The Case for a Defined-Outcome Strategy

Equity markets within the U.S. have staged a decent recovery to date in 2023. However, with inflation still tracking at relatively high levels, and interest rate policies shifting around the globe, concerns about navigating a lower return environment remain evident. Investors are adjusting their equity portfolios accordingly, seeking out more defensive positions as the calendar turns toward the final stanza of the year. By accessing the options market via the implementation of a defined-outcome strategy, the opportunity to obtain a specified level of downside protection for their portfolios could be available.

Key Takeaways

- In this challenging macroeconomic environment, defined-outcome strategies may provide reduced equity risk while maintaining a level of upside participation.

- In a rising rate environment, defined-outcome strategies could help minimize equity volatility while avoiding fixed income duration risk.

- Defined-outcome strategies could be beneficial in terms of seeking a specified level of downside protection by maintaining long exposure to the equity markets while offering option packages that come at a cost as close as possible to neutral.

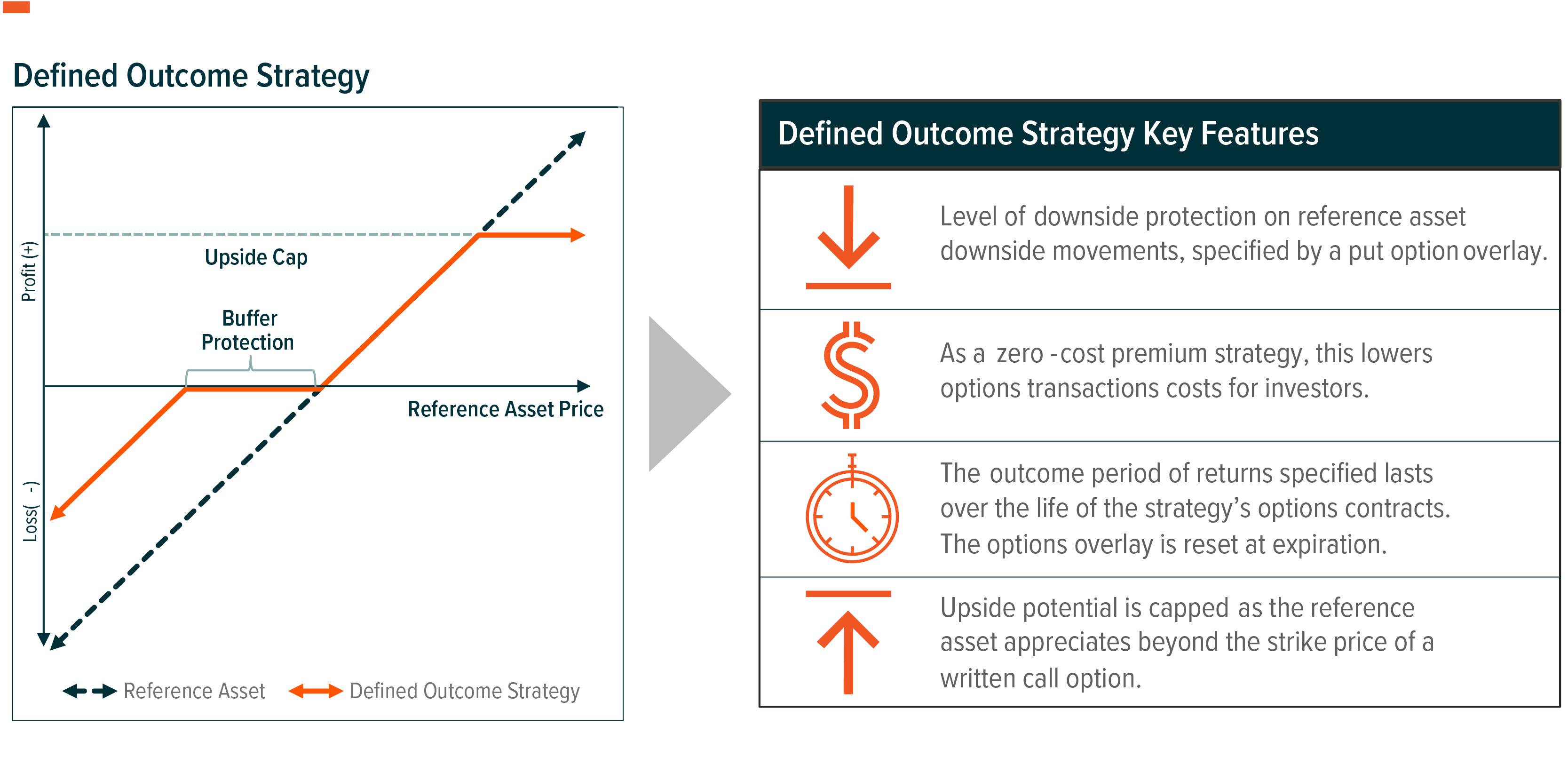

What Are Defined-Outcome Strategies?

Certain defined-outcome strategies, utilizing a combination of put options and call options on a specified reference asset, could provide an explicit level of downside protection with equity upside participation, up to a cap. The key purpose of this type of option overlay is to provide a level of risk mitigation that is predictable and specified, should this type of strategy be held from the initiation of the option contracts to contract expiration.

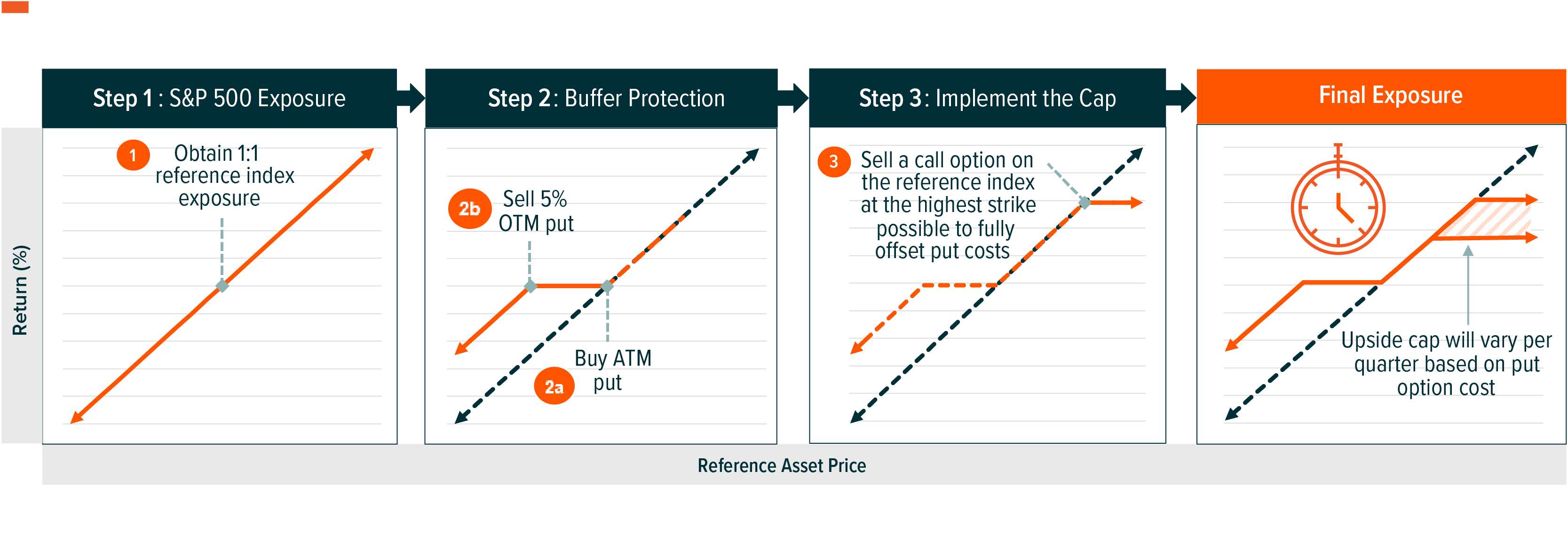

A defined-outcome strategy consists of the following positions that encompass the overarching exposure:

Step 1) Obtain 1:1 exposure to an underlying equity asset or index.

Step 2) The strategy will simultaneously buy a put option and sell a put option on this same underlying asset. This combination of buying a put and selling a put is known as a bear put spread where the strike price of the long put is higher than that of the short put position. The difference between the strike prices determines the degree to which the buffer protection is offered relative to the underlying asset.

