Europe

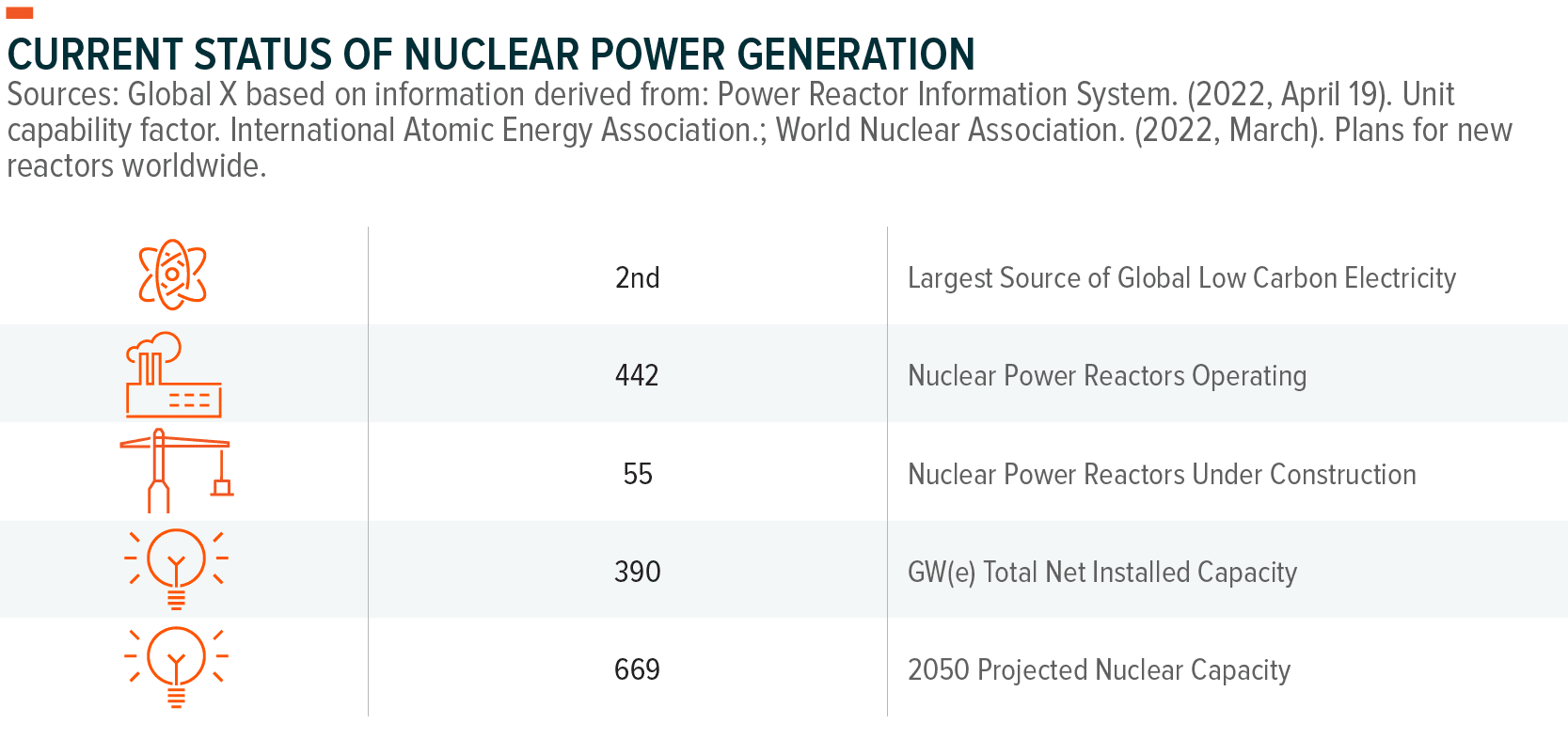

Nuclear power is a clean, efficient, and essential source of electricity used to meet the world’s growing energy demands. Nuclear power can produce electricity at a greater scale while minimising greenhouse gas emissions. This helps countries expand their electricity grid and usage, while limiting air pollution. Roughly 9% of the world’s electricity was generated from nuclear power in 2022 accounting for approximately 30% of the world’s low-carbon electricity.1,2 According to the new projections, to meet energy transition goals by 2050 about 800 GW of new nuclear power may be needed, which may represent around 20 per cent of potential global electricity consumption.3

Uranium fuel enables nuclear power plants to generate electricity. A single uranium pellet, slightly larger than a pencil eraser, contains the energy equivalent of a ton of coal, three barrels of oil, or 17,000 cubic feet of natural gas.4 Global nuclear power output primarily drives the demand for this commodity. Despite expected growth in nuclear power, and a correlative increase in uranium demand, gaining exposure to this commodity sometimes proves difficult. Uranium trades with thin liquidity on futures exchanges and there are ownership restrictions related to its usage in weapons production.

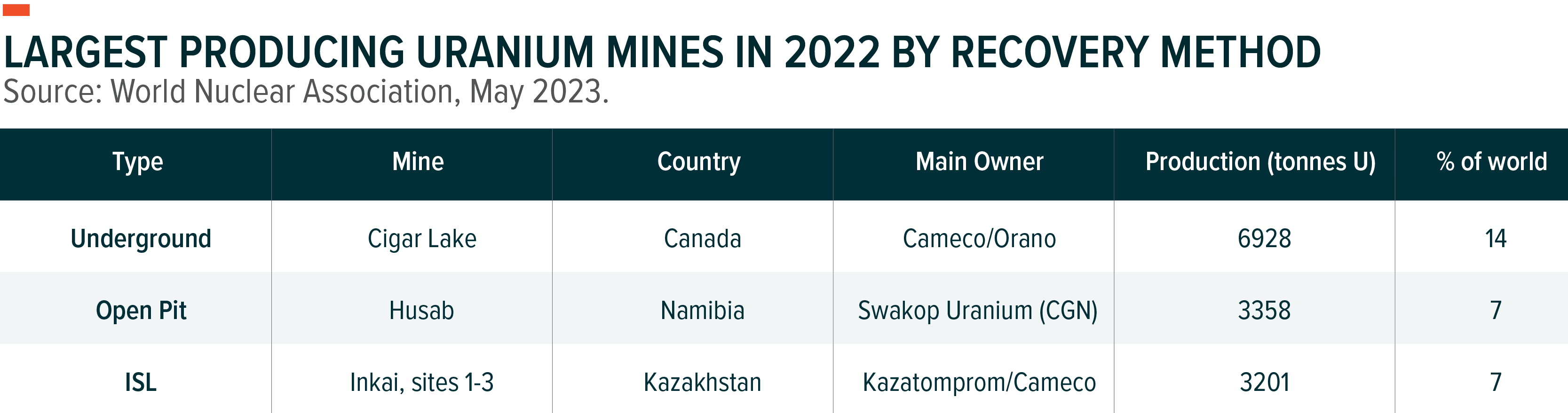

Uranium is a heavy, dense, and radioactive metal, making it a potent source of energy. Found in most rocks in concentrations of two to four parts per million, it appears as commonly in the Earth’s crust as several other metals, such as tin and tungsten.5 Uranium extraction generally involves recovery from the ground using open-pit mining, underground mining, in-situ leach (ISL) and heap leaching methods.6

When uranium is near the surface, miners dig the rock out of open pits. Open pit mining strips away the topsoil and rock that lie above the uranium ore. When uranium is found deep underground, miners must dig underground mines to reach it. The rock is then removed through underground tunnels.

