Sustainably-Themed Investing: Affecting Positive Change Through Disruption

Against the backdrop of a global pandemic that impacted most facets of society in an unprecedented fashion, two investment areas shone through in 2020: thematic investing and sustainable investing. Thematic investing refers to the process of identifying disruptive macro-level trends and the underlying investments that stand to benefit from the materialisation of those trends. Sustainable investing is an investment approach that considers environmental, social, and governance (ESG) factors, alongside financial ones, in the pursuit of competitive returns and positive impact for people and planet. At the end of 2020, aggregate U.S.-listed Thematic ETF AUM stood at US$104.1 billion, representing a growth of 274% and close to quadruple the number from a year prior (US$27.8 billion at the end of 2019). At the same time, on a global scale ESG-oriented ETFs reached a tipping point in 2020 with AUM growing 223% over the year to a record US$189 billion.1

While at first glance these two areas may seem independent from each other, thematic investing and sustainable investing are not only far from mutually exclusive, but potentially synergistic and complementary to each other in certain circumstances. Both investment philosophies inherently focus on a long-time horizon. Looking at investor demographics, both thematic investing and sustainable investing notably appeal to younger investors: 83% of millennials said they were “extremely interested” or “very interested” in thematic investing according to a Global X-commissioned 2017 survey, while 86% of millennials expressed interest in sustainable investing, according to a Morgan Stanley survey in the same year.2 As millennials enter their peak earning years and inherit trillions of dollars, we believe investment assets in both thematic and sustainable areas, especially those that sit at the intersection of thematic and sustainable investing (or “sustainably-themed investing”), will continue to rise meaningfully.

In the following sections, we will discuss why it may make sense to consider sustainably-themed investments, and then dive into a few specific examples.

Sustainably-themed Investing: Aligning Impact with Growth

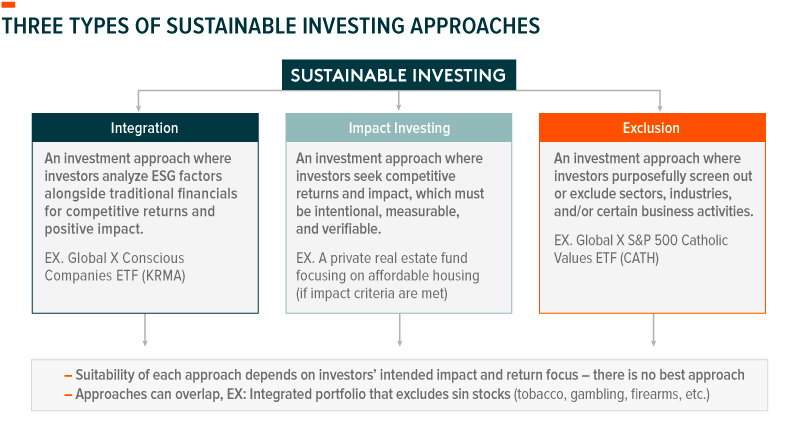

Broadly speaking, there are three categories of sustainable investing approaches: Integration, Impact Investing, and Exclusionary.

Typically, ESG-oriented ETFs track indices that employ integration and/or ESG-related exclusions in the security selection process. ESG data is a critical input to this process, informing company-level composite ESG scores (for an integration approach) and business involvement metrics (for an exclusionary approach). If exclusions are part of an index methodology, index providers use business involvement metrics, usually expressed as revenue percentages, to narrow investment universes down to only companies with an acceptable level of involvement in certain activities, like manufacturing or distributing weapons or alcohol, for example. In ESG integration approaches, company-level ESG scores or ratings are used alongside traditional considerations to identify and weight index constituents.

For public market investors, an ESG integration approach could be the best way to affect changes while providing broad market exposure. As we previously discussed in “How Sustainable Investing Can Create Long-Term Value,” as capital increasingly flows to responsible companies, other investors could view the resulting momentum as a positive sign and invest accordingly themselves. Ideally, companies recognise the source of positive investor sentiment and maintain their standards, while less responsible companies are motivated to improve theirs. Data has shown that companies with high ESG scores, on average, experienced lower costs of capital compared to companies with poor ESG scores.3

A limitation of ESG integration and exclusionary approaches is the difficulty for investors to articulate or gauge the direct sustainable outcome of their invested dollars. This is largely due to two reasons. First, the complex and dynamic nature of ESG data makes it hard to know if one is investing in best-in-class companies in terms of sustainability. There are many ESG data providers and sometimes scoring methodologies and resulting outputs contrast. Second, the characteristics of public equity markets afford investors little opportunity to directly trace, monitor, and measure the impact of their investments. This stands in contrast to the private markets, where investors have more visibility into where their funds are being directed.