Step 3) Lastly, the strategy will sell a call option at a strike price such that it offsets the costs of the bear put spread detailed in Step 2. This short call option position helps create the zero-cost put spread collar.

Defined-outcome strategies can be implemented using options with differing time expirations such as quarterly or annually. Since the premium cost of the bear put spreads will change over time, this will likely result in a different call strike price and therefore a different upside cap during each outcome period. Ultimately, the combination results in a final payoff structure that will likely allow the strategy to achieve full upside potential, up to a cap, with the ability to provide a specified level of protection on losses. Hence, these multiple legs help create the defined outcome characteristics of a strategy like this.

Expectations of a Defined-Outcome Strategy

Given the specified level of downside protection offered from a defined-outcome strategy, implementing it could result in a “defined-outcome” of returns from the underlying asset should this strategy be held from contract initiation until contract expiration.

Quarterly Reset Defined Outcome Strategy

For example, the Cboe S&P 500 15% WHT Quarterly 5% Buffer Protect Index, a representation of a quarterly defined-outcome strategy, has a 5% buffer that resets each calendar quarter. The index does this by implementing a hypothetical portfolio containing a put spread featuring a long “at-the-money” put option position paired with a short 5% “out-of-the-money” put option. This means that, in down markets, losses may only occur over a quarterly period if the losses of the S&P 500 exceed 5%. In an uptrend, all of the price appreciation associated with the S&P 500 upside up to a specified cap is dependent on the strike price of the covered call for the outcome period.

