Europe

Loading...

Past performance is not a guide to future returns.

Past performance is not a guide to future returns.

Silver appears to be setting up for its strongest run in decades. With the Federal Reserve (“Fed”) potentially poised for rate cuts, and 2024 possibly shaping up to be a year of fundamental deficits, the silver market looks set for a breakout.1 2Silver has surged to its highest level in over a decade, and gold is hitting record highs, largely driven by the momentum of expected interest rate reductions.3 4 However, some see broader forces such as, monetary policy shifts, geopolitical risks, and the US election shaping a turbulent economy where silver could shine as a store of value.5 On the fundamentals, booming demand from China’s solar and EV industries fuelled by the energy transition is adding to silver’s outlook according to the International Energy Agency.6

Silver physical demand surpassed supply in 2023, following a three-year pattern; the global market deficit was down by 30% year over year (yoy) from 2022's likely all-time high, but it was still one of the greatest at 184.3Moz.7

2023 saw silver's industrial demand continue to rise, achieving a record due to high solar demand.8 Sluggish supply played a role in the previous registered deficit as well.9 Due to the possibility of medium-term industrial demand growth and the lack of visible supply expansion, deficit circumstances may remain, with a fourth year of deficit seemingly on the horizon. The Silver Institute has already predicted a 17% supply-demand gap for this year, driven by rising industrial demand, a rebound in jewellery and silverware, and sluggish mine production and recycling.10

Furthermore, the solar panel industry could significantly increase industrial silver use to a record high this year.11

In 2023, silver industrial output reached another record at 654.4Moz, up 11% yoy; amid higher-than-expected Solar photovoltaic (PV) capacity increases.12 This year, global industrial usage is projected by the Silver Institute to grow by another 9%, driven again by green applications like solar panels.13

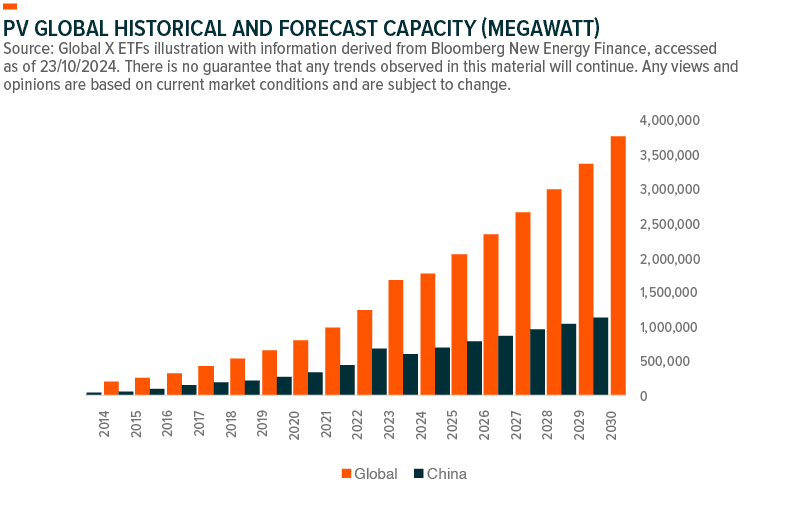

In recent months, China's silver demand has risen by over 20% yoy, powered by strong fundamental demand across solar, EVs and electronics.14 China’s silver industrial usage jumped 44% in 2023 alone and now accounts for 40% of global silver industrial demand.15 With over 80% of world’s solar panels produced in China, the outlook for silver potentially remains bright.16

Further, and according to BloombergNEF’s base case, globally, the capacity of installed solar PV is expected to increase 125% by 2030 from a 2023 base, with China accounting for most of this projected growth and domestically expected to potentially increase the installations by 66% over the same period.17 In northwestern Xinjiang, a Chinese state-owned business connected the world's largest solar facility to the grid, is set to generate 6.09 billion kilowatt hours of electricity annually.18 This milestone signals even greater demand for solar panels, potentially driving China’s silver imports higher as its renewable energy push accelerates.

Beyond China, despite high global silver prices which have traditionally discouraged Indian silver imports, India's silver imports surpassed the total combined for 2023 already in the first four months of this year.19

