Uranium 2.0: Nuclear’s Green Narrative Is Intensifying, and Energy Security Is Now Essential

The need to decarbonize the global economy, find a reliable energy supply, and meet rising energy demand has an interest in nuclear power surging. A root cause of the interest in nuclear power, and renewables in general, is Russia’s invasion of Ukraine shifting the world’s energy landscape. European Union (EU) governments continue to warn of a gas emergency with the EU cut off from Russian gas supplies, and they are preparing for a total stoppage this winter. In this report, the latest in our uranium series that includes Uranium, Explained and Nuclear Energy and Uranium Moving Into the Mainstream, we highlight how the current environment has the world embracing nuclear energy as critical to the energy transition and long-term energy security.

Key Takeaways

- We expect nuclear to be a climate change solution based on the U.S. Inflation Reduction Act and a “transition activity” under EU Green Taxonomy, which should boost uranium investment.

- With Europe in an energy crisis, countries may begin to stockpile uranium for use as a backup power source. The enrichment market could change and extend output amid an increase in nuclear energy and uranium demand.

- In terms of perceived risks with nuclear energy, the industry has implemented safe and technologically proven means to transport, store, and dispose of nuclear waste. Also, cost guidance will likely increase across the global mining sector; however, in the uranium industry, most operational expenses are set or hedged against inflation.

Green Energy Transition Readying for a Nuclear Boost

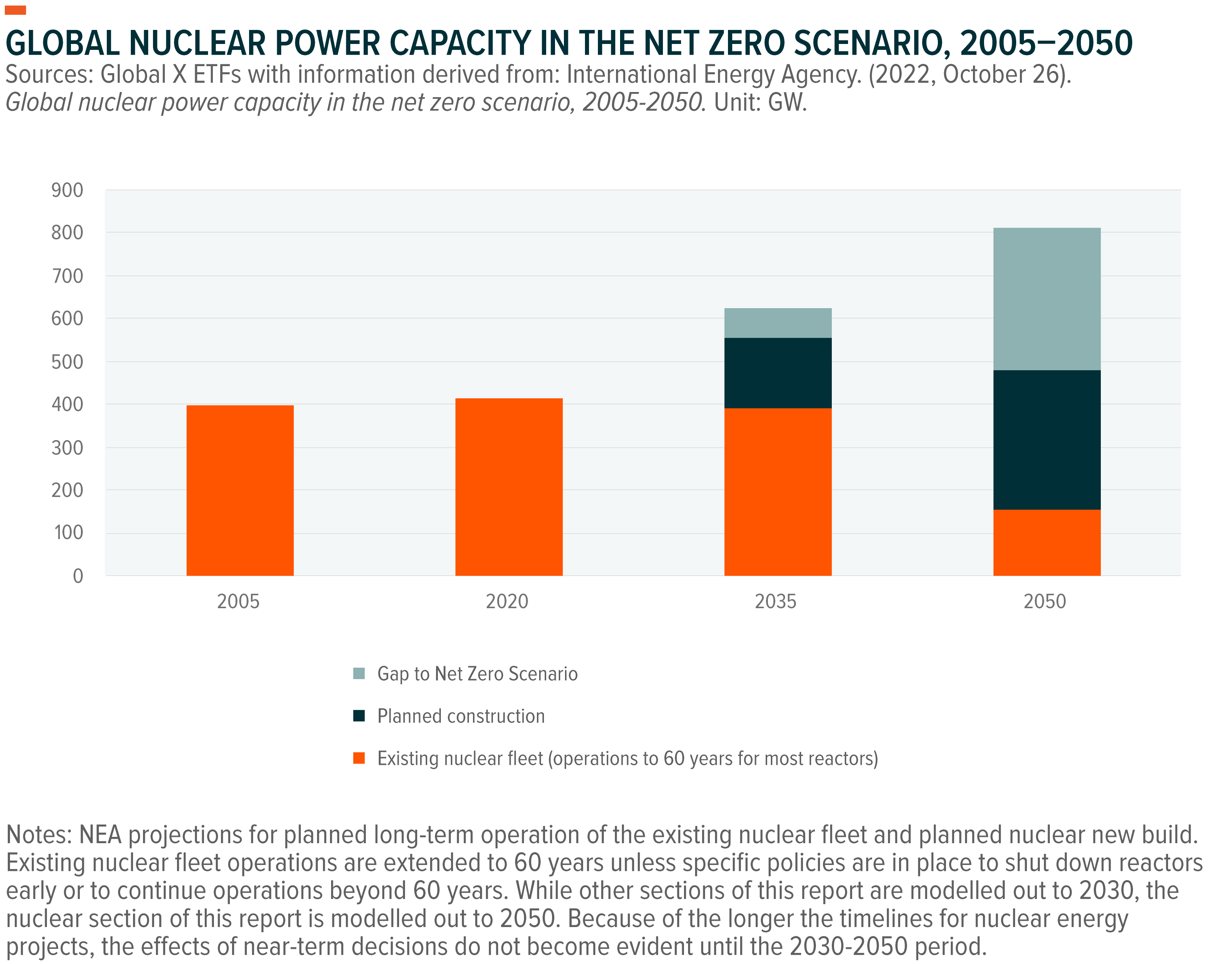

The conversation about nuclear power as a tool to address climate change continues to gain steam. According to the International Energy Agency (IEA), for the world to meet net zero emissions goals, the nuclear sector must double in size over the next two decades (“the Net Zero Scenario”).1 Recent policy may help, as the Inflation Reduction Act (IRA) in the U.S. is predicted to increase investment in the uranium sector, strengthening nuclear energy as a climate solution. The bill, touted as the biggest climate investment in U.S. history, will:

- Establish a nuclear power production tax credit to support current nuclear generators, expanding on the Civil Nuclear Credit Program. The tax credit runs from 2024 to 2032.2

- Swap technology-specific renewable energy tax credits for technology-neutral credits that place advanced nuclear energy on par with other zero-carbon energy generation. The tax credits can be used for production or investment beginning in 2025.3

- Support fuel supply projects for advanced reactors that produce high-assay low-enriched uranium (HALEU), which can make advanced reactors smaller, require less frequent refuelling, and be less wasteful. The bill provides $600 million to the HALEU program to buy enriched HALEU or obtain it by processing Department of Energy (DOE) stockpiles. Additionally, $100 million is for developing suitable HALEU transport.4

In Europe, nuclear technologies are “transition activities” under the EU Green Taxonomy, a classification that should improve investor confidence in uranium. In July 2022, the European Parliament didn’t object to the Commission’s Taxonomy Complementary Delegated Act, which, therefore will be in effect starting January 2023 with nuclear energy classified as green energy.5 Research, development, and deployment of cutting-edge technologies that reduce nuclear waste and heighten security, a class of reactors known as Generation IV, are among the nuclear-related actions included in the taxonomy.

Europe’s Energy Shock Makes Energy Security a Priority

After Russia stopped sending gas to Europe through the Nord Stream pipeline, Europe quickly realized the necessity for energy security and independence. Europe has adapted to the situation by diversifying its sources of gas imports from Middle East, Algeria, Norway, and the US. 6 For example, the continent increased its gas imports from the Middle East (Iran and Turkey) by 22% from January 2022 (before Russia invaded Ukraine) to September 2022. 7 The diversification of energy sources is also material: the IEA highlighted the need for a “massive surge” in investment to face the energy shock and speed up the transition to clean energy. 8

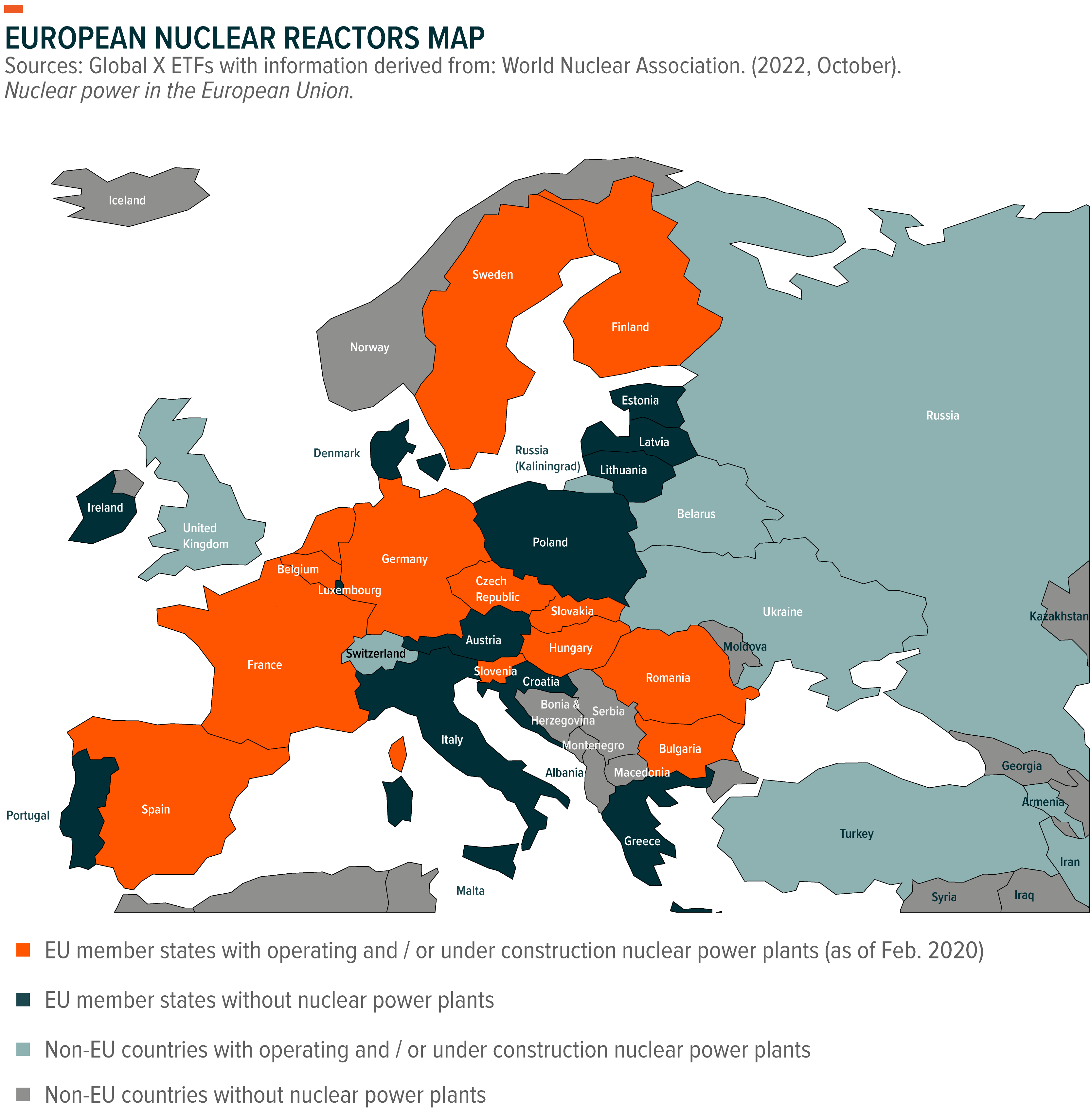

As part of this surge, nuclear power is being promoted as a clean energy alternative that can help improve energy independence. The ability to store uranium as a strategic reserve to secure energy supply is another way in which nuclear power can help countries achieve energy security, in addition to the fact that nuclear is the most dependable energy source because it has the largest capacity factor, as previously noted. France’s longstanding energy security strategy relies heavily on nuclear power, and the country accounted for more than half of EU uranium demand as of March 2022, followed by Spain, Sweden, and Belgium.9

