Europe

Loading...

Much to the surprise of global investors, the U.S. economy in 2023 has consistently exceeded expectations, proving to be more resilient than experts had forecasted in 2022. Reports showing strong economic data, despite an aggressive rate hike campaign last year prompted the U.S. Federal Reserve (the “Fed”) to make a noteworthy announcement at its latest meeting; the need to keep its policy rate elevated for an extended period.

Influenced by a combination of robust economic data and more persistent inflation than initially anticipated, the Federal Funds Rate (“Fed Funds”) rose to its highest level in over 20 years, a move mirrored closely by short-term treasuries. With the front-end of the treasury curve boasting rates above 5.5%, and recent inflation data revealing slowing inflation in the U.S., the current interest rate environment may pose an enticing entry-point for global investors.

U.S. Treasuries have historically borne a reputation as safe-haven assets during times of market volatility. Duration risk is particularly low for 1–3 month Treasury Bills (“T-Bills”), while the current yield curve inversion has elevated potential returns in this most liquid portion of the curve. The cash-like properties of T-Bills, coupled with their hedging properties may be appealing for any investor seeking a combination of safety, liquidity, and yield.

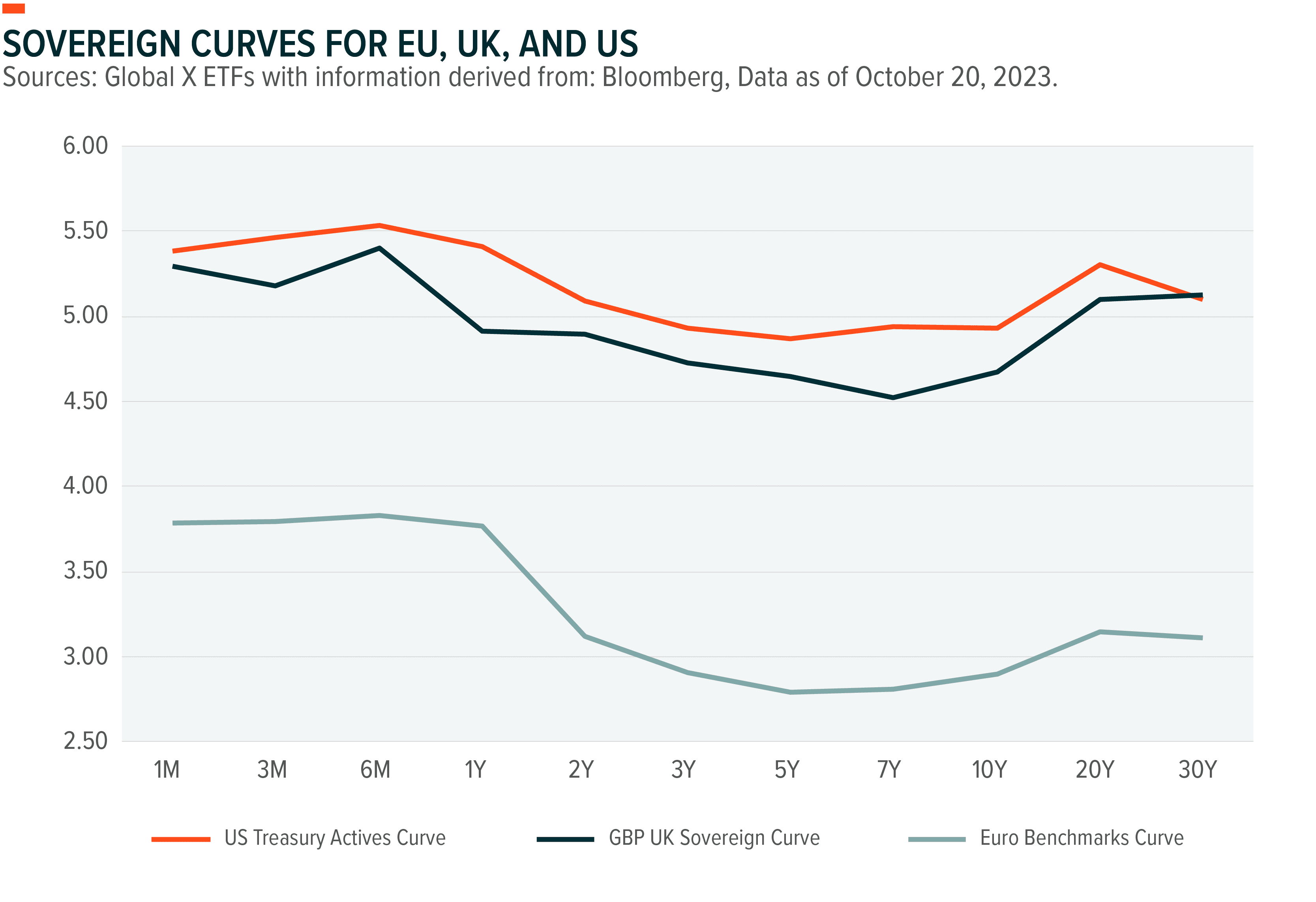

The U.S. economy continues to flourish in 2023 with real GDP growth on track to potentially reach 5.4% for the year, according to the Federal Reserve Bank of Atlanta.1 In contrast, the U.K. and the Eurozone have slowed, with Germany, the largest economy in the EU, on track for its second recession this year. This diverging growth paints substantially different pictures in the relative value of global sovereign debt, particularly as the Fed positions for one more possible rate hike in 2023.

The U.S. Consumer Price Index (“CPI”), a measure of the average change over time of prices paid by U.S. consumers, has trended steadily downward in recent months, showing 3.7%, year-over-year in September of 2023, down from a high of 9.1% in June of 2022.2 Simultaneously, the Fed’s goal to keep rates higher for longer has pushed nominal yields to their highest levels in 15 years. This combination of declining inflation and rising nominal rates has sent real yields higher.

Meanwhile, economic activity in the United Kingdom (“UK”) and Eurozone tells a different story. Recently, both the European Central Bank and the Bank of England signalled pauses to their rate hikes in response to declining inflation measures and slowing economic activity. Consumer prices across the European Union (“EU”) rose by 4.3% in September of 2023, down from 5.2% the previous month, its slowest pace in two years.3 At the same, the U.K. saw inflation come in at 6.7%, unchanged from the previous month.4

On a relative basis, U.S. debt offers the highest real rates of any developed market economy in the world; this metric backs out inflation from the nominal interest rate. While this dynamic will likely continue to evolve as monetary policy around the world adapts to changing economic conditions, the combined strength of the U.S. economy and the overall high yields on its debt, provide a compelling relative value argument for U.S. Treasuries.