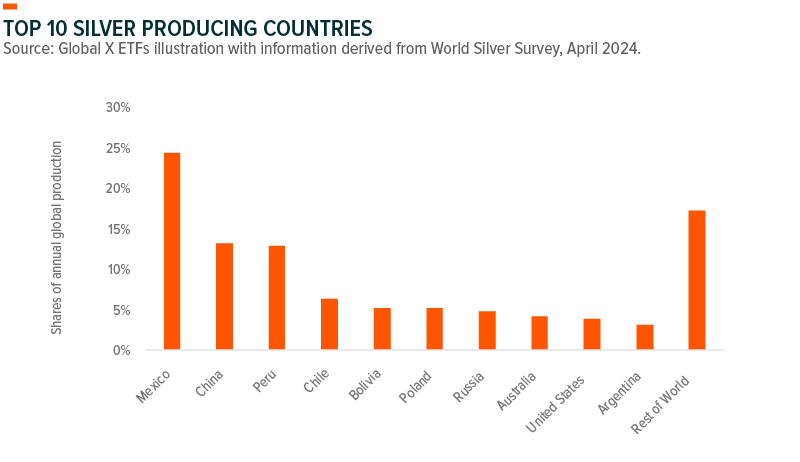

The global silver market is also deficit-ridden owing to sluggish supply of which major producers in Mexico appear to be primarily responsible: global mining production declined 1% year over year to 830.5Moz in 2023 as Mexico experienced its first 5% yoy reduction in output since 2020 due to strike actions.20

Looking forward, silver output from copper and zinc miners may continue to be hampered by socio-political stoppages and falling ore quality in 2024; still, it could rise in 2025 as miners recover from underinvestment and maintenance delays.21

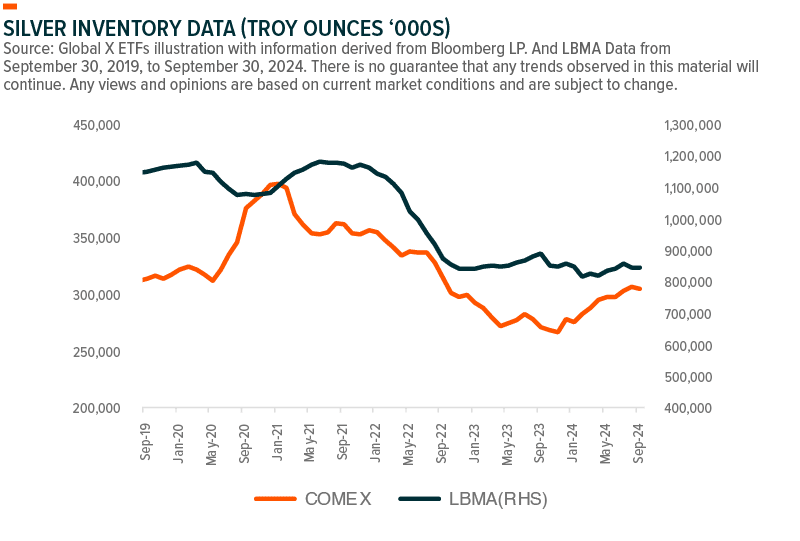

So far, high above-ground inventories have prevented a physical squeeze in the market.22 However, inventories are finite and might eventually further decrease, allowing the market to tighten further.

Though above-ground silver inventories may limit industrial-fuelled price upside in the short term, currently, macro drivers could support silver more than gold.

Given their status as precious metals, silver and gold are easily comparable. Two critical differences between the pair are firstly their respective market sizes, with silver being much smaller than gold, and secondly the industrial usage, which contributes to around 54% of silver’s annual demand while only around 7% of gold's.23 24 Despite these distinctions, silver is often called “second gold” as lower real yields, and a weaker US dollar might boost both precious metals.25

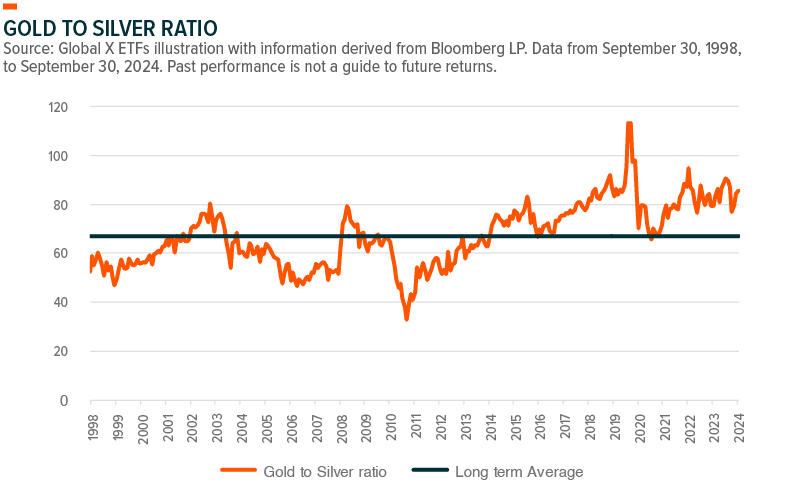

The gold-to-silver ratio, a metric which shows how much silver is needed to buy an ounce of gold, has averaged 67 in the last 30 years.26 With gold sitting at record highs and the ratio now above 80, silver may offer opportunities if it is cheaper than gold.27