In 2020, the European Atomic Energy Community (Euratom) reported that EU-27 utilities received 12,592 tonnes of mined uranium, or about 26% of the world’s supply from mines.10 Niger, Russia, Kazakhstan, Canada, Australia, and Namibia were the key suppliers.11 Most nations that mine uranium do not produce nuclear power, so uranium transport is vital. Since 1961, International Atomic Energy Agency (IAEA) standards have governed radioactive material shipping. Uranium oxide concentrate, known as yellowcake, is carried from mines to conversion plants by road, rail, and ship in 200-litre drums, each holding about 400 kg U3O8, packed into shipping containers.12

In the wake of Russia’s invasion of Ukraine, governments around the world are revisiting commodities supply chains and trade management, especially in the energy sector. On this path, potential sanctions on uranium imports from Russia have also been considered. 13 On the other side, the risk of Russia halting uranium exports as a retaliatory measure also supports the need to reduce Russian imports of nuclear-reactor fuel.

Potential sanctions on Russian uranium, which represents 6% of the global uranium supply, are likely to affect the broader market, making it even tighter than it already is.14 According to the European Atomic Energy Community, the uranium that originates outside the EU-27 accounts for 95% of EU domestic total consumption, and Russia is the second-biggest source of uranium for EU member states behind Niger.15

Russia has roughly 43% of the global enrichment capacity, Europe 33%, China 16%, and the U.S. 7%.16 Some spare capacity can be found in the U.S. and Europe. China is expanding its capacity considerably, in line with domestic requirements.

The Biden administration introduced legislation “to build a stronger domestic nuclear fuel supply for the future” under a Nuclear Fuel Security Program.17 This legislation can be viewed as an attempt to wean off Russian uranium imports, which the U.S. is somewhat reliant on currently. Russia accounts for 16.5% of the uranium imported into the U.S. and 23% of the enriched uranium needed to power U.S. commercial nuclear reactors.18

The opportunity for the U.S. uranium industry is significant, as the country has only one commercial enrichment facility, owned by Urenco Ltd. The administration’s $4.3 billion investment would go toward buying low-enriched and other forms of uranium directly from U.S. producers, boosting domestic manufacturing and securing fuel for the advanced reactors now under development.