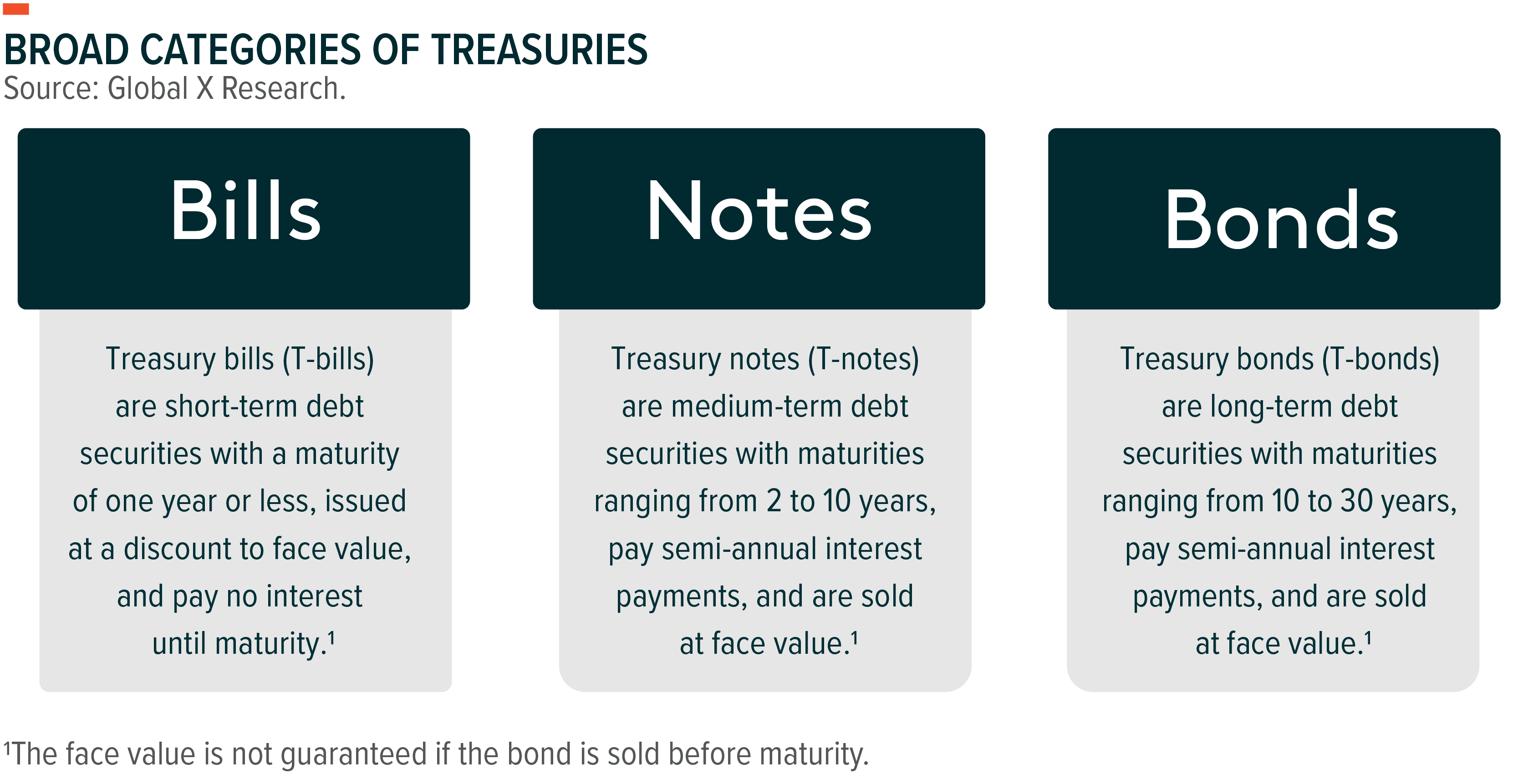

Treasury securities (“Treasuries”) are direct obligations of the United States Federal Government (U.S.), issued in maturities of 10-30 years (“T-bonds”), 2-10 years (“T-notes”), and 1 year or less (“T-bills”). T-Notes and T-Bonds pay interest semi-annually, while T-Bills are issued at a discount and mature at par without intermediary coupon payments. Regardless of their maturity, all treasuries are traded and pay interest in greenbacks (USD).

Treasuries carry one of the lowest credit risks among developed sovereigns, thanks to their underlying government guarantee, the dollar’s reserve currency status, and the exceptional credit ratings of the United States. However, treasuries do carry varying levels of interest rate (“duration”) and reinvestment risk.

CLIP LN addresses interest rate risk by investing in the shortest 1–3-month segment of the Treasury curve, thereby minimising time to maturity. Interest rate risk centres around duration, which measures how quickly cashflows are returned to investors. Short duration bonds expedite the return of principal and allow for prompt reinvestment of the maturing principal. This ability to consistently reinvest in newer and potentially higher-yielding issues helps blunt the index’s exposure to rising rates, which could make it an attractive solution for mitigating interest rate volatility during periods of uncertainty.

The Treasury curve shows diverging performance between short and long bonds over the past year, reflecting a yield curve inversion, when short term rates yield higher than long-term rates. While short-term rates are anchored to Fed policy, long-term rates are volatile and can be influenced by several factors, including inflation expectations, long-term growth expectations, and supply and demand dynamics.