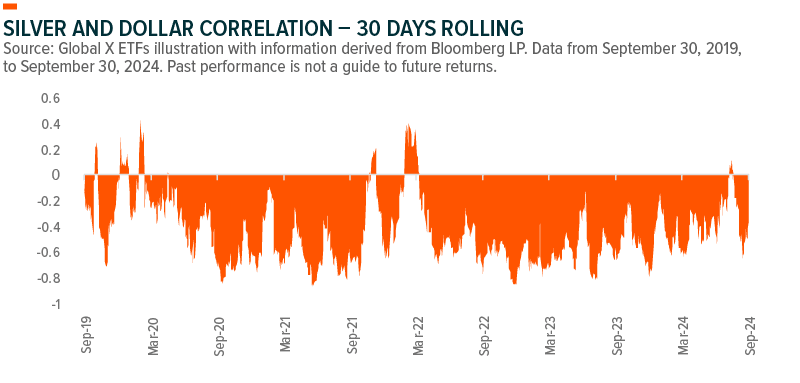

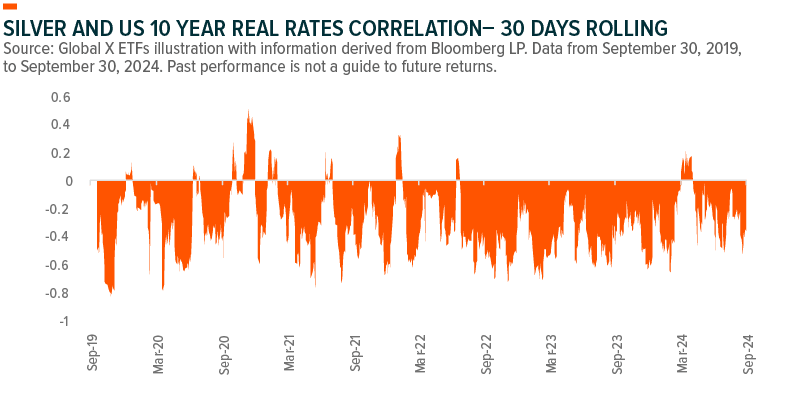

As an additional tailwind, the current macro-environment impacts silver as it is inversely related to the dollar and may serve as an inflation hedge and portfolio diversifier/safe haven for some investors.28 Among multiple central banks easing cycles, and especially among the Fed’s one, falling real rates could cut the opportunity cost of silver, potentially boosting its investment profitability.29 30

Dovish monetary policy, US election uncertainties, geopolitical threats, and market volatility may benefit ‘safe-haven’ assets like silver and gold. Fed Chair Jerome Powell's Jackson Hole address, in which he pledged rate cuts, was a turning point leading to a renewed dovish tone.31 In September, the US central bank cut rates more than expected for the first time in four years, lowering its benchmark lending rate objective by 0.5 percentage points to 4.75%-5%.32

Markets may be increasingly volatile while approaching and in the aftermath of the US elections in November 2024. However, both parties' policies may benefit precious metals. With markets continuing to worry about the national debt and deficit, this could well drive demand for ‘safe-haven' assets.33

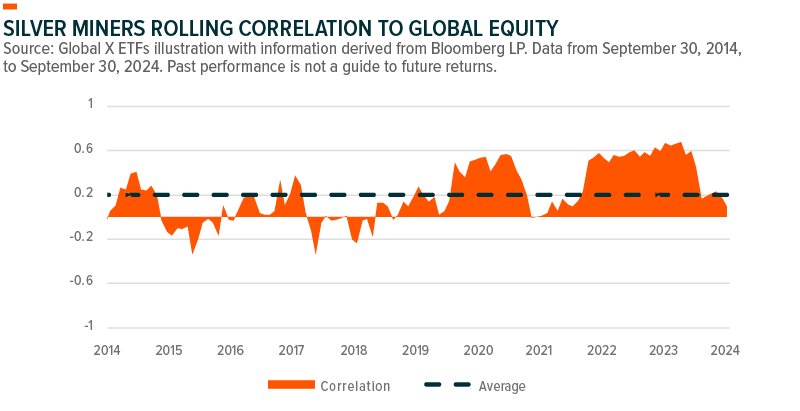

Precious metals' reputation as a potential safe-haven asset attracts investors during macroeconomic uncertainty, such as the present tumultuous markets. Moreover, silver is potentially a valuable portfolio diversifier due to its low long-term correlation with other risky assets.34

The dual nature of silver as both a precious and industrial metal makes it entirely unique. Since silver can appreciate during both periods of high economic growth (when industrial demand is expanding) and times of high volatility (when demand for precious metals is rising), we think that a direct or indirect exposure to it could be strategic holding in an investor’s portfolio. Particularly now, when dovish monetary policies, geopolitical threats, and US elections are creating a fractured economy, silver could shine as a potential store of value. At the same time, China’s strong solar silver demand could further exacerbate the fundamental deficit.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.