Compared with ESG integration, impact investing draws a clearer line between one’s investment dollars and achieving a specific outcome. Industry definitions of impact investing limit much of a public equity investor’s opportunity set, given the requirements on measurability of impact and “additionality”, the latter of which means “only allocating to businesses that they would not otherwise choose to invest in if they were not seeking to achieve a positive social impact.”4

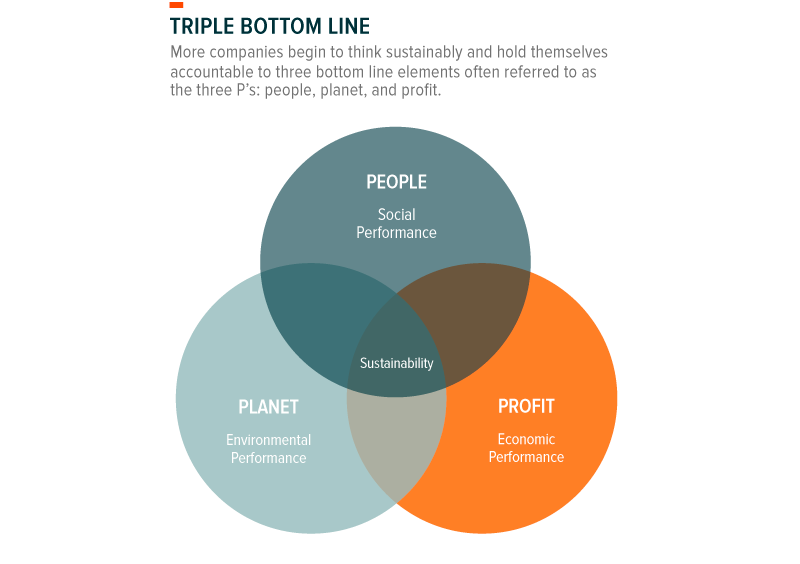

In our opinion, one way to potentially facilitate positive environmental and social changes without sacrificing financial returns, is to approach sustainable investing through a thematic lens. Following a sustainably-oriented theme means targeting innovative and disruptive industries that could lead to tangible improvements in certain environmental and/or social matters. As relevant industries grow and representative businesses scale, they may not only affect more positive changes for people and planet, but also reward their investors with financial profits (see the “Triple Bottom Line” framework as shown in chart below).

It is not by chance that we are witnessing numerous disruptive themes emerge at the intersection of thematic and sustainability. When examining the key stakeholders in the adoption of thematic investing – consumers, businesses, governments – all three are prioritising goals that could propel sustainable themes forward. These goals include ambitious climate neutrality targets, better health outcomes, improving quality of life around the world, and increased productivity in the labour force, just to name a few.

In the next few sections, we will discuss how certain disruptive themes contribute to sustainability goals, while providing investors with notable potential for economic profit.

For Planet: CleanTech and Renewable Energy

Clean Technology, or “CleanTech,” describes myriad disruptive technologies that mitigate or inhibit negative environmental impacts. The business activities under this theme could involve renewable energy production, energy storage, smart grid implementation, residential/commercial energy efficiency, and/or the production and provision of pollution-reducing products and solutions.

Since the inking of the Paris Agreement in 2016 to fight climate change on a global scale, many signatories have upped the ante, vowing to take more aggressive measures in the pursuit of carbon neutrality. The European Green Deal, for example, is a set of policy initiatives by the European Commission with the overarching goal of making Europe the first climate-neutral continent by 2050. In North America, the Government of Canada submitted draft legislation in November 2020 to Parliament, titled “The Canadian Net-Zero Emissions Accountability Act”, adding Canada to the list of over 120 countries pledging to reach net-zero emissions by 2050.5

The further development and adoption of CleanTech will be essential to achieving carbon-neutrality goals and limiting emissions to acceptable levels. It will also require significant investment. A scenario presented by the International Renewable Energy Agency (IRENA) estimates that US$110 trillion of cumulative global investments between 2016 and 2050 would keep the world on the right track, with about 80% of that going to clean technologies.

In the Canadian government’s Pan-Canadian Framework on Clean Growth and Climate Change (the “PCF”), which is the government’s master plan for climate action, clean technology is listed as an important pillar. After establishing the PCF, the government announced in 2017 a budget of US$21.9 billion over 11 years for green infrastructure which will include “targeted investments to support greenhouse gas reductions and enable greater climate change adaptation and increased resilience.”6

Turning our attention to the U.S., the new climate-conscious Biden Administration and a supportive Democrat-controlled Congress will likely accelerate climate action, directing capital to CleanTech. President Biden’s climate action pledge includes an ambitious US$2 trillion plan that would accelerate a clean-energy transition, cut carbon emissions from the electricity sector by 2035, and achieve net-zero emissions by 2050.7

Closely related to CleanTech, renewable energy production is also a theme of critical importance for environmentally- conscious investors. Despite being inherently related, these two themes are complementary to each other in that they primarily cover different parts along the climate / “green” value chain. CleanTech encompasses up-chain activities such as manufacturing of photovoltaic (PV) components, inverters, wind turbines/blades, grid components, and stationary storage/batteries. Further down the green value chain, renewable energy producers primarily engage in energy generation from renewable sources such as wind, solar, hydroelectric, geothermal, and biofuels. It is worth keeping in mind that beyond renewable energy, part of the CleanTech theme is related to pollution reducing practices like carbon capture, use, and storage (CCUS) and carbon dioxide removal (CDR) which could be useful for achieving carbon neutrality.