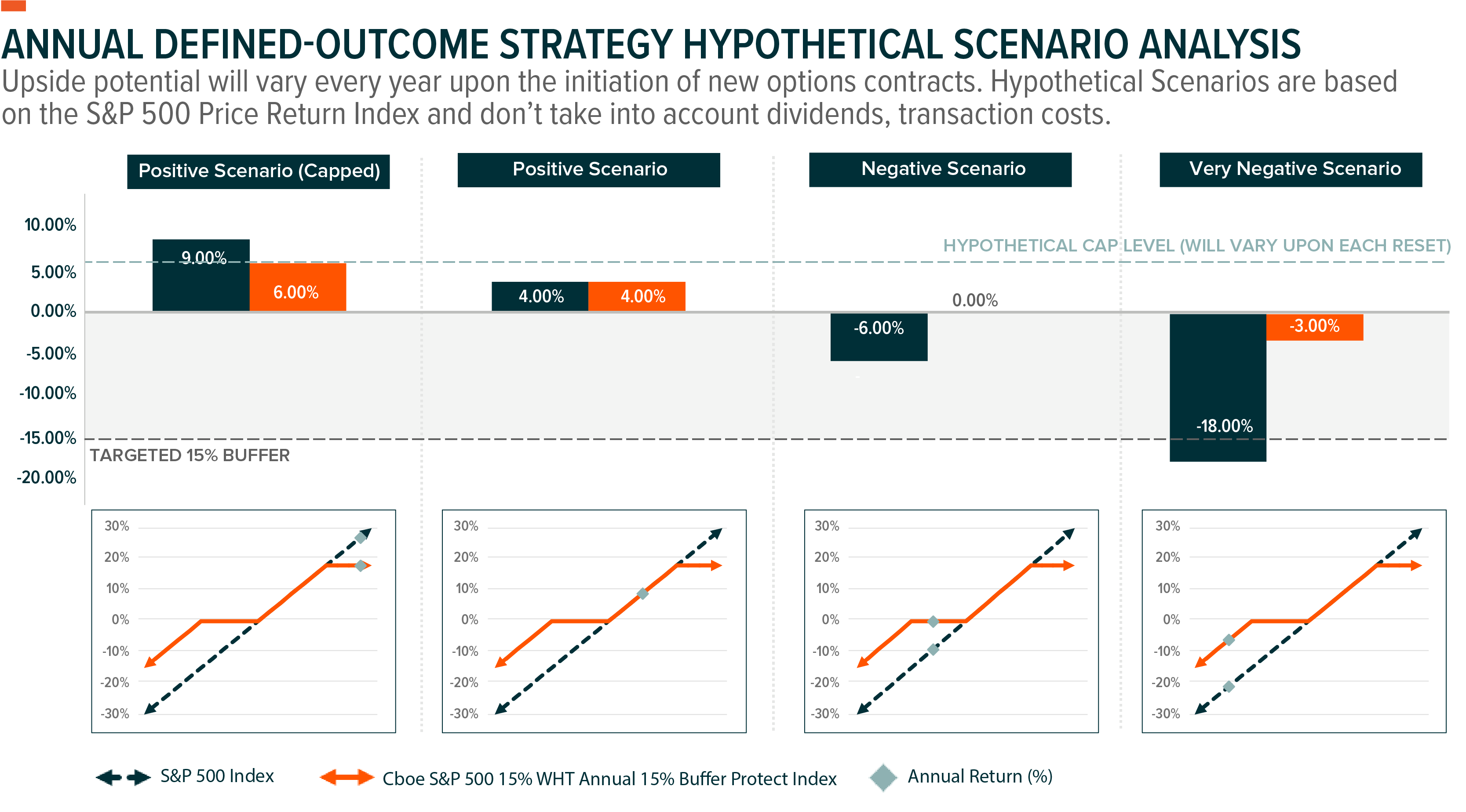

Annual Reset Defined Outcome Strategy

Another implementation approach to a defined outcome strategy is to utilize the same aforementioned options overlay, but with options that have a 1-year time length until expiration. By implementing a defined outcome strategy over a longer timeframe, with a wider strike price between the long put option and short put option positions, an annual defined outcome strategy can potentially offer a higher level of downside protection. Using the Cboe S&P 500 15% WHT Annual 15% Buffer Protect Index as a representation of an annual defined outcome strategy, the index is designed to provide a 15% buffer on the S&P 500 index that is reset each calendar year.

One difference relative to a quarterly buffer strategy is that an annual reset potentially offers a higher level of downside protection because its options are rolled less frequently. However, the upside potential is lessened due to the longer wait for an upside cap reset. Therefore, having stronger convictions for bearish, equity market sentiment over the course of a 1-year period, but still looking to maintain a level of U.S. equity exposure, may lead to the determination that an annual defined-outcome strategy is more palatable. On the other hand, the quarterly defined outcome strategy may be more suitable in terms of seeking to lower the U.S. equity beta in a portfolio.

Why Should Investors Consider Defined-Outcome Strategies?