As a proxy for short-term rates, the 1-3 Months US T-Bill Index is highly correlated with the Federal Funds Rate (“Fed Funds”). This correlation means that T-Bills react quickly to shifts in Fed policy. Ultra-short duration treasury indexes closely follow these rate movements by holding 1–3-month T-Bills, thereby mitigating their exposure to interest rate risk.

T-Bills inside of 1-year currently yield close to the Fed’s upper bound target rate of 5.50%, its highest rate since the Great Recession. Meanwhile, 10-year U.S. treasury bonds yield around 5.00%, spreading -50 basis points to Fed Funds. These high yields on the short end of the treasury curve could provide investors with an enticing opportunity to take advantage of higher yields, at minimal credit and duration risk.

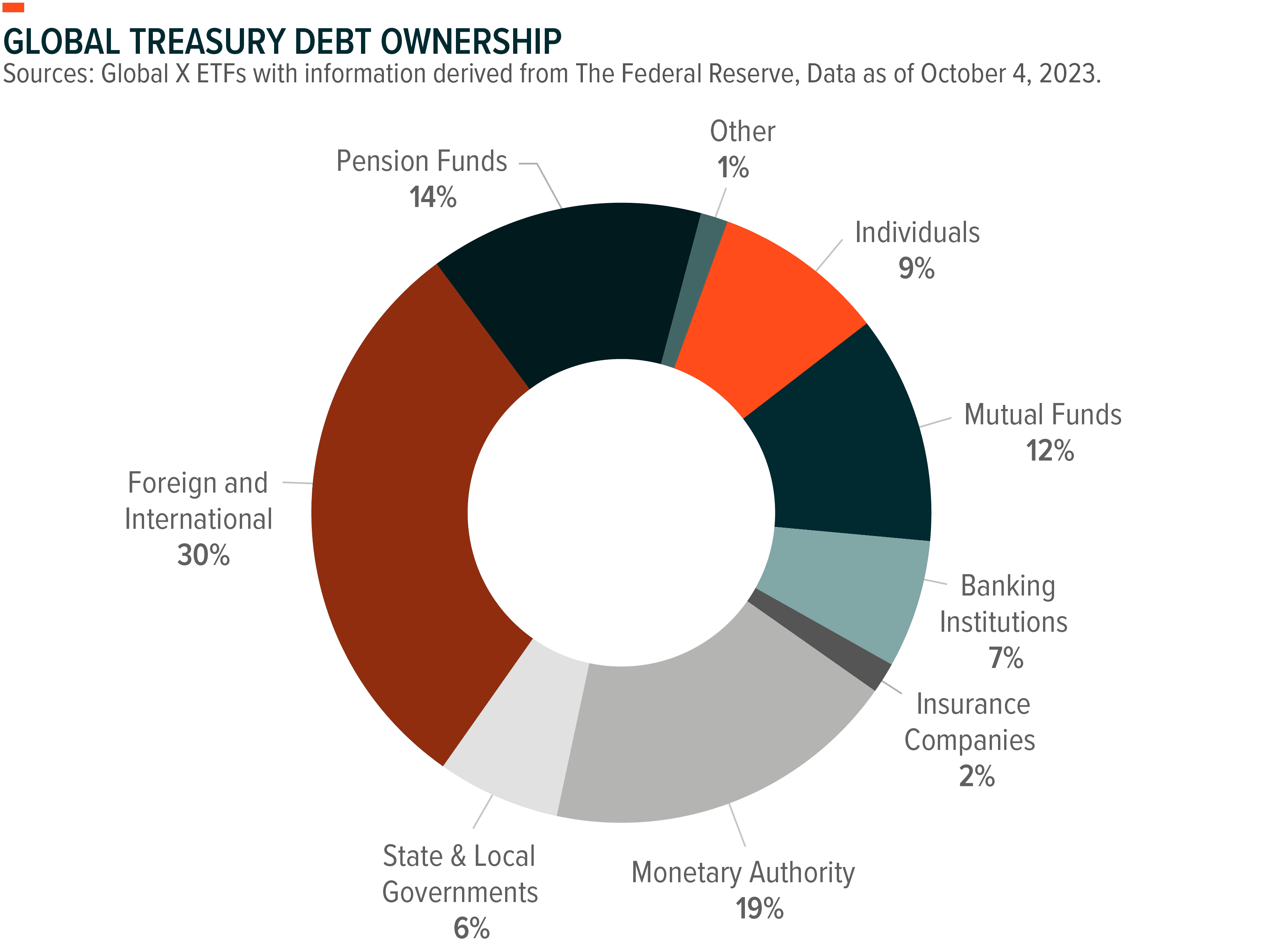

Short-duration T-Bills trade in the most liquid portion of the Treasury curve. Their strong liquidity and credit backing makes them popular tools for hedging, trading, and currency management activities among institutional investors and foreign central banks. To illustrate their scale, over $13 trillion of T-Bills have been issued to date in 2023, versus $2.5 trillion across all other treasury maturities.5

Investor flows have also shown an increasing preference for highly liquid short-term Treasuries, illustrating growing demand for stable high-yield investments. Year-to-date, net flows to U.S. focused ultra-short duration bond ETFs rose by over $3.9 billion across Western Europe and the U.K, while in the United States, total net flows for these funds accumulated to over $37 billion over that same period.6

