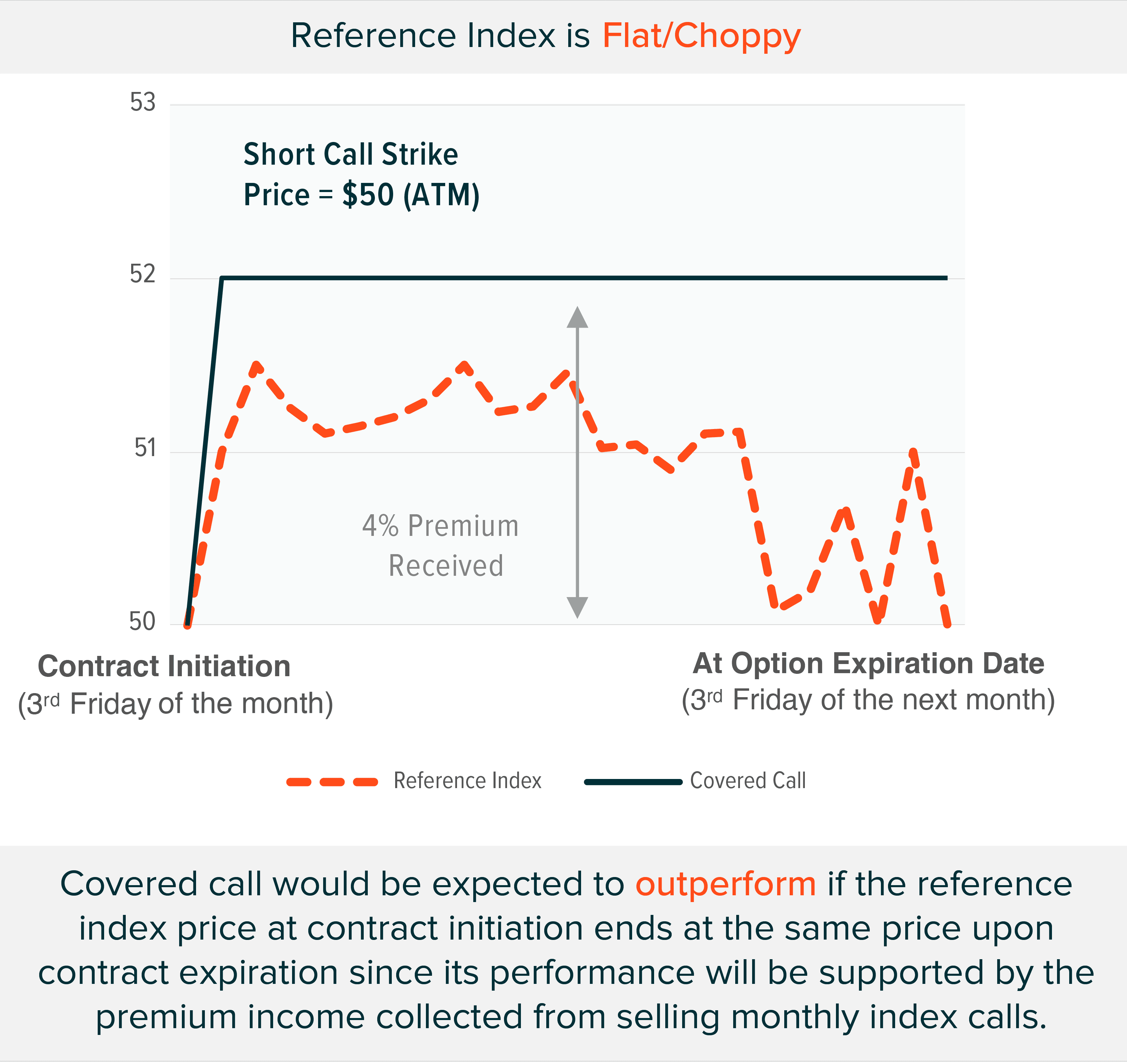

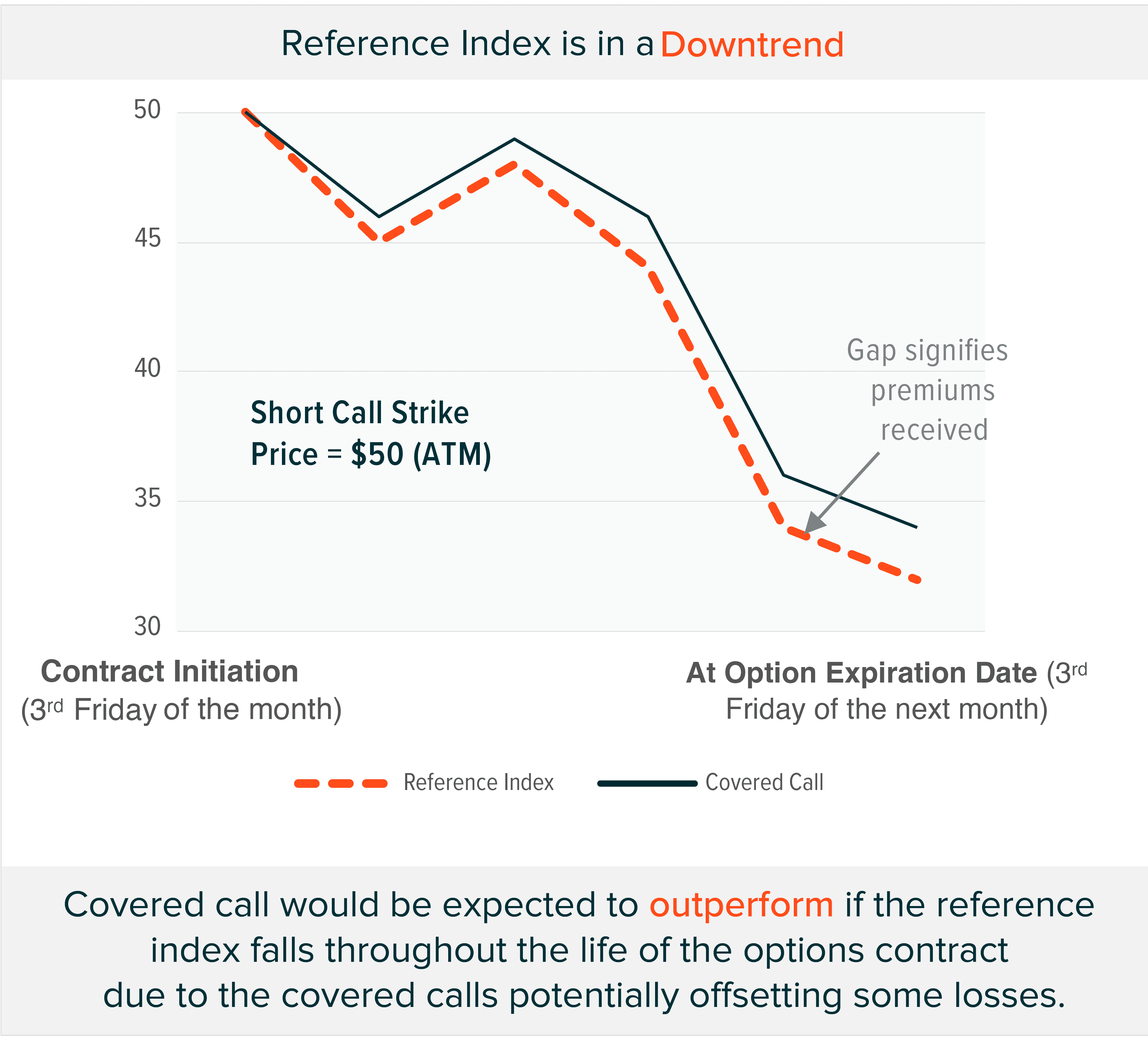

Notwithstanding reinvestment, the income component potentially provided by tracking BXNTU may suit the needs of various accounts, such as institutions like pension funds and endowments. That said, tracking an index that writes call options against 100% of its underlying portfolio can affect a fund’s performance in varying market scenarios. In theory, the premiums that BXNTU might receive position it to outperform the Nasdaq 100 most effectively when the index trades in choppy, flat, and declining directions.

Wealth generation can be pursued in many ways, beyond traditional allocations like the 60/40 equity and fixed income structure. A strategy like QYLD LN might offer a potential stream of current income and a diverse group of holdings on which to base its risk-adjusted returns. With a portfolio that seeks to follow the rules set forth by the Cboe Nasdaq 100 BuyWrite v2 UCITS Index and daily disclosure of portfolio holdings, QYLD LN also could allow awareness of the fund’s exposures. Trading the upside potential associated with its reference equity index to create premium income, QYLD LN may act as a functional portfolio diversifier and downside volatility mitigator on multiple levels.

Operating within the ETF sleeve, strategies like QYLD LN that track an index operating a covered call option strategy have the potential to reduce the beta coefficient associated with a basket of investments like the Nasdaq 100. Index funds might inherently provide this benefit because they typically take positions on a broad base of assets.