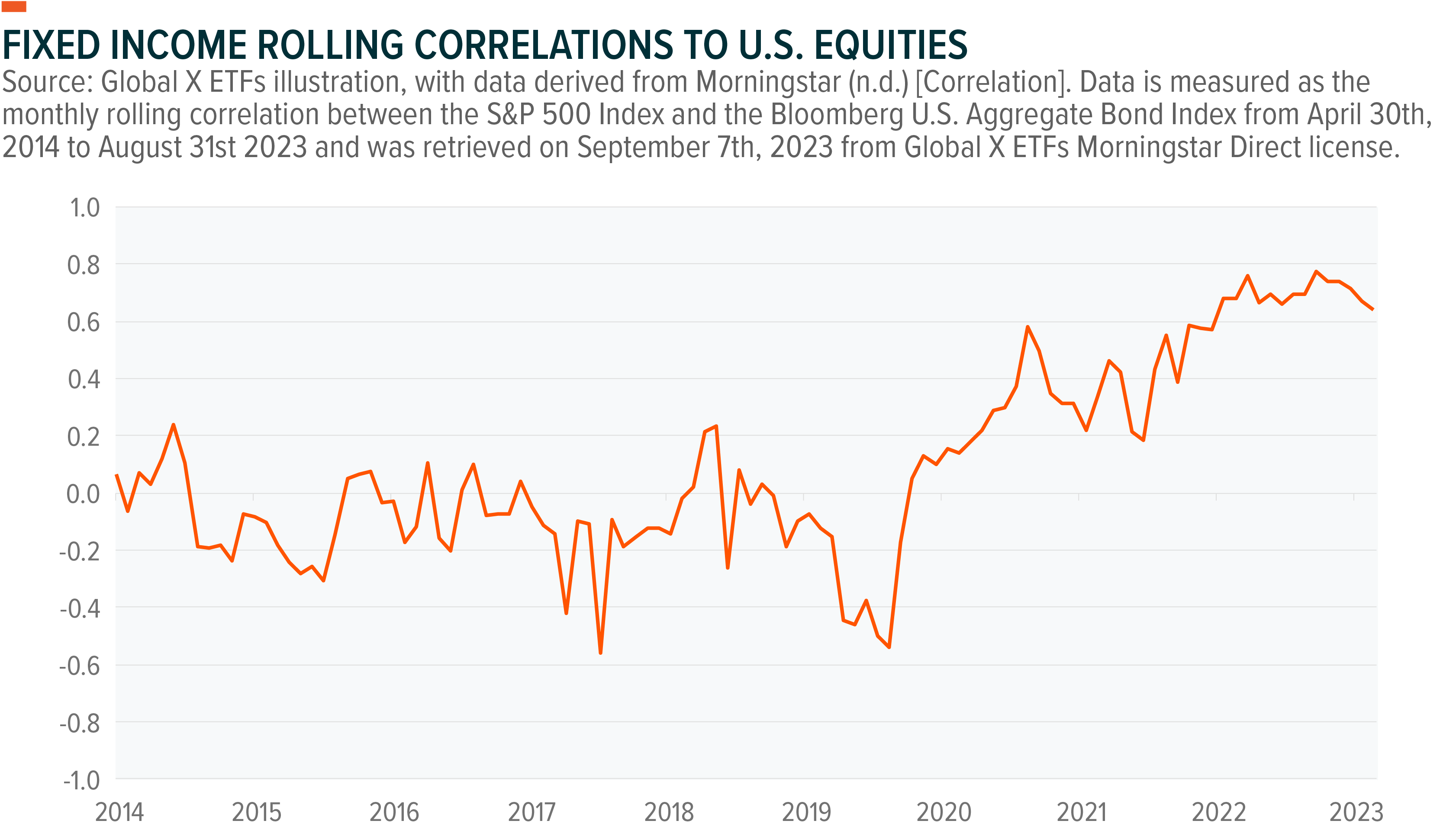

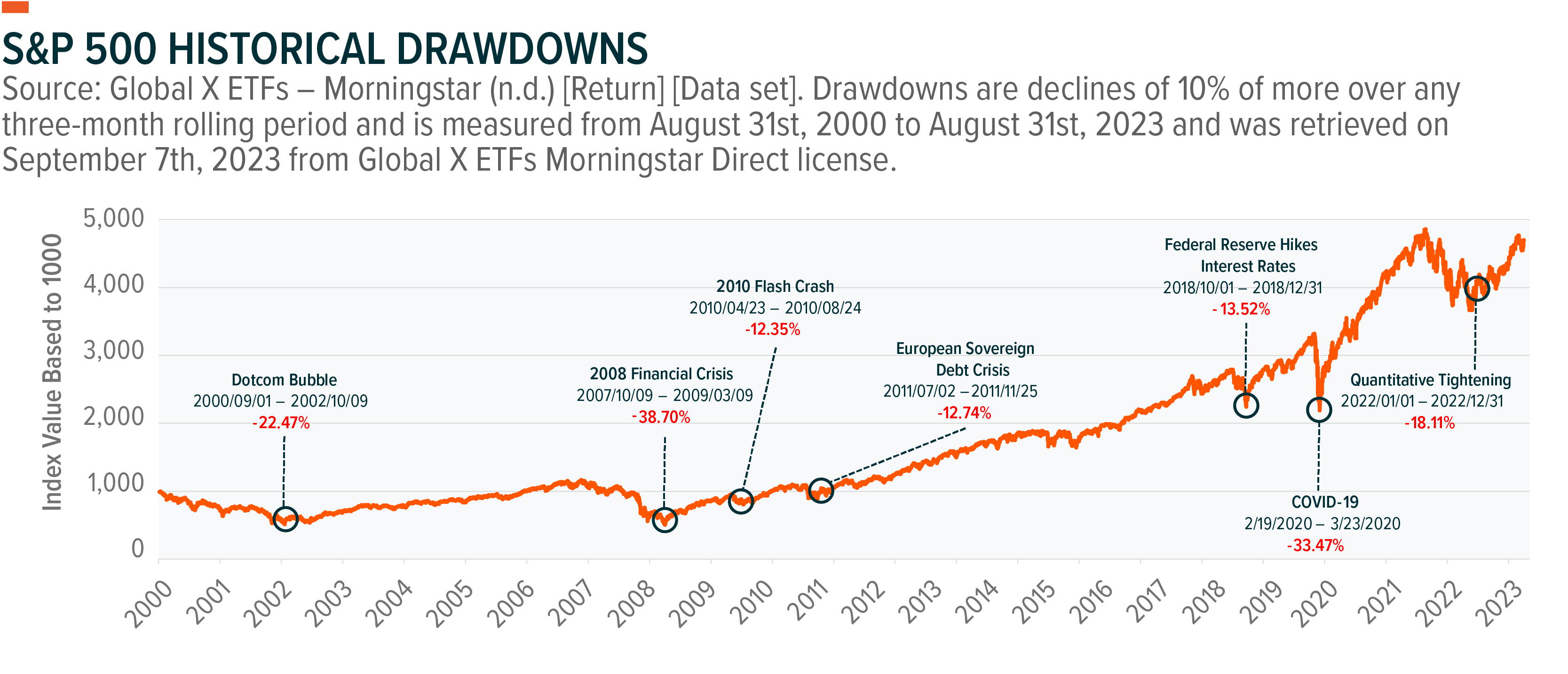

After a period of low interest rates and strong equity performance for most of the past decade, the recent inflationary environment led central banks around the globe to increase interest rates at an enhanced pace. This activity has slowed in the late stages of 2023. However, companies that benefitted from the previous low interest rate environment are still under pressure. The bond market has been adversely affected as well, with noteworthy weakness for the typical 60/40 portfolio and a side-effect of rising correlations between equity and fixed income markets. With the potential for higher volatility, it may make sense to explore a defined-outcome strategy for additional sources of portfolio diversification beyond typical asset classes.

As the COVID-19 pandemic showed, the risk of an unknown event or a market correction could always be looming on the horizon. Expecting potential capitulation within equity markets, limiting left tail risk may be a priority as opposed to maximizing gains. A defined-outcome strategy can potentially allow an investor to achieve multiple objectives. If equity markets were to fall, a defined-outcome strategy would be expected to provide its specified level of downside protection. However, if markets were to rise, participation in the potential upside of the underlying asset is still possible.

Defined-Outcome Strategies Can Potentially Help Alleviate Portfolio Volatility

Investors have typically sought different types of strategies to lower their portfolio’s volatility and mitigate substantial downside movements on particular assets. One common example of this is by purchasing a protective put. These types of option strategies simply purchase a long position on an underlying asset paired with a long put option on