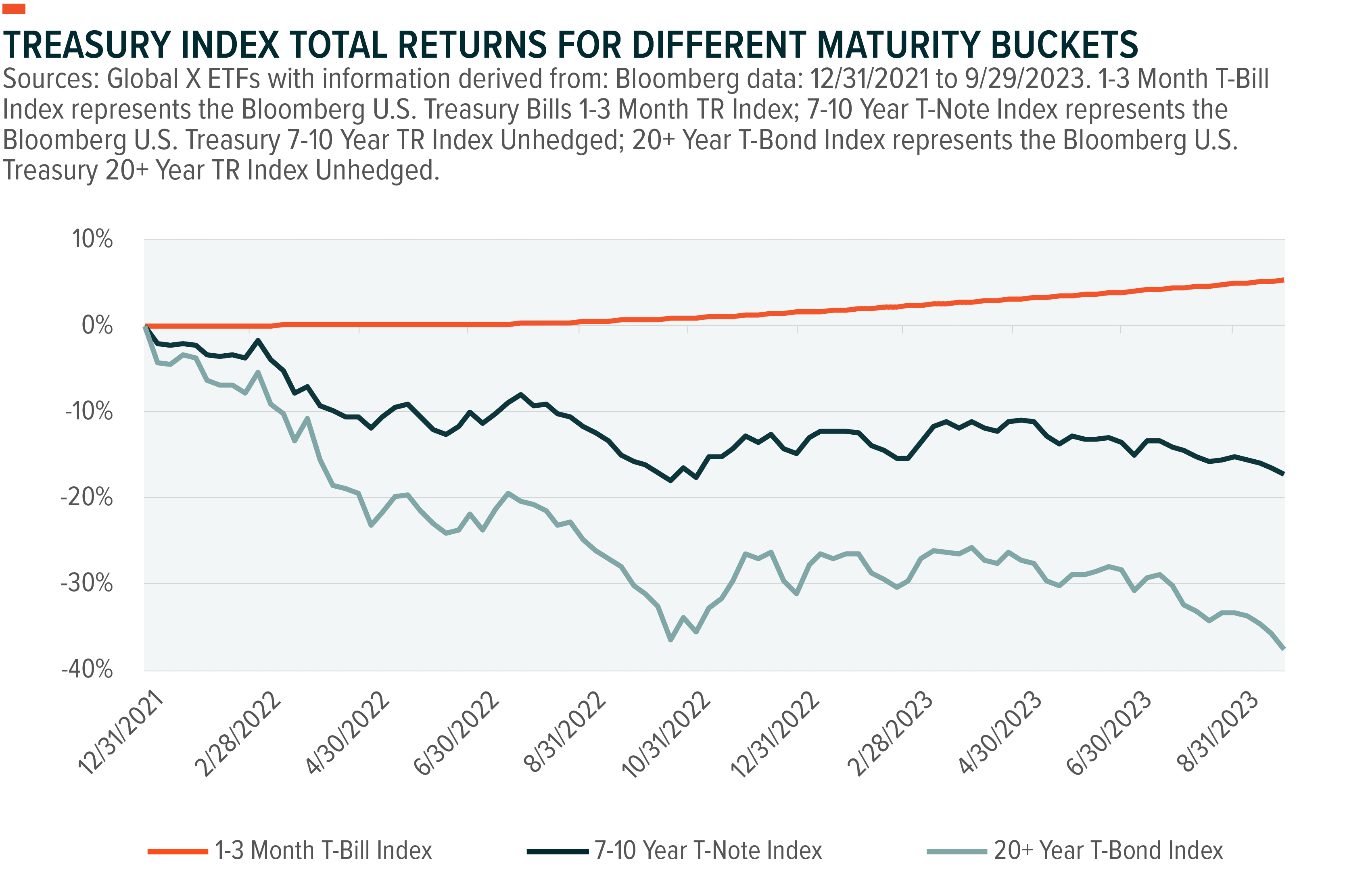

Since the Fed started its hiking cycle, rising short-term rates have generally outpaced rising long-term rates. Over time, this inverted the Treasury curve while bringing down the prices of long-term Treasuries. This negative spread between long and short duration assets shows that investors were not rewarded in 2022 for investing further out the curve.