The Asia-Pacific Region Is Essential to the Nuclear Industry’s Growth

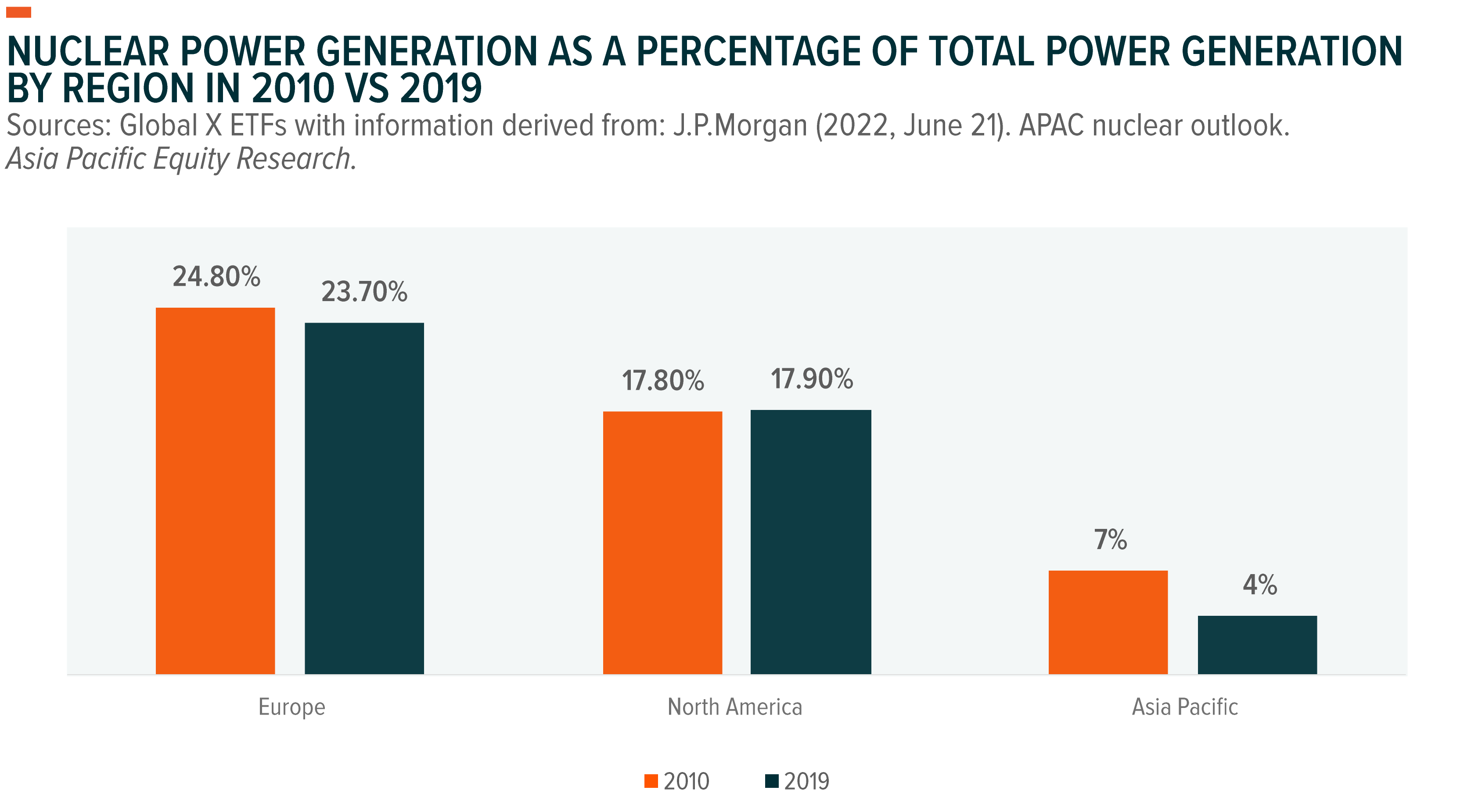

Nuclear power only accounts for 4% of the energy market in Asia-Pacific (APAC), compared to 24% in Europe, the Middle East, and Africa (EMEA) and 18% in the Americas.19 However, APAC is crucial for the expansion of the nuclear industry; most countries including Japan, China, India, and South Korea, have a nuclear program in development. For example, South Korea has a 15-year energy strategy. Under the plan, nuclear power would account for about one-third of the country’s energy mix by 2030, enhancing energy security and fulfilling climate targets.20