For Planet: Electric Vehicles, Lithium & Battery Technology

Traditional internal combustion engine (ICE) vehicles leave a significant environmental footprint, emitting carbon dioxide (CO2), carbon monoxide (CO), and other toxins as they turn fossil fuels into energy through combustion. This is particularly troubling as street-level tailpipes release emissions into the air that we breathe, making auto emissions a more immediate health threat than those of industrial smokestacks. Equally troubling, auto-related greenhouse gases like CO2 accumulate in the atmosphere, contributing to global warming.

One obvious benefit of electric vehicles (EVs) over ICE vehicles is the absence of carbon emissions, particularly when they are recharged from renewable energy sources. Additionally, the electric motors that power EVs are about as 3x efficient as traditional ICE engines. Energy efficiency measures how much output is attained by consuming the same amount of input energy – the higher, the better. Electric engines are 90% efficient as compared to internal combustion engines which are 20-40% efficient.8

Most of today’s EVs use lithium-ion batteries due to their high energy per unit mass, high power-to-weight ratio, high energy efficiency, high-temperature performance, and low self-discharge.9 Next-gen battery technologies such as solid-state could require twice as much lithium as traditional technologies, while providing greater mileage between charges and extending battery lifespans.10 As we noted in our piece “Can Lithium Keep Up With the EV Boom”, in the face of the rapid projected rise of global EV demand – estimated compound annual growth rate (CAGR) of 29% in EV sales between 2019 and 2030, a lithium supply crunch could be looming. That said, several automakers, including Tesla, VW, and Daimler, are all reportedly exploring options for direct access to the lithium market in the hopes of vertically integrating their supply chains. We believe EVs and lithium are inherently intertwined themes that a sustainably-minded investor should keep a close eye on as they grow in lockstep.

For People: Health & Wellness and Longevity

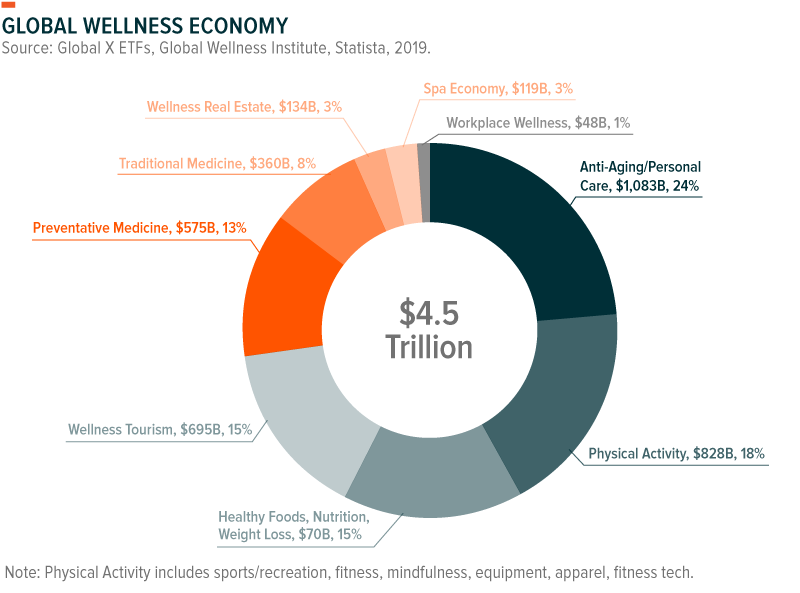

Physical health and the well-being of populations is a foundational component of social sustainability. The Health & Wellness theme goes beyond traditional healthcare; rather than treating symptoms or diseases as they are diagnosed, a health and wellness mindset is one that seeks to improve one’s quality of life by optimising physical and mental health. Health and wellness-related activities include exercise, leading an active lifestyle, nutrition, relaxation, preventative health, anti-aging products, and workplace wellness programs. In our view, companies that provide related products and services stand to benefit from the continued increase of global consumer spend directed to the “global wellness economy,” which was worth US$4.5 trillion based on the latest available data.11

Taking a similar approach to social sustainability, the Longevity theme tracks companies that cater to the health needs of a growing global senior population. These include companies involved in age-related pharmaceuticals, senior living facilities, and other sectors that contribute to increasing lifespans and health spans.

