Sustainable Transition: The Opportunity in Hydrogen

Achieving net-zero emissions is among the most pressing and globally shared objectives of the 21st century. Hydrogen is key to these plans.

Our planet’s climate is changing for the worse. Two months ago, we published a report that touched on how temperatures are rising and why this presents an existential threat to billions around the world, including submerged coastlines, more natural disasters, lethal heatwaves, and crumbling economies.2020 tied 2016 for being the hottest year on record, and 2021 tied 2018 as the sixth warmest year on record.1,2 The root of these changes, however, is the same as ever.

Around 75% of warming comes from atmospheric carbon dioxide (CO2) and humans are responsible for increasing concentrations of such CO2 by 47% since the start of the industrial revolution.3,4 It is globally accepted that capping warming to 1.5°C above pre-industrial levels can limit climate risk – a path that is achievable if we reduce emissions by 45% from 2010 levels by 2030.5 Transitioning to renewable power production and electrifying areas of the economy that still depend on fossil fuels is core to this. But some sectors can’t be electrified and many industrial processes release emissions unrelated to energy. Hydrogen offers solutions to these gaps.

In the following piece, we explore the essential role hydrogen will likely play in striving for net-zero emissions and limiting climate change.

Key Takeaways

- Hydrogen can help decarbonise hard-to-electrify sectors like transportation, buildings, and industry

- More affordable and abundant renewable energy is driving down the cost of hydrogen production

- Hydrogen fuel cells can generate zero-carbon electricity that powers cars, heats buildings, & more

- Hydrogen can serve as a storage solution for variable renewable energy sources

SETTING THE STAGE: RENEWABLE POWER CAN ONLY GO SO FAR

The shift to clean power is well underway, but this alone is not enough. Renewables’ share of global electricity generation reached 29% in 2020, 2% more than in 2019 and almost 10% more than in 2010.6 Yet, electrical end-uses represent only a small share of total final energy consumption, just 17% in 2019, with transportation, buildings, and industrial processes accounting for the remainder.7 So despite renewables’ continued gain of share within the power sector, decarbonisation requires a transition to clean energy across all sectors.

Buildings, transportation, and industry still rely heavily on high-emitting fossil fuels. In 2020, renewables made up just 12.6% of primary energy consumption.8 Direct electrification of these sectors can meaningfully shift the energy consumption mix to renewable sources, but electrification is not always viable or possible. The remaining share of energy consumption must come from other zero-emission sources. This is where hydrogen comes in.

WHY HYDROGEN?

Hydrogen is the most abundant and lightest element in the universe. At standard conditions, hydrogen is a gas (H2) that has immense potential as an energy carrier, containing three times more energy content by weight than gasoline.9 On earth, it only naturally occurs bonded to other elements in molecules like water (H2O) and methane (CH4), and must be isolated as H2 for use on its own – which we refer to as hydrogen production.