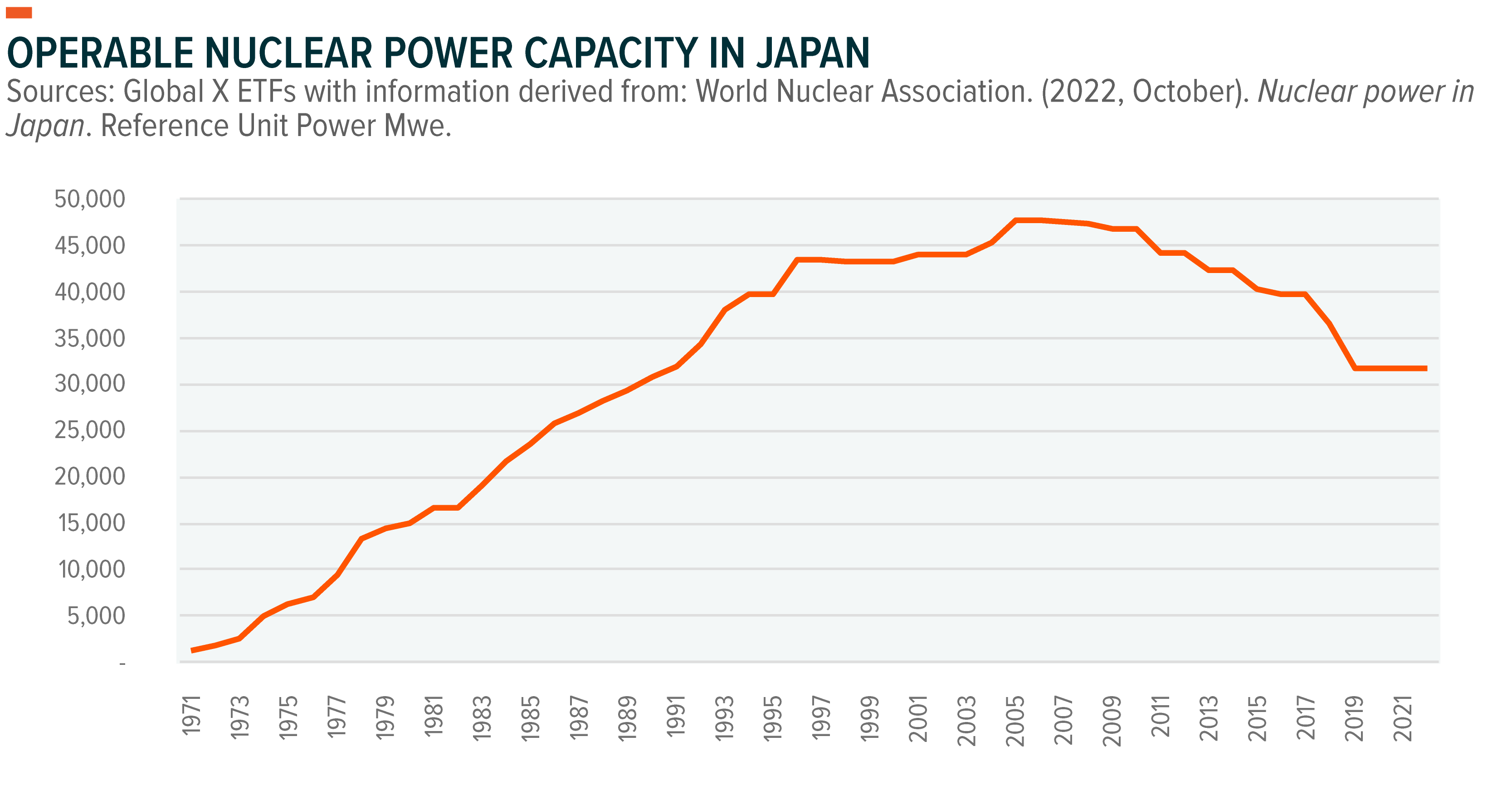

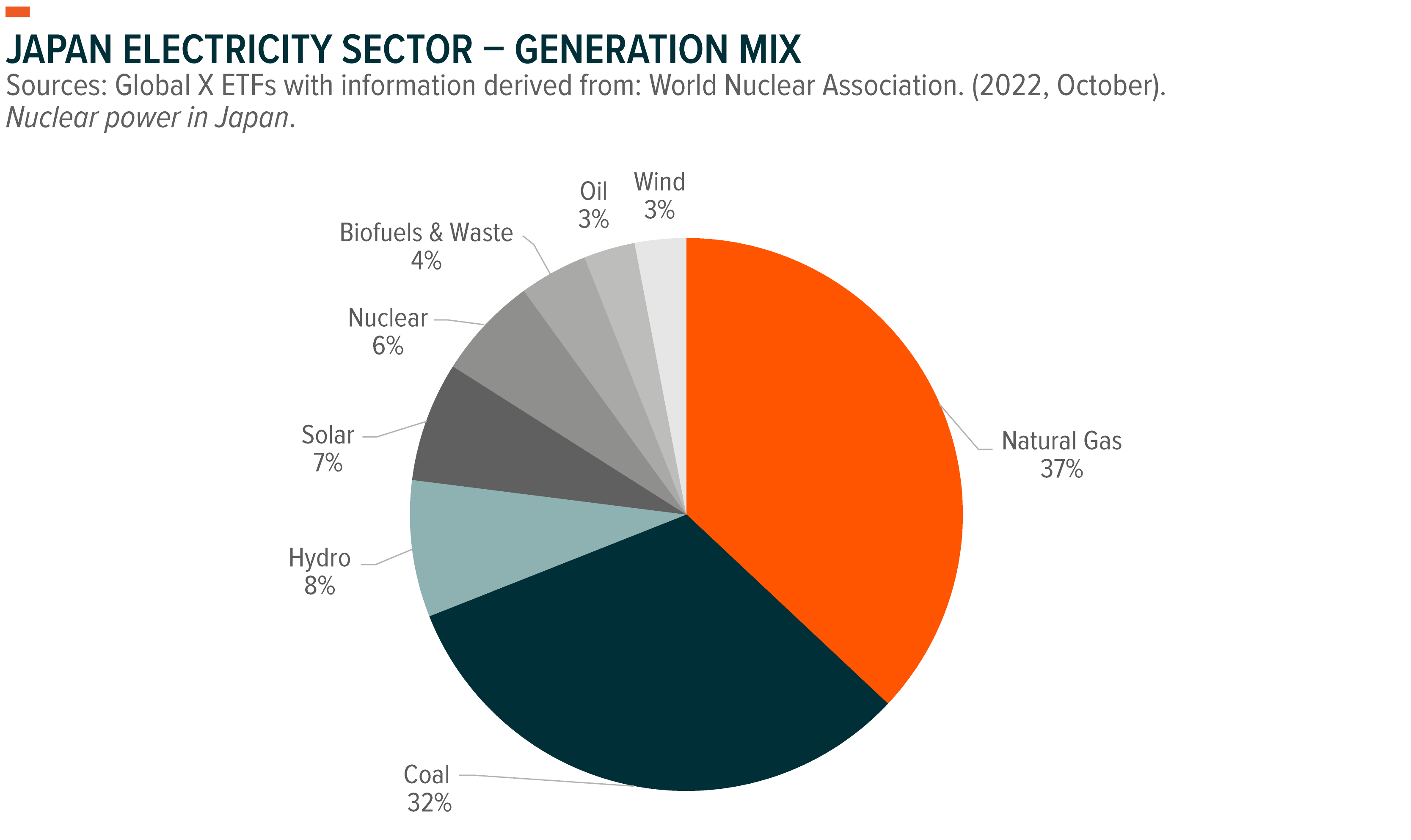

In Japan, Prime Minister Fumio Kishida aims to re-establish Japan as a nuclear-powered nation for the first time since the 2011 Fukushima disaster.21 Before Fukushima, Japan derived almost one-third of its power from nuclear reactors.22 According to the International Atomic Energy Agency, Japan had 50 generating reactors, but 46 were shut down following the tragedy.23 As a result, in the years since, Asia’s most advanced economy has consumed more coal, natural gas, and fuel oil, despite its goal to attain net zero carbon emissions by 2050. As of June 2022, the World Nuclear Association said that Japan needs to import about 90% of its energy requirements.24 For Japan to achieve its goal of becoming carbon neutral by 2050, nuclear power may be required.

Finally, China’s nuclear industry has expressed confidence in its ability to speed its expansion plans. The China Nuclear Energy Association considers 6–8 new reactors a year through 2025 a reasonable goal, with as many as 10 also possible.25 As we noted in Uranium, Explained, China has the most ambitious nuclear program with plans to construct roughly 150 new reactors in less than two decades. If completed, China would triple its nuclear energy capacity and become the world’s largest nuclear power producer, ahead of the EU and the U.S.