When the removal of the uranium minerals is accomplished without any major ground disturbance, it is done through ISL mining. Weakly acidified groundwater (or alkaline groundwater where the ground contains a lot of limestone such as in the USA) with a lot of oxygen in it is circulated through an enclosed underground aquifer which holds the uranium ore in loose sands. The leaching solution dissolves the uranium before being pumped to the surface treatment plant where the uranium is recovered as a precipitate.7

Heap leaching involves dissolving a chemical in a liquid. Spraying chemicals over piles of crushed rock containing uranium results in the leftover rock and a uranium-containing liquid, much like pouring hot water over discarded coffee beans produces waste coffee grounds. The liquid must next undergo further processing in order to recover the uranium.8

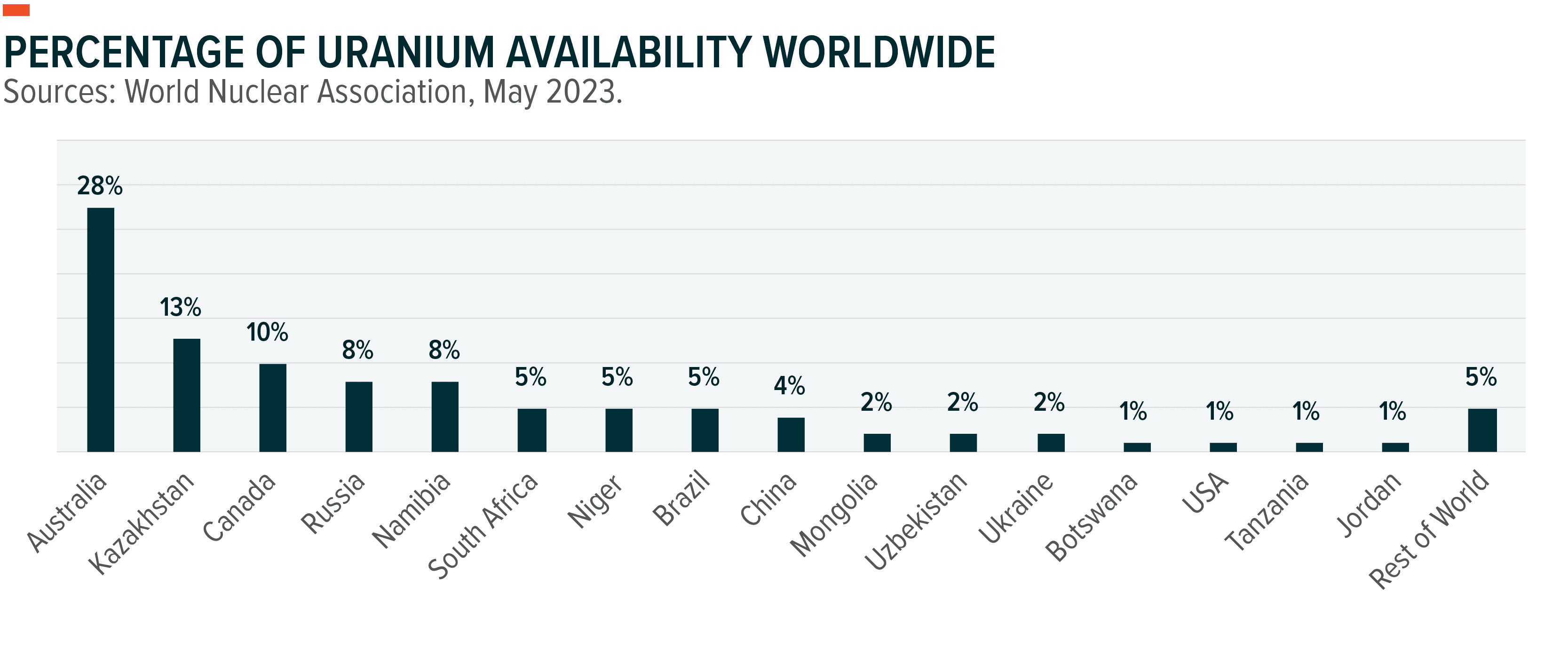

Uranium can be found in many parts of the world but is fairly top heavy in where the reserves can be found. Countries such as Australia, Kazakhstan, and Canada often lead the uranium production charge, but uranium is present across many nations globally.

Nuclear power remains one of the few sources of electricity that combines large-scale power output and low greenhouse gas emissions, with costs comparable to those of traditional fossil fuel power stations.9

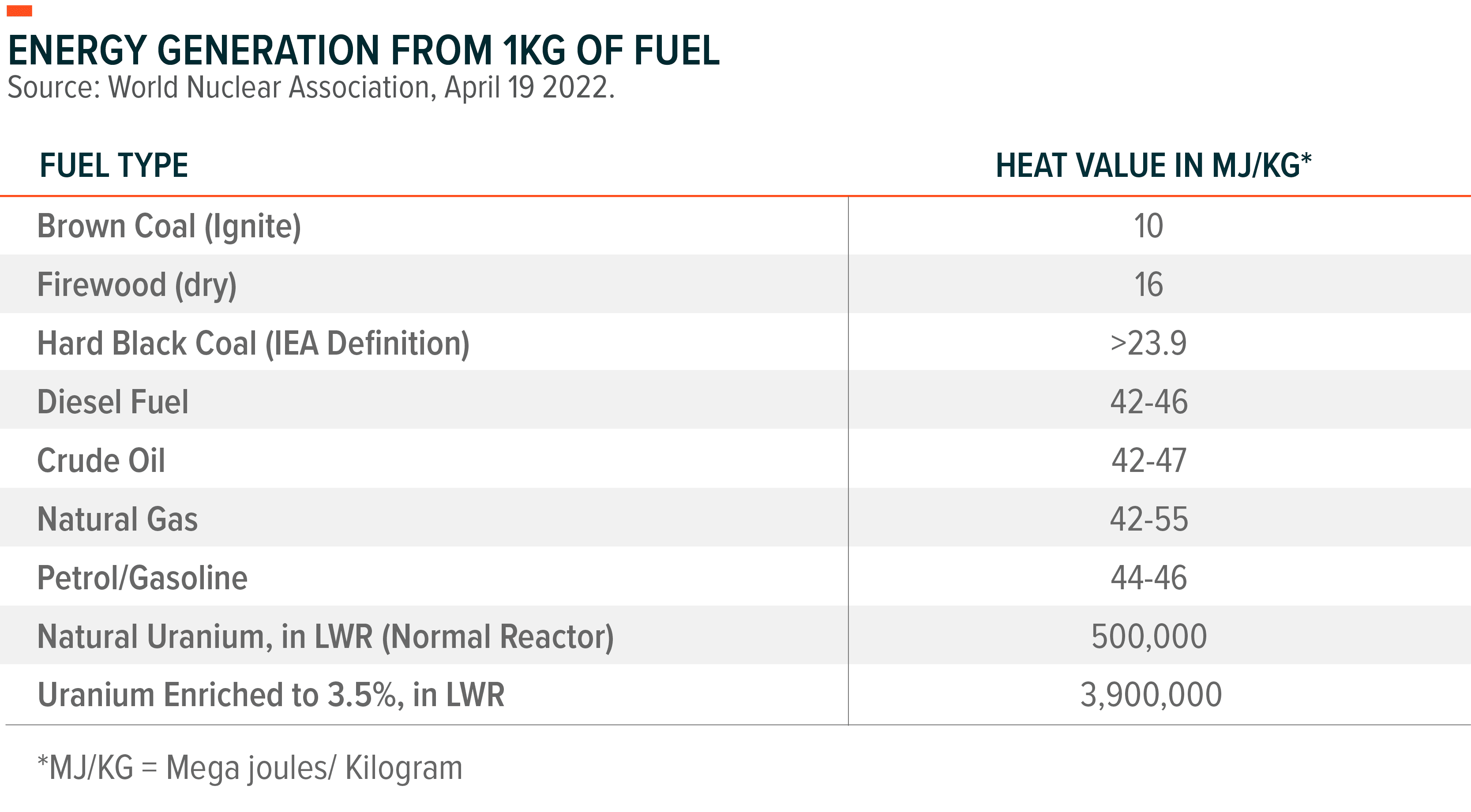

Similar to coal or natural gas power plants, nuclear reactors generate electricity by producing immense heat. This heat produces steam, which propels a turbine connected to an electric motor. As the turbine rotates, the electric motor produces electricity. In nuclear power stations, however, the heat generated derives from splitting uranium-235 atoms in the process of nuclear fission, as opposed to burning fossil fuels.10

Nuclear fission produces thousands of times more energy than that released through the process of burning similar amounts of fossil fuels, making nuclear power a very efficient method of generating utility-scale power.11 Additionally, the ongoing fuel costs for nuclear power plants tend to remain quite low due to the minimal amount of material needed to power the plant.