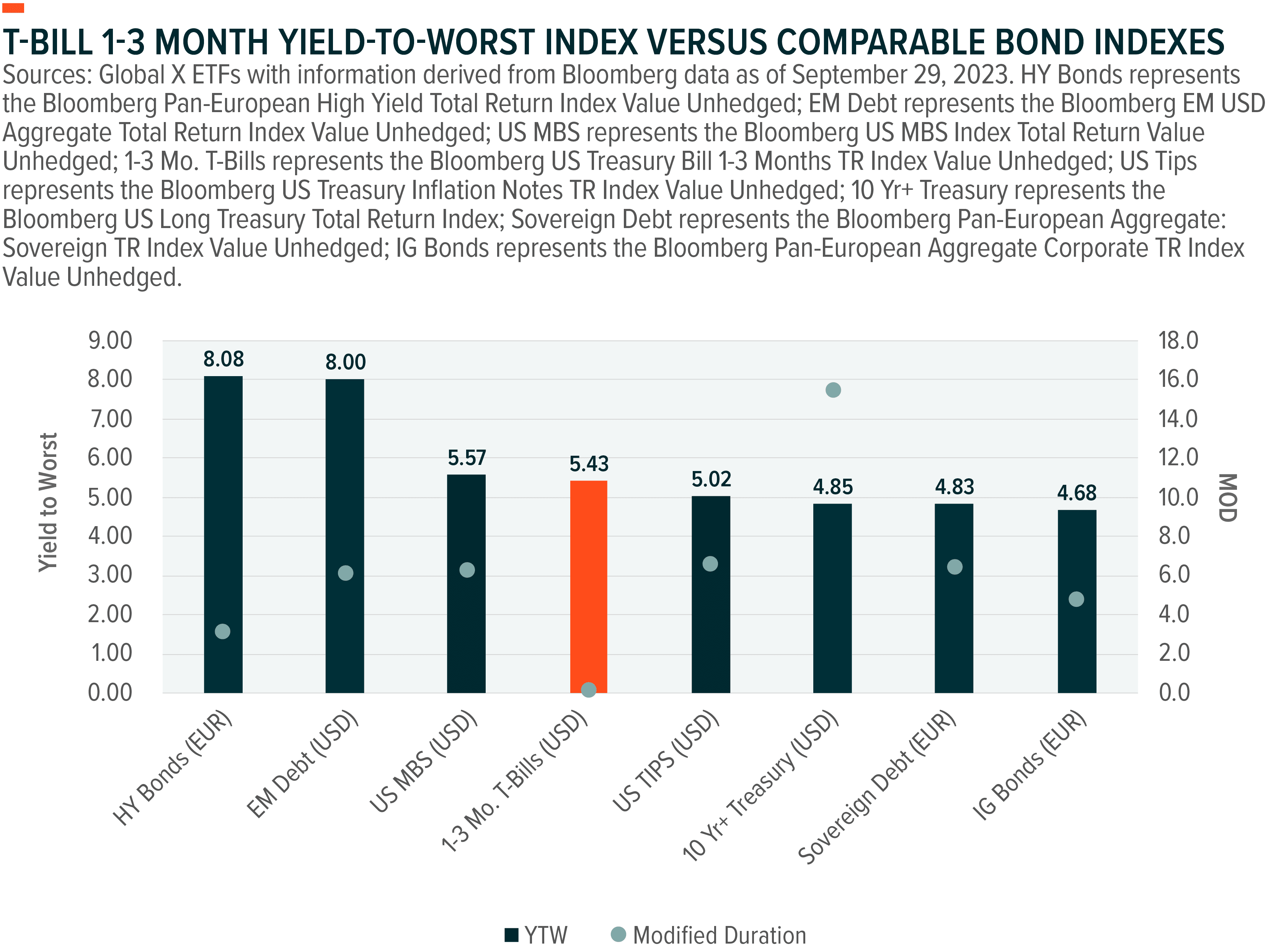

This interest rate risk was evident in the negative performance of longer duration treasury indices over the past year. The Bloomberg U.S. Treasury: 7-10 Year TR Index and the Bloomberg U.S. Treasury 20+ Year TR index both underperformed the 1-3 Month T-Bill Index, reflecting declines of –17.34% and -37.61% respectively, versus the Bloomberg 1-3 Month T-Bill Index’s return of +5.28% over that same period.

While past performance is not indicative of future results, the lower yields of longer-term treasuries may reflect expectations of uncertainty over the horizon, potentially dampening returns in risk assets over the near-term. Additional concerns regarding inflation and the direction of monetary policy may warrant allocations to the safety and liquidity of short-term treasuries as economic conditions evolve.

CLIP LN seeks to offer global investors an alluring option for USD-denominated sovereign debt exposure, providing a liquid investment vehicle that minimises credit and duration risks, at an attractive yield. This makes it an ideal tactical and strategic tool for opportunistic investors, adaptable to any international bond portfolio.

Ease of entry and egress for investments will be important as market conditions unfold. The U.S. Treasury market is the largest sovereign debt market in the world, with $25 trillion worth of securities outstanding;7 1–3-month T-Bills currently comprise the most liquid segment of the Treasuries market, making up approximately 92% of all treasury debt issuance in September 2023.

While the direction of interest rates and economic growth remains uncertain, potential opportunities continue to proliferate as risk assets reprice to more attractive levels. Going forward, opportunities to extend duration or seek opportunities in credit may arise. Elevated real yields, stable returns, and pristine credit quality position CLIP LN as a prime cash-holdings tool for investors to rely on during these uncertain times. Its cash-like liquidity makes it an ideal short-term investment vehicle to wait out market volatility, providing an optimal springboard, should investors need to capitalise on opportunities in the year to come.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Federal Reserve Bank of Atlanta. (2023, October 18). GDPNow.

2. U.S. Bureau of Labor Statistics. (2023, October 12). Consumer Price Index.

3. European Central Bank. (2023, October 18). The Harmonised Index of Consumer Prices (HICP).

4. Bank of England. (2023, October 18). Inflation and the 2% target.

5. SIFMA. TreasuryDirect US Treasury Securities, Issuance Gross. Data as of October 4, 2023

6. Bloomberg. Total ETF Fund flows, Western Europe, U.K, U.S. Exchanges. Data as of October 20, 2023

7. SIFMA. U.S. Treasury Securities Statistics. Data as of October 4, 2023