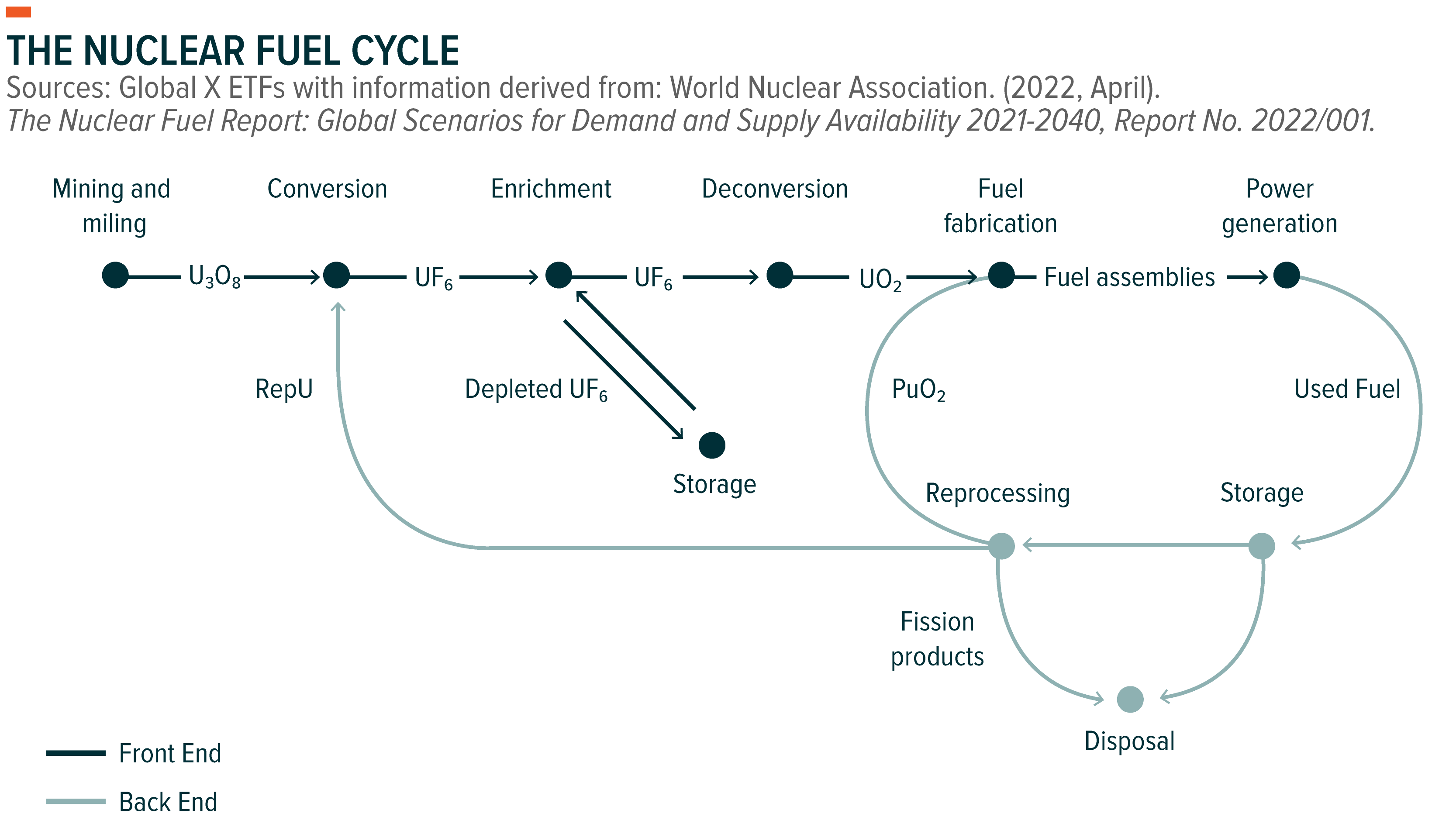

Uranium Enrichment Is Key to Getting the Ball Rolling

To generate nuclear energy, the utilities that buy uranium from the mines need a certain quantity of enriched uranium. Uranium consists of two main isotopes, U-235 and U-238, that are chemically identical but different in mass. Their difference in mass allows the isotopes to be separated and makes it possible to increase, or “enrich,” the percentage of U-235. The fission of the U-235 atoms generates nuclear energy. Lower levels of enriched uranium, such as uranium with 5% U-235, are commonly used for nuclear reactor fuel.

Historically, the uranium enrichment process has a good degree of inertia. Even when enriched uranium demand declined following the Fukushima accident, enrichment plants continued operating because it was costly to shut down and re-start centrifuges.

Primary and secondary supplies are the two basic divisions of uranium supply. Mined and processed uranium is referred to as the primary supply, while reprocessed uranium that is added back into the fuel cycle is the secondary supply.

The ability to redirect excess enrichment supply to uranium production by underfeeding (operating at low tails assay) affects the secondary uranium supply. Currently, enrichment facilities are underfeeding because of the oversupply of enrichment capacity worldwide. Underfeeding is more prominent since the implementation of centrifuge technology, and gas centrifuges need to remain online even as enrichment demand drops away. A centrifuge is required to spin continuously for long periods.

However, the enrichment market could change and extend output amid an increase in nuclear energy and uranium demand. In line with this expectation, Urenco, one of the leading international suppliers of enrichment services, stated in its most recent annual report that “The enrichment market is recovering and now approaching a level which allows us to plan for reinvestment in plant capacity.”26 In addition, a potential ban on Russian enriched uranium from the U.S. and the EU would likely lead other enrichment plants to step in. Capacity at enrichment facilities would have to be ramped up, leading to overfeeding.

Structural Risks: Nuclear Waste

Radioactive waste is among the key risks associated with nuclear power plants. However, nuclear power generates little waste, and the waste that it does generate is carefully controlled. All U.S. nuclear power reactors store spent nuclear material in thick concrete with steel liners 40 feet underwater.27

Used fuel assemblies cool in a pool after being removed from a reactor. The pool and water protect employees from radiation. The fuel is usually pool-cooled for five years before being casked. The waste is then stored for about 40 years in dry casks which are enormous steel-reinforced concrete containers.28 Indeed, these barrels are for long-term storage until a disposal location is available. The two main types of nuclear waste are front end and back end. Front-end nuclear waste comes from uranium mining and contains depleted radium, which is incredibly dense and commonly repurposed into tank shells and other durable metals. Back-end nuclear waste is gamma-radiated spent fuel rods with long half-lives.