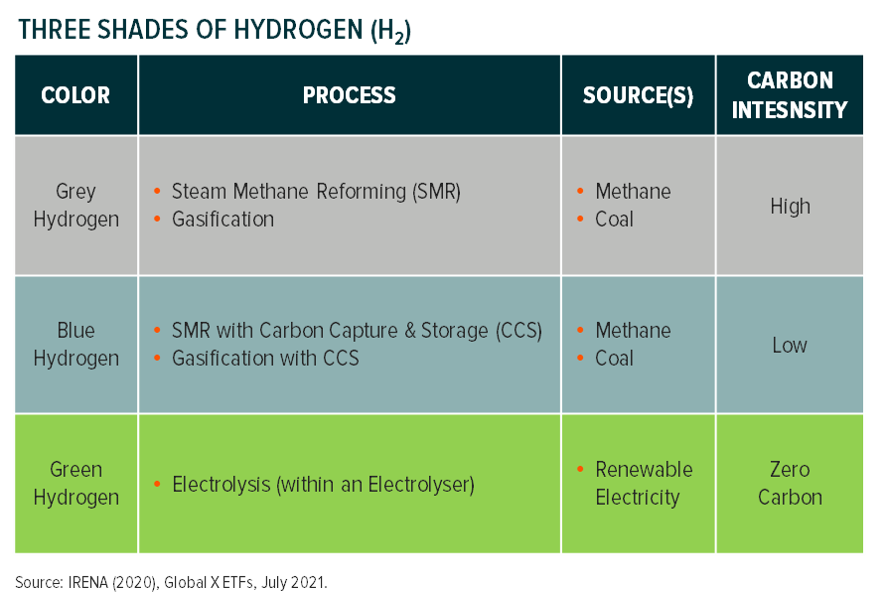

Despite its energy potential, hydrogen is primarily used today as an input for refining petroleum, treating metals, and producing fertiliser. Almost all of this hydrogen is produced using the fossil-fuel intensive methods of steam methane reforming or gasification (grey hydrogen).10 According to the International Energy Agency (IEA), hydrogen production uses 6% of global natural gas and 2% of global coal, resulting in over 830M tonnes of CO2 emission annually.11 Hydrogen production doesn’t have to be emission-intensive, however, and its potential as an energy carrier can actually contribute to decarbonisation. In-fact, low- to zero-carbon production could make hydrogen an US$11T market by 2050, increasing annual demand for H2 from today’s 70 megatonnes (Mt) to 613Mt in the 1.5°C warming scenario.12

Current production methods can use carbon capture, and storage (CCS) to reduce emissions, possibly by 85-95% in the future.13 Hydrogen produced in this way is called “blue hydrogen.” More importantly, though, another hydrogen production method called electrolysis has the potential to produce hydrogen without releasing any emissions. Water electrolysis is the process of splitting water into H2 and oxygen using an electric current. In practice, electrolysis occurs in a device called an electrolyser, which uses power from an external energy source to produce hydrogen, or electrolytic hydrogen.14 When this power comes from a clean energy source like wind or solar photovoltaic (PV), hydrogen production is a zero-emission process and the resulting hydrogen is called “green hydrogen.”

While all shades of H2 have energy potential that can be turned into electricity in fuel cells without releasing direct emissions, low-carbon production methods hold the key to the future hydrogen economy. Low-carbon hydrogen has the potential to bring clean energy to the above-mentioned sectors where electrification is not viable and reduce emissions in countless other ways. However, this can only become a reality once a meaningful transition to green hydrogen is well underway.

MAKING A HYDROGEN ECONOMY A REALITY

Electrolysis produces a small share of today’s hydrogen and not that much of it is green.15 Why? Producing green hydrogen is expensive. As of November 2021, green hydrogen costs US$3US$.64/kg to produce compared to between US$1.34 and US$2.4/kg for grey hydrogen and US$2.09/kg for blue hydrogen.16 Yet, these figures do not show how much progress the industry made over the past decade: in 2010 green hydrogen production cost US$10-15/kg, or roughly 23.4x more than it does today.17