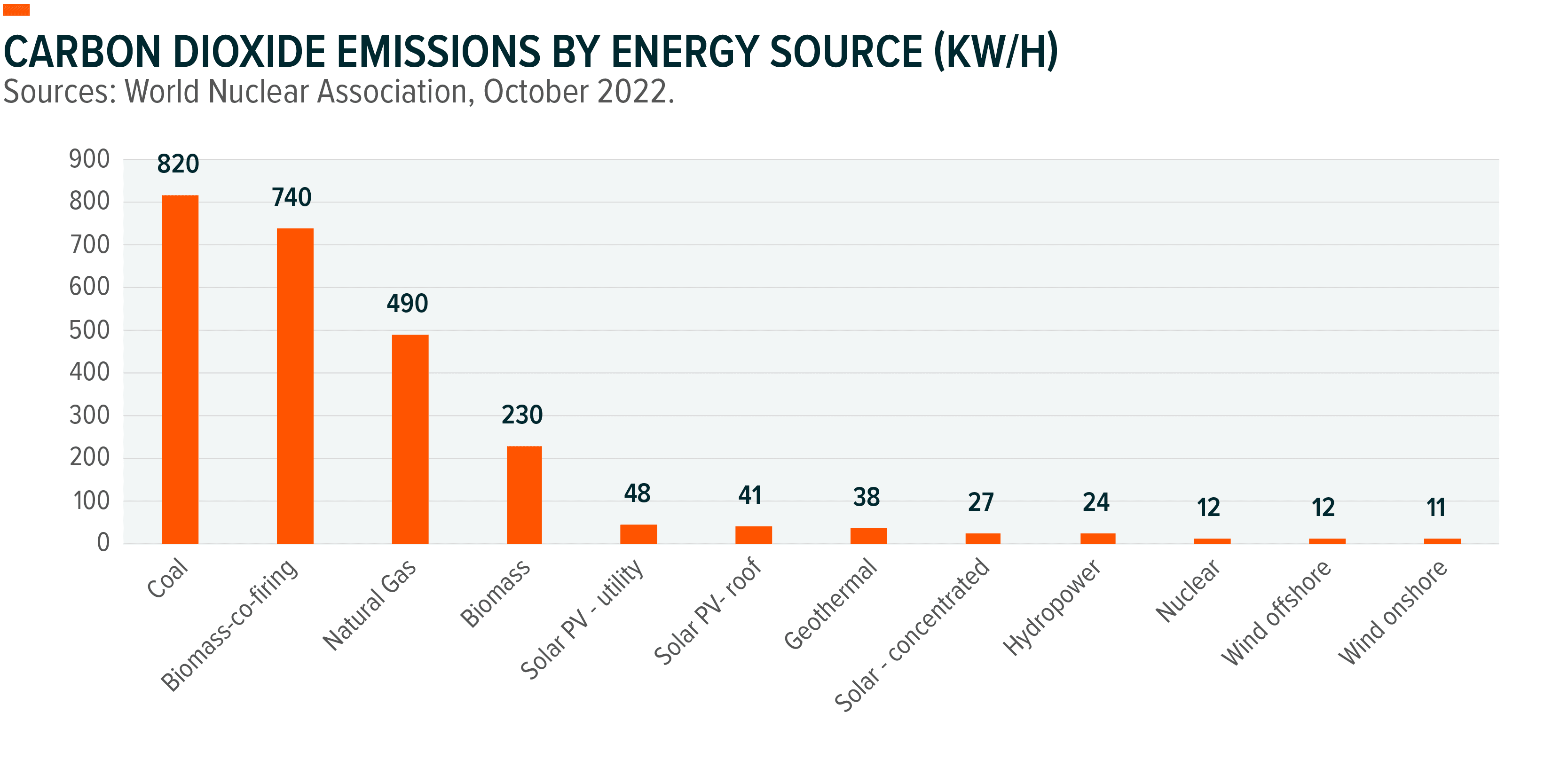

In addition to the power density advantage of uranium, nuclear power also ranks among the cleanest methods of producing electricity, as measured by greenhouse gas emissions. The U.S. Environmental Production Agency estimates that 35% of global greenhouse gas emissions derive from electricity and heating (25%), as well as other energy sources (10%), giving nuclear adequate room to lower global emissions, while increase total share of electricity generation along with wind, solar, hydropower. 12