As seen, after being removed from the reactor for about five years, spent fuel is transported to dry casks. Since the 1970s, the global nuclear business has completed more than 2,500 cask shipments of spent fuel without radioactive emissions, casualties, or environmental damage.29

Nuclear power generates much less waste than thermal power, for example. Since the 1950s, the U.S. has generated just 90,000 metric tonnes of wasted fuel, which could fit on a single football field 10 yards deep.30 The nuclear industry has devised safe and technologically proven means to transport, store, and dispose of radioactive waste. Radioactive waste accounts for less than 10% of all hazardous items carried annually in the U.S.31

When compared to other types of industry, the nuclear power business generates relatively little waste. Globally, the vast majority, or 97%, of waste is considered to be either light or moderate (LLW). Toxic materials of this type have been routinely disposed of in near-surface repositories for decades. In France, for example, only 0.2% of radioactive waste is considered high-level waste (HLW), despite the country’s extensive fuel reprocessing industry. 32

Because radioactive waste is handled carefully and decays naturally, it shouldn’t be too much of a concern for nuclear power plants. In addition, the U.S. Department of Energy announced up to $40 million in financing for a new Advanced Research Projects Agency-Energy (ARPA-E) initiative. This program will restrict waste from advanced nuclear reactors, safeguarding the land and air and promoting nuclear power as a stable source of clean energy.33

Contingent Risks: Cost Inflation

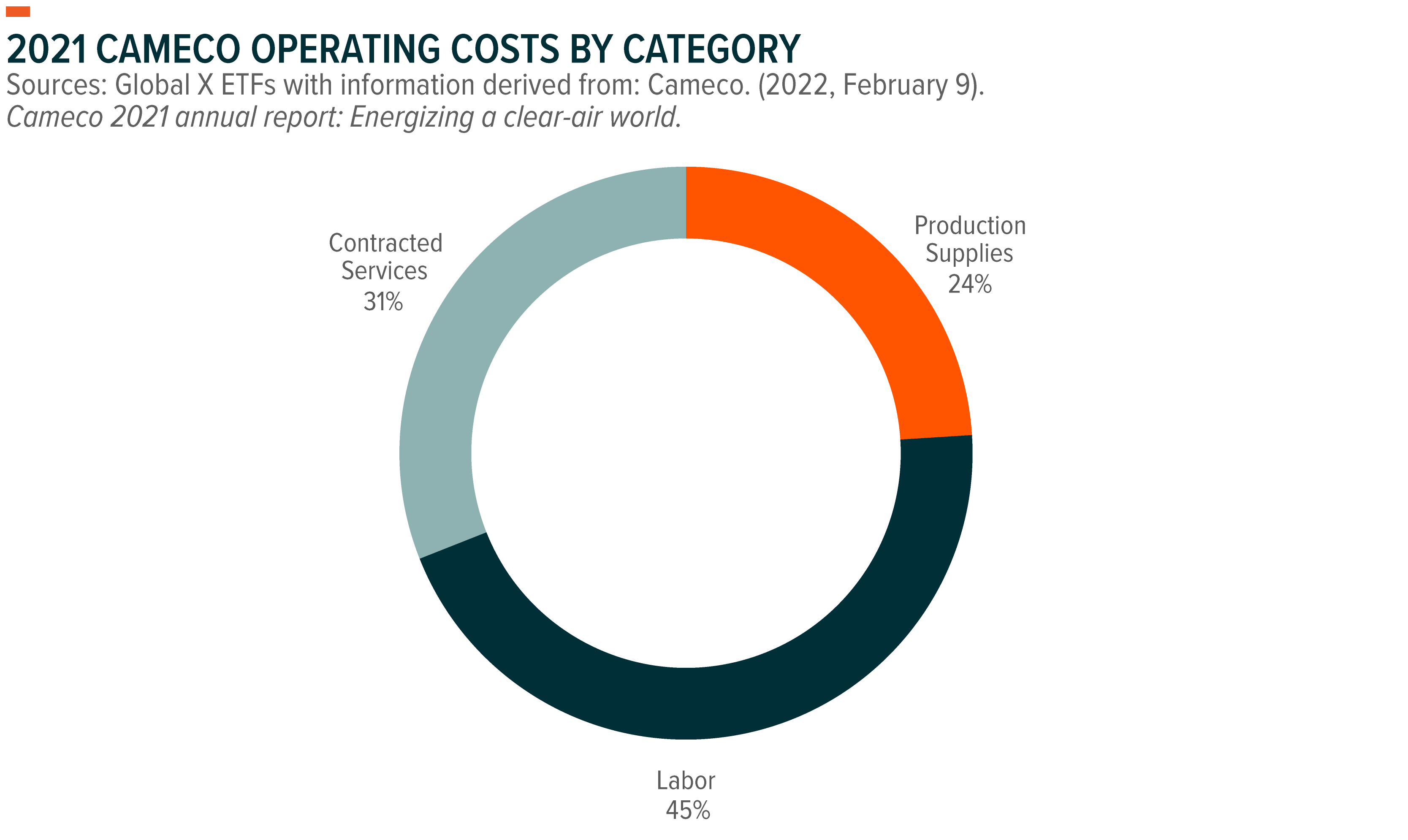

The global mining sector will likely report higher-cost guidance for 2022 due to inflation. Like all mining companies, uranium mining companies are affected by the cost of inputs such as fuel and labour, which is their most significant cost category. For example, labour accounted for 45% of Cameco’s costs in 2021, contracted services 31%, and production supplies 24%.34Also, uranium implies a lower transport cost than coal, oil and gas due partly to the high energy density.

We expect the overall impact of price changes on mining cash flows to be small and mining companies to continue to provide a solid revenue stream. According to Cameco, “Uranium prices will need to reflect the cost of bringing on new primary production to meet growing demand.”35 Uranium mining companies have large, creditworthy customers that continue to need uranium despite fluctuations in economic conditions.

Uranium demand from utilities has been consistent. Utilities typically purchase their requirements many years in advance, taking into account the long time it takes to process and convert natural uranium into fuel assemblies. Power plants usually locate sources of uranium 12–24 months ahead of its projected usage.36 Once found, negotiations typically translate into long-term contracts ranging 3–15 years.37 Long-term contract arrangements suit utilities because they know their forward requirements many years in advance, and they serve the uranium miners by providing stability.