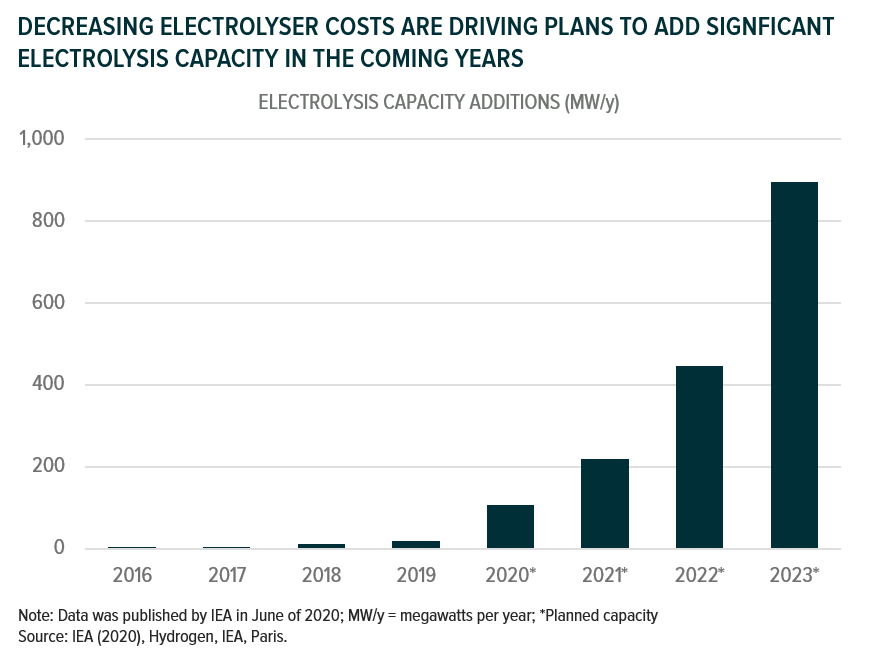

The cost and availability of renewable energy and the cost of electrolysers are historically the primary inhibitors to affordable green hydrogen production. But these hurdles are now disappearing. Renewable power is cheaper and more available than ever. Over the past decade, total generation capacity increased nearly 4x for wind and 17.5x for solar PV, while the levelised cost of electricity decreased as much as 80%.18,19 This trend appears to be continuing, with the Hydrogen Council reporting in February 2021 that ongoing reductions in the costs of renewables are “as much as 15% lower than previously expected.”20 Decreasing electrolyser costs are similarly driving cheaper production. The capital cost of electrolysis dropped by 60% from 2010 to 2020, and in 2021, the Hydrogen Council reported that their new forecast for the 2030 cost of an electrolyser is 30-50% lower than what they projected in 2020.21,22

These developments could bring green hydrogen to paradigm-shifting cost parity with grey hydrogen within the next 7-13 years in several regions, especially if carbon emissions are taxed.23 While this is an optimistic view, it is not unrealistic. Hydrogen took center stage at the recent COP26 Conference, which resulted in an agreement between nearly 200 nations that builds on the Paris Agreement in key areas.24 This agreement, known as the Glasgow Pact, reaffirms goals set by the Paris Agreement and acknowledges that the world’s climate change efforts must accelerate over the next decade to avoid the worst outcomes. Additionally, the Glasgow Pact acknowledges the central role fossil fuels play in climate change and calls for the phasedown of coal usage.

COP26 yielded several other impactful agreements between smaller groups of attendees. Such agreements include:

- The U.S. and China unexpectedly agreed to boost cooperation on renewable energy generation, developing regulations, and deploying clean technologies.25

- About 450 banks, pension managers, and other firms committed to align 100% of their funds with net-zero emissions targets by 2050. Together these firms command US$130T in assets, enough to address a large portion of necessary clean technology investments.26

- About 100 countries agreed to cut methane emissions 30% by 2030.27 Methane contains ~80x more warming potential than carbon dioxide, so curtailing this gas could have the most immediate impact of any of the deals struck at COP26.28

Among the commitments endorsed during COP26 was a ‘hydrogen breakthrough’ goal which aims to ensure affordable low-carbon hydrogen is globally available by 2030.29 In addition, a number of countries reaffirmed their commitment to using hydrogen, including the United Arab Emirates, Japan and Germany.30

We expect green hydrogen production costs to continue to decrease, setting the stage for the viable use of green hydrogen.31

USING HYDROGEN TO POWER FUEL CELLS & DECARBONISATION EFFORTS

Indirect electrification refers to using electricity as an input into industrial processes, rather than as an immediate replacement for fossil fuels.32 In the context of clean energy, indirect electrification occurs when electrolysis produces hydrogen. Fuel cells can put this indirect electricity to use, generating an electric current by inducing an electrochemical (redox) reaction between H2 and oxygen that produces only heat and water as biproducts. Assuming hydrogen becomes cost-competitive with fossil fuels, hydrogen fuel cells offer significant promise for achieving net-zero emissions in the transportation and buildings sectors.