People are living longer and populations are getting older. Based on current projections, the world will have nearly 1 billion individuals aged 65+ by 2030 and over 1.5 billion by 2050.12 Despite lifespans extending, noncommunicable and age-related diseases present burdensome and avoidable economic and social costs. Other broad socioeconomic trends have implications for older populations as well. Economies are becoming more globalised, urbanisation is increasing population density, and technology is evolving rapidly. Demographic and family changes mean there will likely be fewer caretakers for larger elderly populations – people have fewer children than ever, are less likely to be married, and are less likely to live with older generations. To mitigate this imbalance, society will need better information and tools to ensure the well-being of older citizens. In our view, companies that can effectively address different challenges arising from longevity, such as those involved in treating illnesses or providing senior housing, are positioned to reap the economic rewards through their business activities.

For People: Education

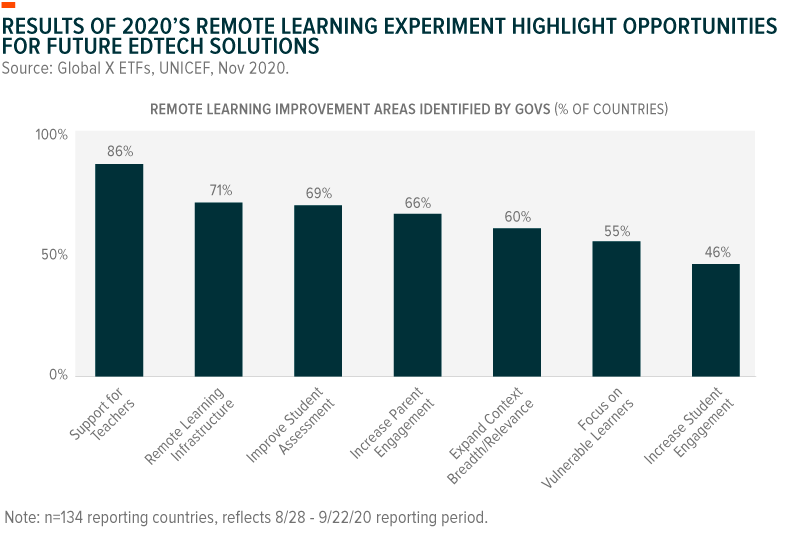

In our view, the Education theme underpins social sustainability in both developing and developed economies. “Quality Education” is listed as Goal #4 of the United Nations Sustainable Development Goals (SDGs), which are a collection of 17 interlinked global goals designed to be a “blueprint to achieve a better and more sustainable future for all.”13 The UN initiative is geared toward ensuring inclusive and equitable quality education, while promoting lifelong learning opportunities for all. To this end, education technology, or “EdTech,” can remove logistical obstacles to education, like geography and personal schedule, as well as potentially lower education’s cost barriers. The COVID-19 pandemic served as a real-world test for these technologies, revealing potential areas of improvement and future industry opportunities.

Even in the most developed countries, there is more to be done to enhance people’s educational experience, especially in the realm of tertiary education, which includes traditional higher education as well as vocational and professional learning. On average, in Organisation for Economic Co-operation and Development (OECD) member countries, around 18% of individuals aged 15-24 participated in vocational training in 2017.14 And many of those who enrol in such training see success: the OECD notes that “countries with well-established [vocational] programs have been more effective in holding the line on youth unemployment.”15 We expect to see growth in this segment as younger demographics strive to hone their abilities for entrance into the labour market and older ones seek to modernise and maintain their skillsets in a world where automation technologies make the labour market more competitive.

Lastly, educational accessibility means more than just logistical and budgetary flexibility; it’s also about making positive educational outcomes more likely. Artificial Intelligence (AI), for example, can leverage machine learning to understand students’ individual needs and design and adapt curriculums to meet them. Implementing AI could augment learning by ensuring that students strengthen their weakest areas. It also optimises teaching by reducing teachers’ upfront workloads, saving time for them that they could allocate elsewhere. We already see mass-implementation of such technology in China and are starting to see early-stage implementation in the U.S. By 2025, global AI-EdTech expenditure is projected to reach US$6B.16

Conclusion

Thematic investing and sustainable investing approaches are each important in their own right and top-of-mind for today’s increasingly ESG-minded investment community. In our view, sustainably-themed investing is a way for investors to recognise the benefits of both approaches, leveraging key concepts drawn from each. Importantly, looking at companies through a thematic lens could allow investors to grow their investments, while delivering tangible positive change on the environment and/or society. In particular, we believe several well-defined themes such as CleanTech, Renewable Energy Production, Electric Vehicles, Lithium & Battery Technology, Health & Wellness, Longevity, and Education, can all serve investors well in their quest to achieve multiple objectives (financial and otherwise) simultaneously.

This document is not intended to be, or does not constitute, investment research