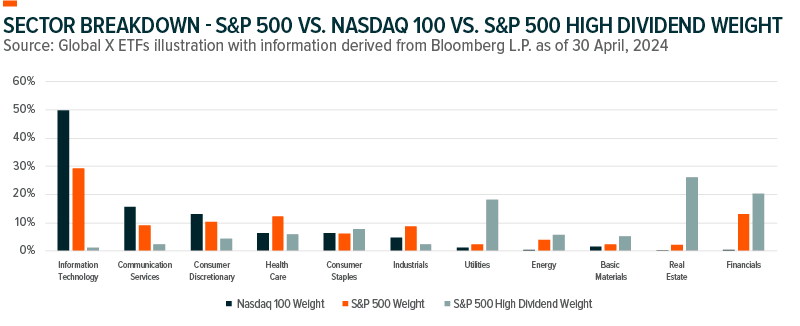

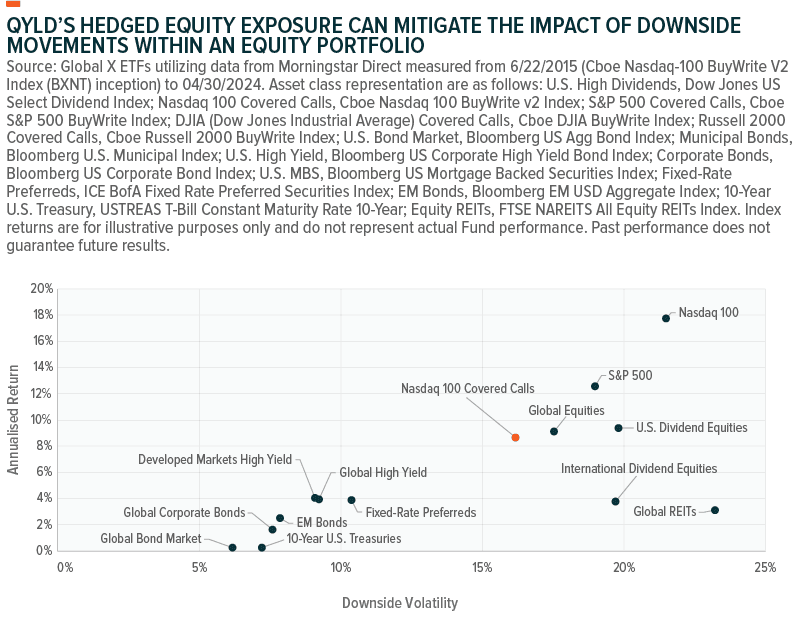

When it comes to conventional income accounts that have more of a tendency to seek out high dividend-paying stocks, as the illustration below shows, QYLD LN offers allocations toward sectors that they might have deemed unsuitable. By seeking to monetise the volatility associated with these sectors, QYLD LN’s potential aim to gain value by tracking an index that seeks to generate premium income creates an opportunity to pursue these underexposed positions. This provides a potential defensive posture when value-oriented equities are not trading on an upward trajectory.

Another key attribute associated with systematic covered call strategies tracked by funds like QYLD LN is their attempt to pursue a straightforward, rules-based nature. Passively managed products typically follow a strict set of rules that establish specific exposures over an explicit time frame. Relative to a strategy that employs active management without a daily holdings disclosure, this might allow for a better understanding of precisely where fund allocations are being made. The uniformity of a rules-based investment strategy could allow for seamless implementation into a broader portfolio, where risk-adjusted return metrics can be considered and weighed accordingly.

Because QYLD LN tracks an index that seeks a minimal level of capital appreciation in exchange for option premiums, the fund may offer a value proposition that can be utilised through various allocation combinations. For example, implementation of QYLD LN within a broader growth portfolio has the potential to help obtain a growth and income blend, depending on a potential risk and yield appetite. The ability to possibly be this nimble within an index tracking strategy that maintains a 100% coverage ratio with NDX call options could support the ability to modify a portfolio in a variety of different ways. Some examples of equity portfolio breakdowns that harness QYLD LN are illustrated below.

QYLD LN returns are represented by NAV returns. Beta is measured against the Nasdaq-100 Index.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent quarter- and month-end is available here.

Mixed economic signals, including those from inflation numbers, consumer confidence and elevated treasury yields, make speculating on future market movements particularly difficult. This year’s rapid run-up in value for the Nasdaq 100 and its subsequent slowing doesn’t make it any easier. In this environment, covered call options strategies could benefit portfolios, particularly when volatility ramps up and uncertainties linger. As a core competency of the passively managed ETFs that Global X provides, it is believed that QYLD LN’s systematic approach makes it a compelling diversification tool for a broad range of accounts.

Capital at risk: The value of an investment in ETFs may go down as well as up and past performance is not a reliable indicator of future performance.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Bloomberg L.P. (n.d.) [NDX price from January 1, 2024 to April 30, 2024.] Retrieved on May 10, 2024 from Global X Bloomberg terminal.

2. Bloomberg L.P. (n.d.) [NDX price from January 1, 2024 to April 30, 2024.] Retrieved on May 10, 2024 from Global X Bloomberg terminal.