Fuel cell electric vehicles (FCEVs) rely on zero-emission electric motors for propulsion, similar to battery electric vehicles (BEVs). Different than BEVs, FCEV motors are powered by fuel cells that use hydrogen, stored as H2 in on-board storage tanks, and oxygen from the air as fuel to generate a steady stream of electricity. FCEVs share many of the same advantages over internal combustion engine (ICE) vehicles as BEVs including less maintenance, zero emissions, and quieter drives. But they also have many of their own advantages. FCEVs store electricity indirectly as hydrogen and have no need for the heavy lithium-ion batteries that BEVs use to store electricity. As a result, they are significantly lighter, can offer greater range, operate in all temperatures, and take minimal time to refuel.33 To the downside, FCEVs are less energy efficient than BEVs, indirectly losing energy as heat via electrolysis-based hydrogen production and directly losing energy as heat when fuel cells generate electricity.

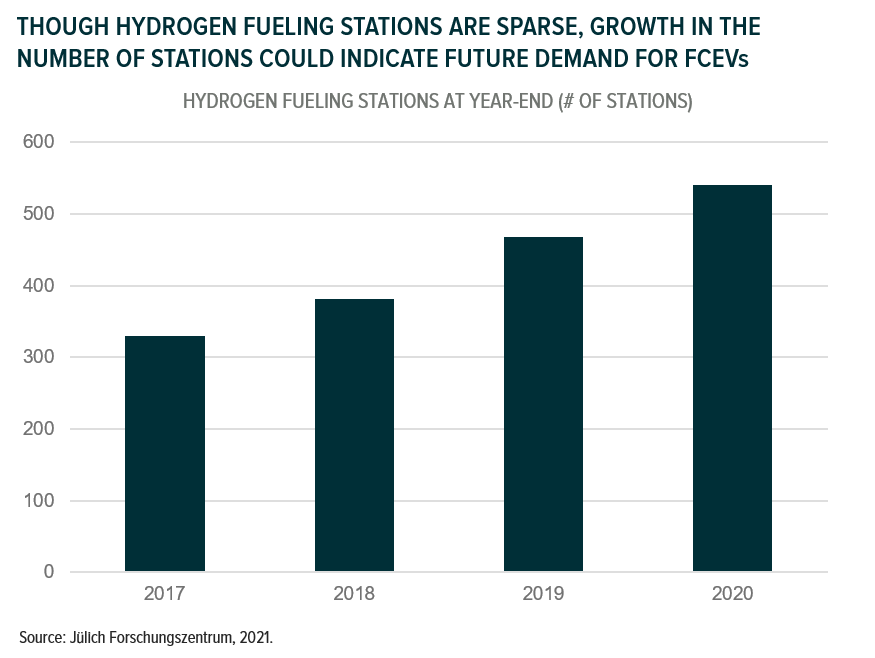

FCEVs are still early stage and potential consumers have a limited number of FCEV options available to them. Fueling a FCEV presents an additional challenge as there are just under 550 hydrogen fueling station located around the world.34 Encouragingly, fueling deployments are on the rise and almost 160 new fueling locations are under construction or in the planning phase (excluding the U.S).35 We expect this expansion to accelerate further as green hydrogen production ramps up and FCEV adoption becomes an explicit component of global decarbonisation plans. It is important to note that traditional EVs are still an essential part of general electrification and there are no plans to replace them with FCEVs. As noted, each has their own strengths and weaknesses. We believe BEVs are the best option to replace ICE passenger cars, which do not require significant range and for which consistent use between charges could compensate for battery drain. FCEVs, on the other hand, are better options to replace ICE trucks, cross-country buses, and other medium- to heavy-duty long-distance vehicles. FCEVs offer considerably more range than BEVs and are much lighter, an important characteristic for vehicles that are already transporting heavy cargo and are often subject to weight-based restrictions and fees.