Typically, long-term commitments include a mix of fixed-price, base-escalated pricing, and market-related pricing mechanisms. Base-escalated contracts use a pricing mechanism based on a term-price indicator when the contract is accepted and escalated over the contract term. A base price is agreed to and fixed in the contract. It is also agreed that this price will escalate, generally in line with inflation. For example, the escalator could be the U.S. Consumer Price Index, to essentially prevent the contract from devaluing in real terms.38

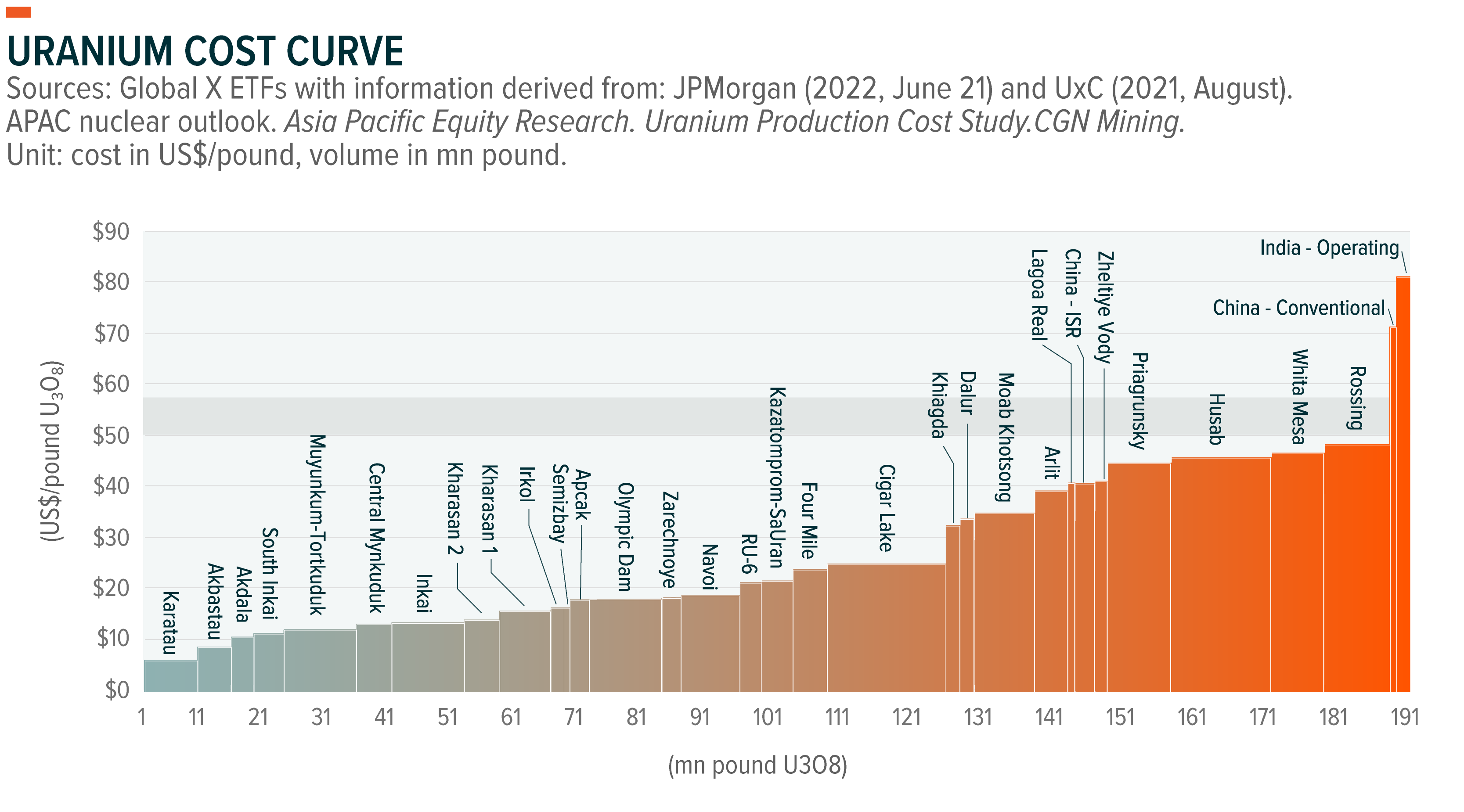

The inflation hedging and the focus on keeping operating margins high and costs lean should mitigate large spikes in miners’ output as miners increase production based on contracted utility demand. In addition, the uranium industry is investing in new technology and business process improvements that can help keep costs in check. Also working in favour of cost control is that the preferred method for extracting uranium, In Situ Leach (ISL) mining, is the most cost-effective and environmentally acceptable method of mining available today. In 2019, this method accounted for 57% of the world’s mined uranium mined.39

According to the cost curve, the increase in the uranium price to US$50 per pound may cause worldwide uranium capacity to increase. Indeed, when the price of uranium reaches US$50 per pound, some mines may find it profitable to resume operations.40

Conclusion: Nuclear Power Gaining Favour

The energy crisis and the demand for energy security have the world reassessing the entire energy supply chain and its critical commodities. With the energy produced by nuclear fission hundreds of times greater than the energy produced by burning the same quantity of fossil fuels, and considerably cleaner, 41 nuclear power is an increasingly important part of the world’s energy mix. Uranium consumption is rising with nuclear power on the energy agendas of many nations, including Japan, which speaks volumes about the energy mix shift over the last decade-plus. Decarbonizing the global economy, ensuring reliable electricity, and satisfying rising energy demands are all reasons why attitudes about nuclear power are shifting, and why we view the uranium sector as one to watch.

This document is not intended to be, or does not constitute, investment research