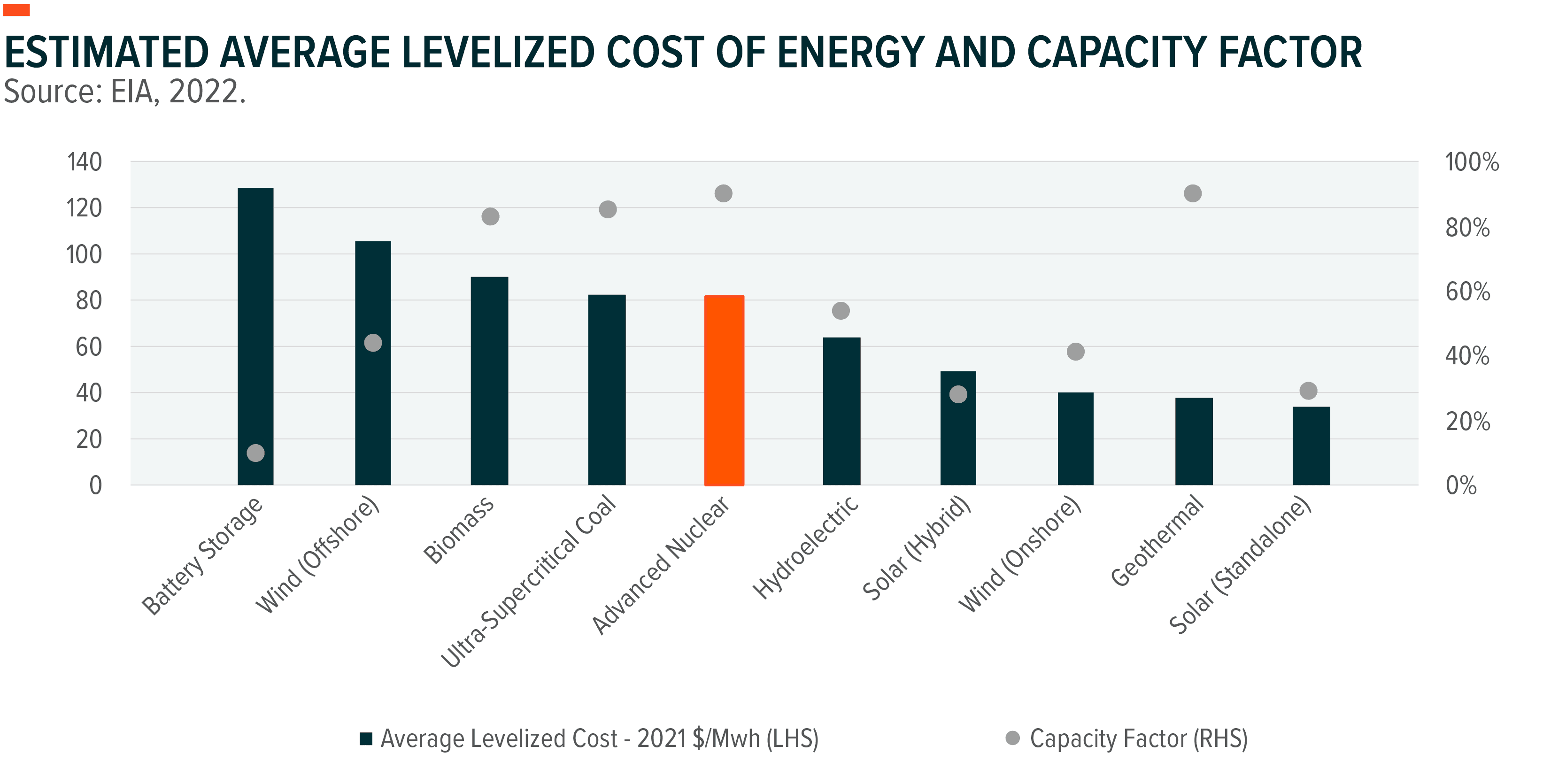

In terms of levelized costs, nuclear power provides a cheaper alternative to coal and biomass, while remaining significantly more cost competitive than offshore wind.13 As a note, while onshore wind and solar are considerably less capital intensive than nuclear, these tend to be less reliable energy sources and qualify as variable renewable energies (VREs). This means they produce energy intermittently, rather than on a demand basis, creating variability in availability when the wind neglects to blow or the sun doesn’t shine. The lower dependency associated with VREs is highlighted when analysing the capacity factor for nuclear against solar and wind.

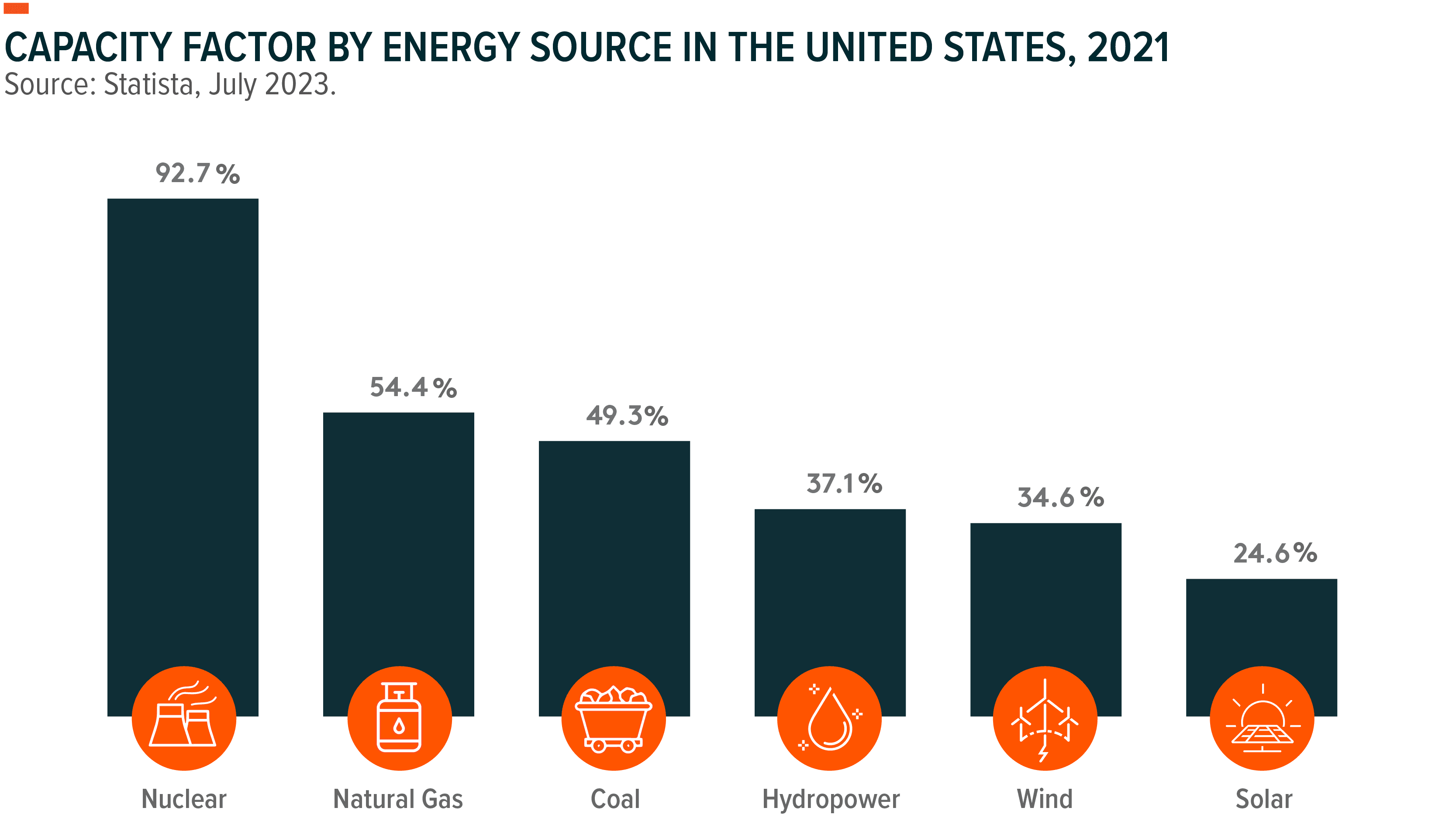

When comparing power sources with unequal capacity factors, the calculation of the final cost of energy production must include storage costs, since demand spikes and periods of low energy production availability require storage reserves to mitigate blackouts for lower capacity factor sources. The average levelized cost of battery storage is more expensive than nuclear, particularly notable given that nuclear plants achieve greater reliability than wind and solar plants.14 Contrary to popular belief, capacity and electricity generation for various fuel sources do not always align. For example, U.S. nuclear utility-scale electricity generation capacity account for 8% of the country’s total capacity in 2022, but generated over 18% of electricity that year, demonstrating the importance of the energy source’s capacity factor.15 For this reason, we see nuclear working in tandem with wind, hydroelectricity, and solar, rather than in competition, by safeguarding energy stability.