the same asset for a level of downside protection. The difference between a protective put and a zero-cost put spread collar, such as a defined-outcome strategy, is that a protective put strategy is expected to have a net premium cost while a defined-outcome strategy is expected to use a covered call to offset premium costs. Therefore, the trade-off is that a protective put may offer higher potential upside, but a defined-outcome strategy may offer a higher level of equity risk reduction related to the underlying asset.

Employing a low volatility factor strategy could be useful in terms of mitigating broader volatility. These types of portfolios tend to be constructed by filtering through a larger index universe to create a roster of low volatility equities over a specific period. Implementing a defined-outcome strategy on a broad index such as the S&P 500 may serve as another option to offset sector risks of low volatility factor strategies to achieve a more explicit level of volatility reduction. Furthermore, a defined-outcome strategy can potentially serve as a complement to the traditional 60/40 equity/fixed income split to improve diversification through the options market.

Conclusion

While markets tend to rise over the long term, there are opportunities for investors to endure a less volatile experience. Using a defined-outcome strategy within a portfolio could provide a way to mitigate potential downside risks while also participating in rising markets. With an explicit level of downside protection over the life of the options overlay, defined-outcome strategies have historically been utilized by investors to minimize equity volatility while avoiding the duration risks of fixed income securities to stay invested in equities for longer.

This document is not intended to be, or does not constitute, investment research