Hydrogen also has the potential to help decarbonise buildings, which for the most part use natural gas or oil for heat and power. Electrification in the buildings sector lags that of other sectors, mainly because there are limited cost competitive alternatives to natural gas. Hydrogen fuel cells for combined heat and power technology (FC CHP), however, could serve as a viable low-carbon alternative as soon as 2030, according to the Hydrogen Council.36 FC CHP generates electricity for power in the same way a fuel cell in an FCEV does, but also uses by-product heat from the fuel cell to heat water and for space heating. Considering that the buildings account for 33% of global energy demand and 25% of global emissions, we anticipate that FC CHP and other hydrogen-based energy options will play a major role in this segment’s decarbonisation efforts.37

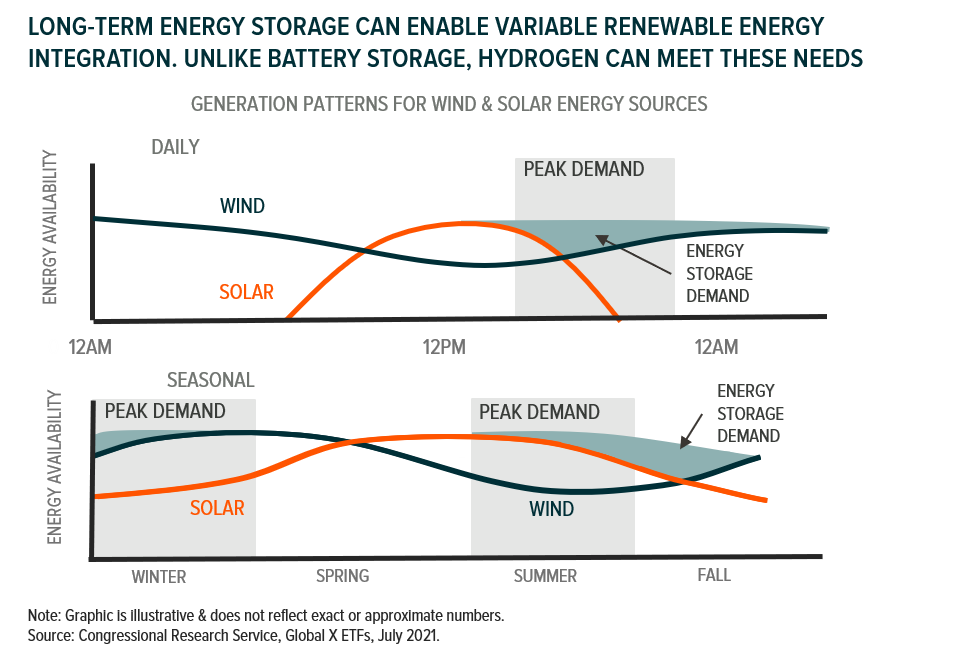

ENABLING VARIABLE RENEWABLE ENERGY WITH GREEN HYDROGEN

More available and affordable renewable energy production is a key enabler of green hydrogen, as discussed, but this dynamic goes both ways. Energy storage is fundamental to the widespread integration of variable renewable energy (VRE) sources like wind and solar PV for which environmental factors directly affect electricity generation. A VRE source can generate more or less electricity than demand, depending on if the wind is blowing or the sun is shining.38 Integrating multiple types of VRE can fill in daily and seasonal generation gaps, but efficiently storing renewable energy offers greater flexibility and allows for creative use of surplus electricity.

Green hydrogen presents particularly advantageous storage characteristics as it can store energy to accommodate for seasonal fluctuations in generation, unlike grid-scale lithium-ion batteries which gradually lose their charge to battery drain.39 Though energy is lost as heat during electrolysis, H2 maintains its energy potential as long as it is stored correctly. This unique characteristic offers benefits beyond just providing on-demand energy; it can help stabilise electricity prices, which improves cost recovery and enables further capacity additions.40 At the same time, these synergies could drive further economies of scale for green hydrogen as renewable energy producers invest in electrolysers to increase H2 storage capacity.

INVESTING IN HYDROGEN

Hydrogen is the most abundant element in the universe and hydrogen-based compounds are a part of our daily, if not hourly, lives. Yet, it is only recently that hydrogen entered the forefront of policymaking, project development, and investment. We believe hydrogen represents the next generation of clean technologies, offering a path to decarbonisation beyond just the power sector. While hydrogen is still in its early innings, we believe investing in hydrogen and other clean technologies will benefit from tailwinds in sustainable innovation that are reshaping our world.

This document is not intended to be, or does not constitute, investment research