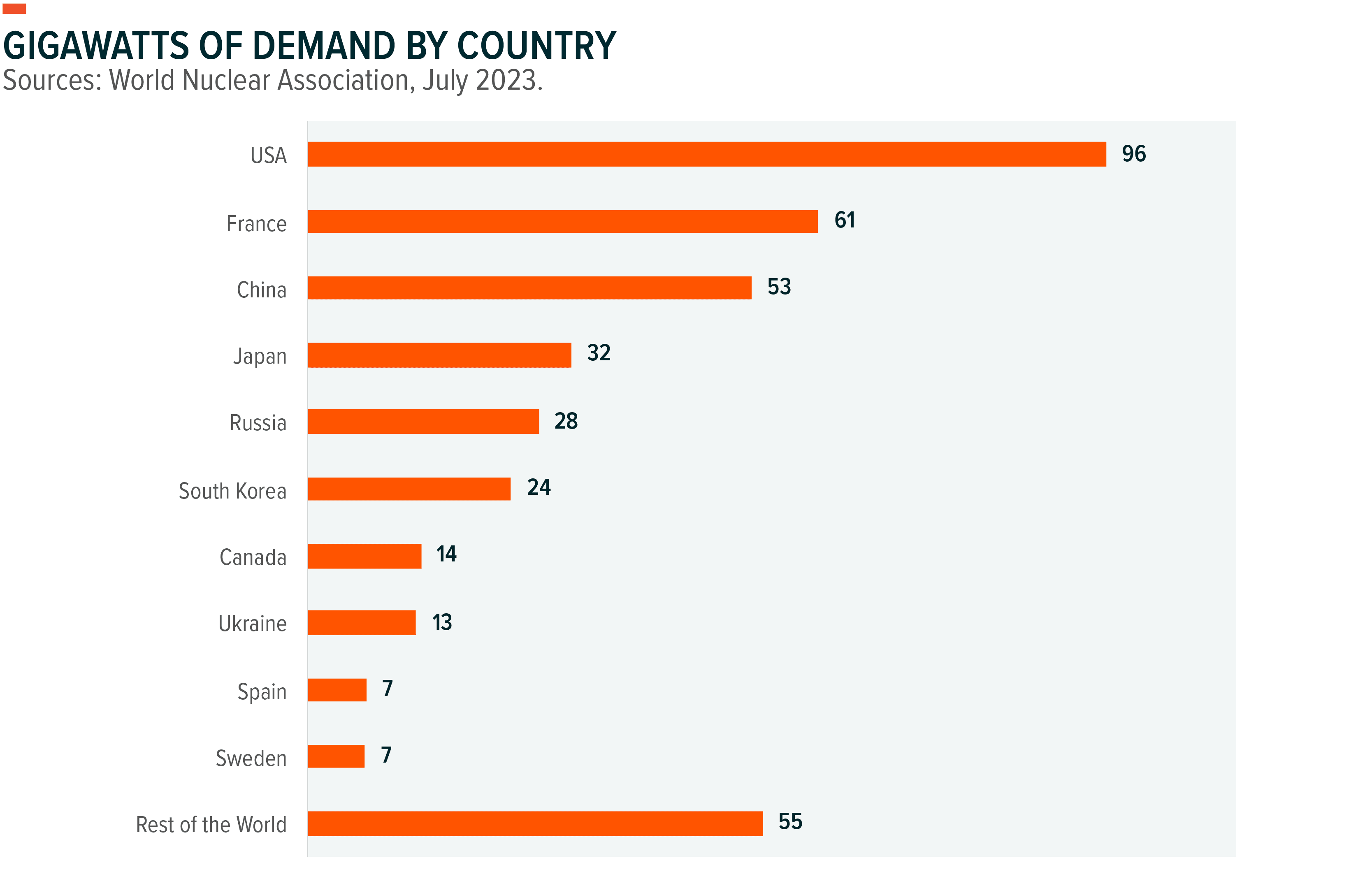

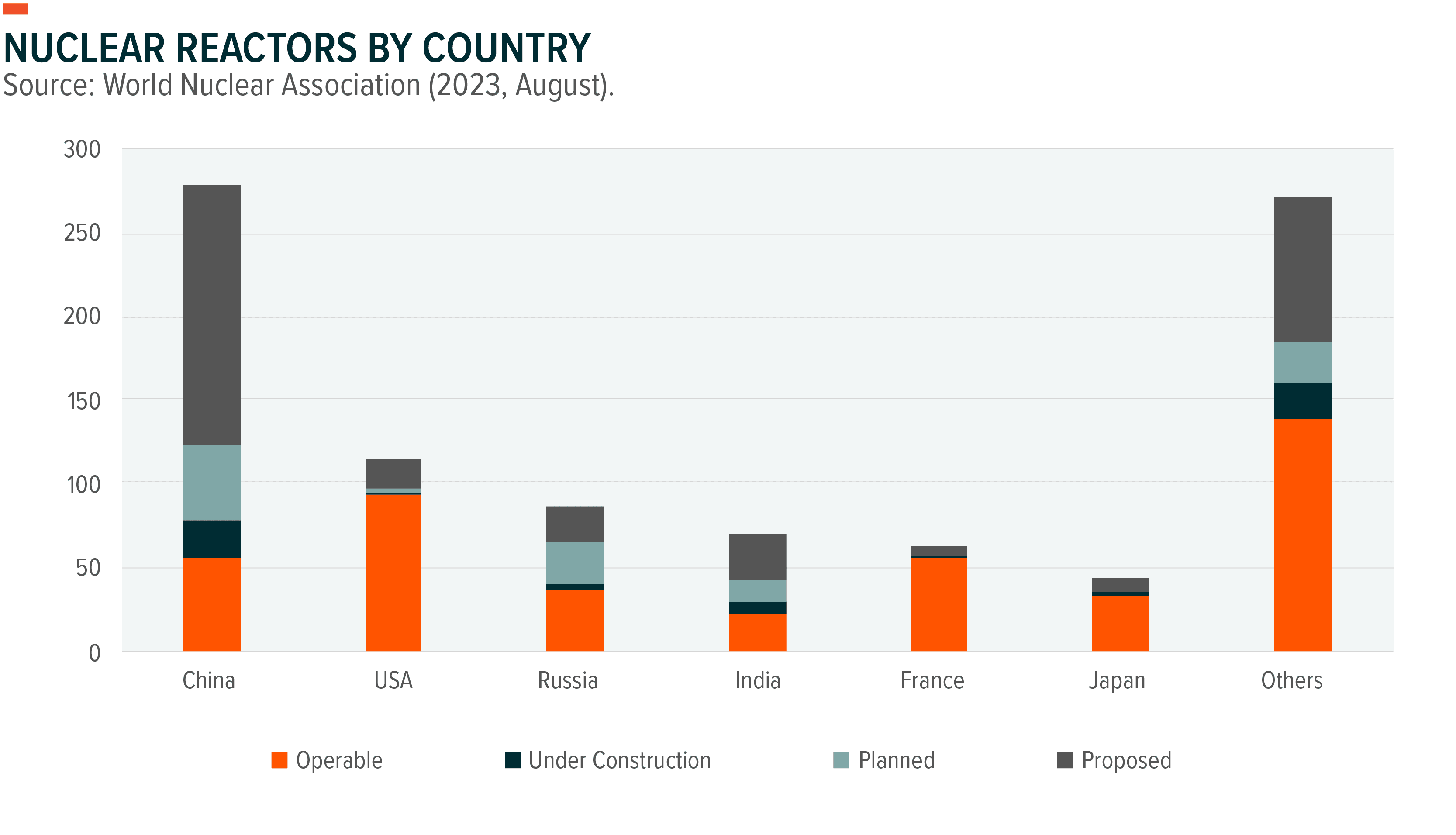

Nuclear power contributes approximately 10% of the world’s electricity generation and serves as a major source of energy in developed markets, such as the European Union (22%) and the United States (18%).16,17,18 Globally, 60 reactors currently under construction represent a 17% increase in nuclear capacity, with an additional 110 reactors planned.19 Reactors in the planning stage represent the second phase after design, while construction marks the final stage prior to being fully operable. The early-stage developments highlight the expanding appetite for nuclear over past few years. The planning stage represents a 27% potential rise in current nuclear capacity, largely led by emerging economies .20 Increased demand primarily derives from countries with large populations contending with the dual issues of substantial electricity requirements and escalating air pollution problems, such as India and China. The latter represents the world’s largest market for uranium and China plans to expand its nuclear power capacity significantly. China maintains 55 operational reactors, producing an estimated 53 gigawatts, 24 reactors under construction, and an additional 44 planned.21

China currently ranks third in the world for nuclear power generation, after France and the United States of America, but by 2030, it is anticipated to take the top spot for nuclear power installed capacity. 22 President Xi Jinping promised in 2020 to make China into a carbon-neutral nation by 2060.23 As a clean and efficient base-load energy source, nuclear power plays a crucial role in this achievement. By 2060, China's nuclear fleet should total 400 gigawatts, or around 18% of the nation's generation, that is more than the present fleet of nuclear power plants in the world and roughly seven times as much capacity as China currently has, which generates around 5% of the country's electricity. 24

Beyond larger emerging countries projects, such as China’s monumental one entailing building over 150 reactors, smaller nations such as South Korea, and Turkey also continue to gain government support for new reactors, with active planning of multiple reactors underway in each country.25

In the developed world, recently, France committed more than €100 million to reviving the nuclear industry. France's Ministry of Energy Transition invested the amount in civil nuclear training, research, and innovation. This follows President Emmanuel Macron's February 2022 "rebirth of France's nuclear industry" and October 2021 "France 2030" investment plan.26 France is mobilising a pro-nuclear alliance to safeguard its nuclear sector and wants the nuclear industry in Europe to be seen as a vital factor in the continent’s ability to compete with the US and China.27 Europe in general is echoing France’s shift in its stance on nuclear power. According to the EU Commission’s definition of net-zero, advanced nuclear technologies meet all current environmental regulations within the EU. In March 2023, EU agreed that nuclear power could help achieve the challenging climate objective. The agreement enables nations like France and Sweden to cut their green hydrogen ambitions for the industry by a fifth by 2030 if they primarily produce the remaining hydrogen using nuclear power rather than fossil fuels and continue to reach their total renewable goals.28

These global initiatives delineate the vital role that nuclear energy plays in decarbonisation efforts. The omnipresent shift away from fixed fossil fuels demonstrates the need for an on-demand clean source of energy to achieve net zero goals. Nuclear is a crucial energy source in filling energy production gaps associated with the energy transition. We can see in the United States, for example, nuclear power’s outsized reliability relative to other energy sources.

Utilising a technology with deployment capabilities to potentially power a small town or mining operation, the concept of small modular reactors (SMRs) is gaining greater traction. SMRs are defined as nuclear reactors, generally 300 MWe capacity equivalent or less, designed with modular technology using module factory fabrication, pursuing economies of series production and short construction times. China, Russia, Canada, Europe, and the United States have SMRs under construction or undergoing the licencing process, while globally approximately 90 SMR designs have reached various stages of development.29 Assembly of the core module of the world's first land-based commercial small modular reactor (SMR), Linglong One, was finished in August 2023 by the China National Nuclear Corporation (CNNC).30 Potential uses for SMRs include deployment in hard-to-reach areas and availability as an export, demonstrating the particular benefits of SMRs to rural communities. SMR components can also be prefabricated and shipped to a site, reducing construction costs and time. Because of lower fuel requirements, SMRs will require refuelling every 3 to 7 years versus 1 to 2 years for conventional nuclear plants, driving down long-term operating expenses.31

Uranium supply consists of new production from mining activity and existing inventories, largely from decommissioned nuclear weapons stockpiles. Since 1980, weapons-grade uranium in the United States and the former Soviet Union has been blended down to be repurposed as reactor fuel as part of nuclear disarmament agreements. This steady flow of supply kept uranium prices, as well as mining production, artificially low.

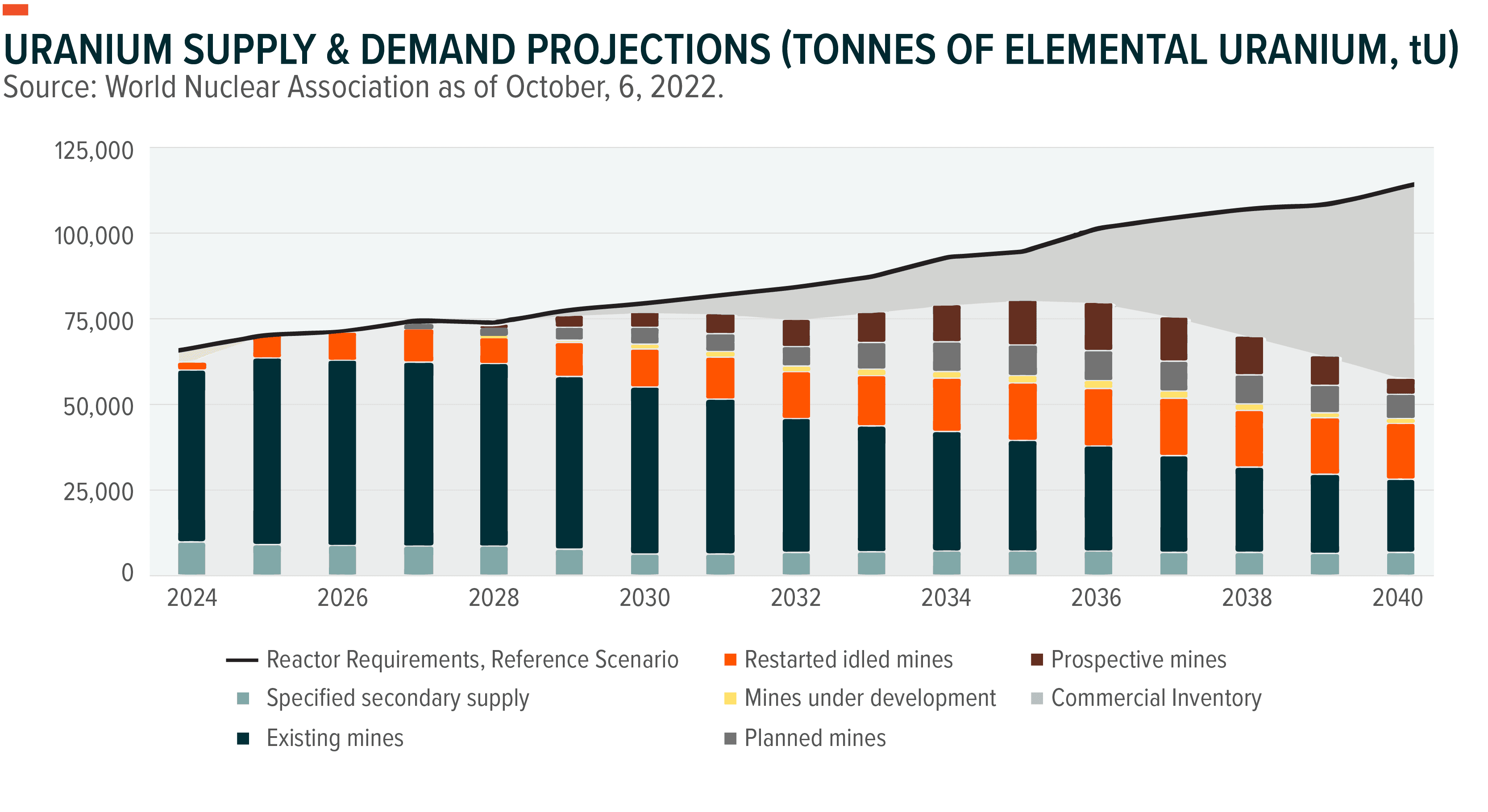

Supply from mining production met approximately 74% of 2022 uranium demand, with the remainder being met with commercial stockpiles, nuclear weapons stockpiles, recycled plutonium, uranium from reprocessing used fuel, and some from the re-enrichment of depleted uranium tails. 32Nowadays, the uranium positive investment thesis is supported by the potential absence of sufficient primary production as secondary supplies are shrinking. Current uranium spot prices might still not be high enough to encourage adequate output increases from the many miners who have shut down production these past years. It may take mines anywhere from two to three years before they begin producing at scale, and prices will likely need to be higher in order to get there. UxC, one of the world’s leading sources for data on uranium, predicts reactor uranium needs will rise to 190-200 million pounds by 2023, up from 165 million pounds in previous years. According to UxC estimates for primary output versus demand, the market is 60–70 million pounds short.33

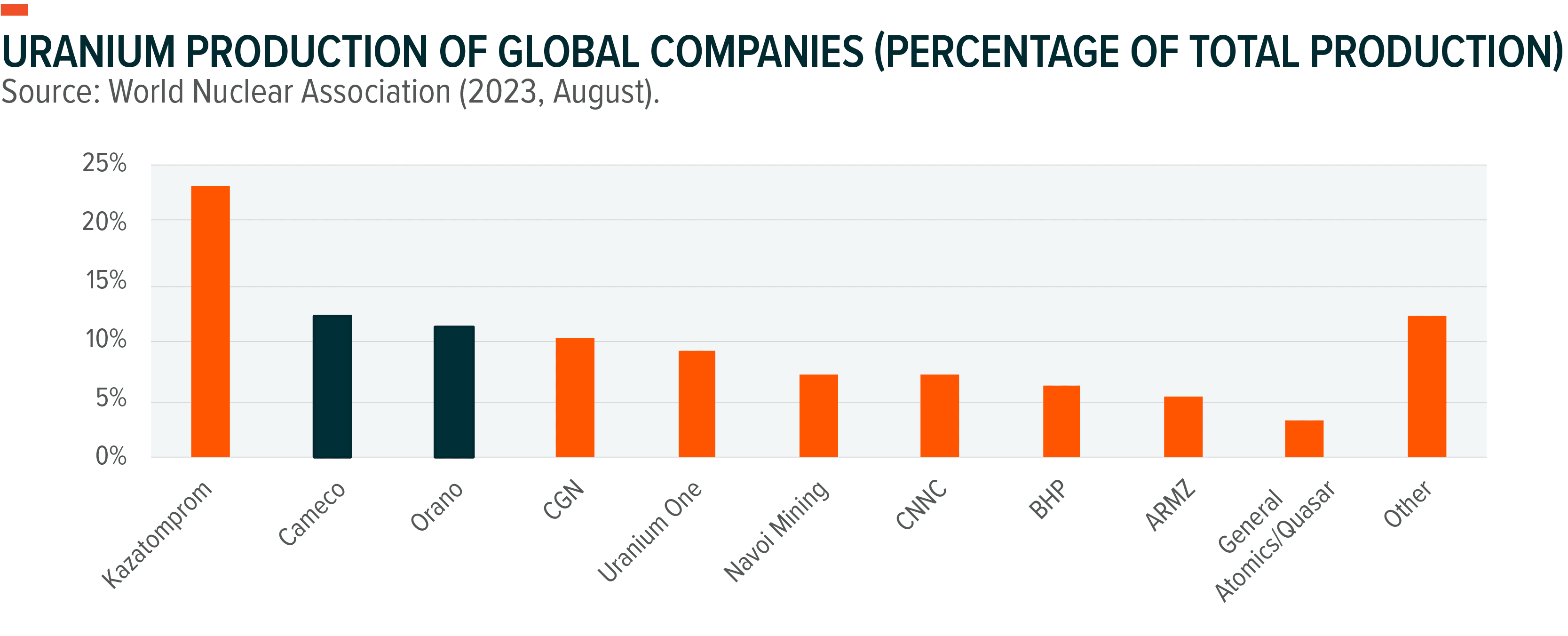

Canada ranked as the world’s largest uranium producer for over a decade, accounting for 22% of world output, but was overtaken by Kazakhstan in 2009.34 With geopolitical tensions affecting Central Asian producers, Canada may fill the void and potentially become the largest producer of uranium. Canada is rich in uranium resources and has a long history of exploring, mining, and generating nuclear power. Leading uranium miners are Cameco and Orano Canada, formerly known as Areva Resources Canada. These two companies produce over 15% of total uranium production and Cameco’s current plans for expanded operations could increase this total in the near future.35

In 2017, Cameco, one of the largest publicly traded uranium companies, produced 15% of the world’s uranium production, prior to widespread production cuts back in mid-2018.36 Cameco announced plans to restart production at McArthur River in February 2022, and on November 9, 2022, it was announced that the Key Lake mill had processed and packed McArthur River uranium ore for the first time since these facilities had been put under care and maintenance in January 2018.37

Cameco's uranium division operated at 60% below capacity in 2022 due to planned supply discipline choices, including returning McArthur River/Key Lake to production after five years on care and maintenance.38 They have adjusted their production schedule for McArthur River/Key Lake and Cigar Lake to produce at 100% capacity (18 million pounds per year) in 2024 due to market improvements, new long-term contracts, and contracting conversations.39 Cameco can boost production from its existing assets to 25 million pounds per year at McArthur River/Key Lake, but in that case, more investment is needed. They also expect to increase production at their Port Hope UF6 conversion facility to 12,000 tonnes by 2024 to meet their long-term conversion service business.40

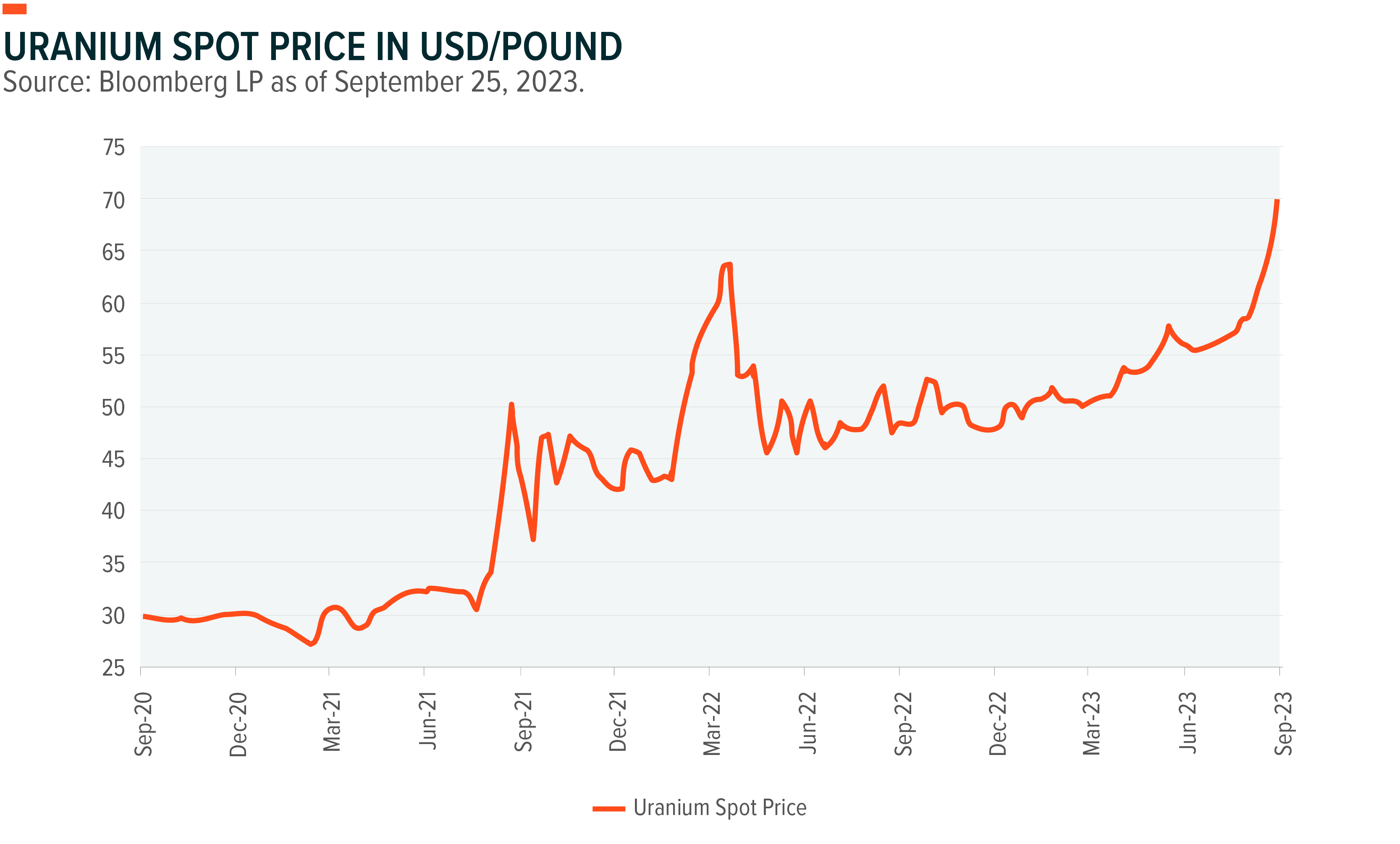

Uranium prices took a hit following the 2011 Fukushima nuclear disaster, which led to the multi-year shutdown of all nuclear power plants in Japan. Over the past eleven years, the global nuclear industry has recovered production of nuclear power beyond pre-Fukushima levels. Japan especially put a concerted effort into restoring its nuclear capabilities, operating a total of 33 nuclear reactors to date.41

Since the pre-pandemic environment the investment case has turned positive; in 2022, nuclear has been positioned as a climate solution based on the U.S. Inflation Reduction Act and a “transition activity” under EU Green Taxonomy. After the Russia’s invasion of Ukraine and the consequent energy crisis, the energy security concerns have bolstered uranium and nuclear role as a strategic and reliant source of energy. Uranium prices moved steadily higher in 2023's second quarter as positive catalysts continued to build. Even in a difficult economic environment characterised by recession concerns and high interest rates, uranium has distinguished itself from some of its commodity peers by continuing to maintain momentum. 42

The recent steps taken by policymakers towards validating nuclear energy demonstrate should support uranium prices and are anticipated to pique investor interest further. We believe the policy changes, as well as the supply deficit causing the new sources of demand, support a strong growth outlook for uranium.

The brisk stances taken by governments around the world are also advancing the broader uranium industry. Large uranium producers, such as Cameco and Kazatomprom, as well as small cap miners, can benefit from the shift to uranium. Thus far in 2023, the majority of uranium mining companies have performed well, but the bulk of uranium miners still trade at discounted levels compared to the pre-Fukushima period.43The focus on keeping operating margins high and costs lean should mitigate large spikes in supply, as miners slowly increase production based on contracted utility demand.

The nuances of gaining exposure to uranium increase in comparison to dealing in other more commonly traded commodities, such as oil or gold. Common solutions involve purchasing uranium mining stocks or exchange traded funds (ETFs) that own a basket of uranium mining stocks. Another entails gaining access to uranium futures, which trade with relatively light liquidity. Individual uranium miners potentially hold high idiosyncratic risks though, but accessing the industry through a broad basket of uranium mining stocks globally could help mitigate some of these risks. While uranium futures offer exposure to the spot price of uranium, they can be subject to negative returns associated with contango, which occurs when the spot price of a commodity trades below its future price, along with the thin liquidity.

Individual stocks also potentially offer somewhat of a levered play on the underlying commodity price, given the high fixed costs associated with mining. Uranium mining stocks maintain a relatively high unsystematic risk, due to the esoteric nature of the industry. For this reason, we believe investing in uranium ETFs may provide an efficient and cost-effective method for accessing a diverse basket of companies involved in uranium mining activities around the world.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Statista (2023, August). Distribution of electricity generation worldwide in 2022, by energy source.

2. IEA (2023, February). Low-emissions sources are set to cover almost all the growth in global electricity demand in the next three years.

3. McKinsey & Company (2023, March). What will it take for nuclear power to meet the climate challenge. Note: 2050 global net zero targets are taken into account.

4. GE Hitachi Nuclear Energy. (n.d.) Nuclear power basics. General Electric. Accessed on July 19, 2023.

5. World Nuclear Association. (2023, May). What is uranium? How does it work?

6. World Nuclear Association (2023, May). Uranium Mining Overview.

7. World Nuclear Association (2023, May). Uranium Mining Overview.

8. US Environmental Protection Agency (2023, June). Radioactive waste from uranium mining and milling.

9. World Nuclear Association. (2022, August). Economics of nuclear power.

10. World Nuclear Association. (2023, May). What is uranium? How does it work?

11. World Nuclear Association. (2022, August). Economics of nuclear power.

12. United States Environmental Protection Agency. (2023, February 15). Global greenhouse gas emissions data.

13. The levelized cost of electricity measures the overall completeness of plant types. It represents the per-KWh cost in real dollars of building and operating a generating plant over an assumed financial life and duty cycle.

U.S. Energy Information Administration. (2022, March). Levelized costs of new generation resources in the Annual Energy Outlook 2022.

14. EIA (2022, March) Levelized Costs of New Generation Resources in the Annual Energy Outlook 2022

15. U.S. Energy Information Administration. (2023, June). Electricity explained.

16. International Energy Agency (2023). Tracking Nuclear Electricity.

17. World Nuclear Association. (2023, May). Nuclear power in the European Union.

18. World Nuclear Association. (2023, August). Nuclear power in the USA.

19. World Nuclear Association. (2023, August). World nuclear power reactors & uranium requirements.

20. World Nuclear Association. (2023, August). World nuclear power reactors & uranium requirements.

21. World Nuclear Association. (2023, August). World nuclear power reactors & uranium requirements.

22. International Atomic Energy Agency (2023, May 26). IAEA DG Grossi in China: Nuclear Energy, Safety and Cooperation

23. Ibid

24. Bloomberg. (2023, April 27). China Nuclear Chairman Sees Sevenfold Surge in Capacity by 2060

25. World Nuclear Association. (2023, August). World nuclear power reactors & uranium requirements.

26. Nuclear Newswire. (2023, June 13). France invests over €100 million to revive nuclear sector.

27. Bloomberg. (2023, February 27). France Forges Pact to Make Nuclear Part of EU Clean Energy Shift.

28. Bloomberg (2023, March 30). EU Agrees Nuclear Has Role in Meeting Ambitious Climate Goal.

29. World Nuclear Association (2023, July). Small Nuclear Power Reactors.

30. World Nuclear News (2023, August). Core module installed at Chinese SMR

31. International Atomic Energy Agency (2023, September 13) What are Small Modular Reactors (SMRs)?

32. World Nuclear Association (2023, August). World Uranium Mining Production.

33. Chris Yates (2023, June 28) Are Uranium Prices About to Go Nuclear?

34. World Nuclear Association. (2023, June). Uranium in Canada.

35. Ibid

36. Canadian Mining Journal Staff. (2022, February 9). Cameco plans restart of McArthur River mine, Key Lake mill this year. Mining.com.

37. World Nuclear Association. (2023, June). Uranium in Canada.

38. Cameco (2023). 2022 Annual Report.

39. Ibid.

40. Ibid.

41. World Nuclear Association. (2023, August). Nuclear power in Japan

42. Investing News Network. (2023, July). Uranium Price Update: Q2 2023 in Review

43. Global X ETFs with information derived from Bloomberg LP. Solactive Global Uranium & Nuclear Components Total Return Index data from August 31st, 2010, to August 31st, 2023.